- Rate futures gained on hotter CPI data, and traders cut expectations of Fed easing and priced in a higher-for-longer policy stance

- Weakness in SOFR front-end contracts (Sep-Dec 2026) steepened the front-end curve and pushed up implied short-term rates.

- Treasury 2-year yields rose more than longer maturities, a sign of policy-driven, not growth-driven moves.

US interest futures stayed under pressure as traders repriced the Federal Reserve’s policy path after stronger-than-expected inflation data, with markets moving away from earlier easing assumptions and toward a higher-for-longer stance that now includes limited odds of further tightening.

In the SOFR futures strip, selling was concentrated in the front end, with both the September 2026 SOFR contract and the December 2026 SOFR contract under pressure relative to deferred tenors. The move flattened the front-end curve, indicating less confidence in near-term policy relief and a higher implied path for short-term funding rates into year-end.

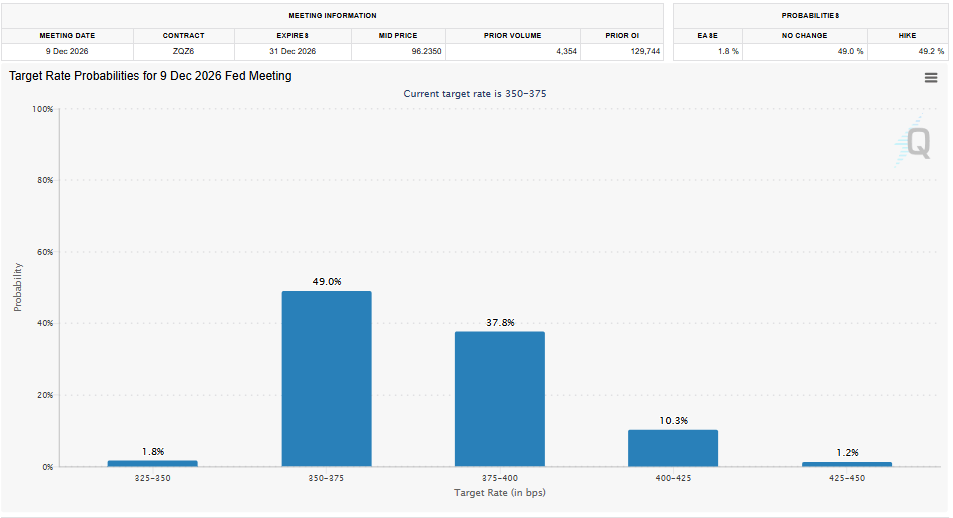

Fed funds futures also moved with the December 2026 contract pricing in a higher effective policy rate than in previous sessions. Pricing in the still-upper-restrictive zone is consistent with the market’s reassessment that the Fed may need to hold, and potentially even tighten, policy restraint if inflation persistence persists through the summer data cycle.

In the short-term rate markets, the options-implied distributions exhibited a clear shift in skew, with a higher probability of unchanged-to-higher outcomes than cuts. The repricing came following a CPI print that was above consensus across core components, particularly in services, confirming concerns that disinflation momentum has stalled.

The adjustment carried through to the forward SOFR curve, with mid-2027 contracts underperforming late-2026 expiries, flattening the expected easing profile and reducing the depth of any prospective rate-cut cycle. Market-implied terminal rate expectations for overnight index swaps were pushed higher as traders scaled back prior expectations of a sustained sequence of easing.

Treasury markets faced similar repricing pressure. The 2-year note, the most sensitive to policy expectations, sold off more than the long end, widening the 2s10s spread. The 10-year yield rose less than the 2-year, indicating that the move was more about the repricing of monetary policy than a broad growth shock.

Liquidity stayed centred in front-month SOFR futures and big-volume Fed funds contracts, with open interest climbing as macro funds and rate RV accounts repositioned around the new inflation trajectory.

Rate futures now generally suggest a regime where the base case is no longer policy easing. Instead, markets are pricing a conditional path based on whether upcoming inflation releases re-establish disinflation momentum or force the Federal Reserve to consider keeping restrictive policy for longer than previously expected.

Markets now await key US NFP data that could provide future guidance to the Fed policymakers. Analysts expect a decline in the payrolls with consistent unemployment around 4.3%.

{kind=link}