- A steep drop in US crude inventories increased fears of tight global supplies.

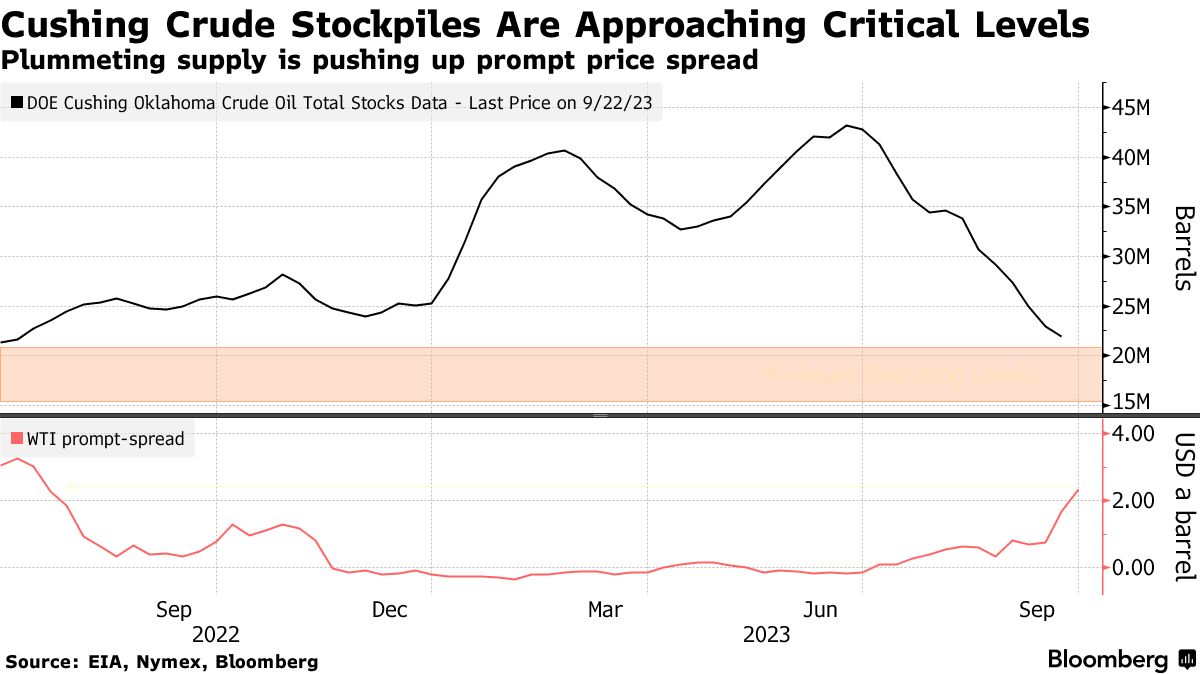

- Inventories at Cushing have been dropping amid strong refining and export demand.

- Vladimir Putin instructed his government to stabilize retail fuel prices.

Oil prices jumped 3% on Wednesday to the highest closing price in 2023 after a steep drop in US crude inventories increased fears of tight global supplies. According to government data, US crude inventories dropped by 2.2 million barrels to 416.3 million last week. The figure beat the 320,000-barrel drop forecast by analysts in a Reuters poll.

Data showed that crude inventories at Cushing, Oklahoma, a storage hub for US crude futures, went down by 943,000 barrels in the week to just below 22 million. It was the lowest since July 2022.

Cushing crude stockpiles (Source: EIA, Nymex, Bloomberg)

Inventories at Cushing have been dropping closer to historic low levels amid strong refining and export demand. This drop has raised concerns about the quality of the oil remaining at the hub and whether it could fall below minimum operating levels.

The tight supply was reflected in time spreads as front-month Brent futures traded at a 42.28 premium over the second month, the highest since October. On the other hand, front-month WTI futures traded at a $2.43 premium for the second month, the highest since July 2022. WTI’s discount to Brent was also at its narrowest since late April.

“The market is overbought, and we need a correction,” said Dennis Kissler, senior vice president of trading at BOK Financial.

Oil prices fell last week but rose again as investors worried about tight supplies heading into winter. These supply worries came after production cuts of 1.3 million barrels a day to the end of this year by Saudi Arabia and Russia, members of the Organization of the Petroleum Exporting Countries and allies known as OPEC+.

“Until a decision to increase production is made, the global oil market will remain tight,” Ole Hansen from Saxo Bank stated.

Further adding to supply tightness, Russian President Vladimir Putin instructed his government to stabilize retail fuel prices after a jump due to increased exports. In response, his deputy prime minister cited proposals to reduce exports of oil products purchased for domestic use.

Elsewhere, the Federal Reserve Bank of Dallas released a poll showing that oil and gas activity in three major energy-producing US states has risen with the latest jump in energy prices.