- Gold prices dropped after Powell delivered a slightly hawkish speech.

- Bullion recorded the best quarter since 2020, with an increase of 13%.

- Gold rallied on Tuesday after Iran launched missiles at Israel.

Gold prices pulled back slightly after rallying and ending higher on Tuesday due to escalating Middle East tensions. The conflict between Iran and Israel raised fears of a wider war, leading to a scramble for safety in the yellow metal.

On Monday, gold prices dropped after Powell delivered a slightly hawkish speech. Initially, traders had been pricing an over 50% chance of a 50-bps rate cut in November. As a result, gold prices strengthened. Notably, prices rallied to an all-time high after the Fed surprised with a massive cut in September.

However, the outlook for November changed when Powell suggested a 25-bps rate cut. Nevertheless, it was not enough to dent gold’s gains. Bullion recorded the best quarter since 2020, with an increase of 13%. Most of this move came from anticipation of lower borrowing costs in the US. Low rates increase the appeal of the nob-yielding precious metal.

The rally resumed on Tuesday after Iran launched missiles at Israel. The tensions in the Middle East have been slowly escalating, with Israel extending the war to Lebanon. With Iran now more involved, market participants were concerned about further escalation that could hurt the global economy. In times of uncertainty, gold shines as a safe store of value.

Meanwhile, the US released mixed economic reports on manufacturing and employment. Business activity in the manufacturing sector stalled, with the PMI coming in below forecasts at 47.2. Economists had expected an increase to 47.6.

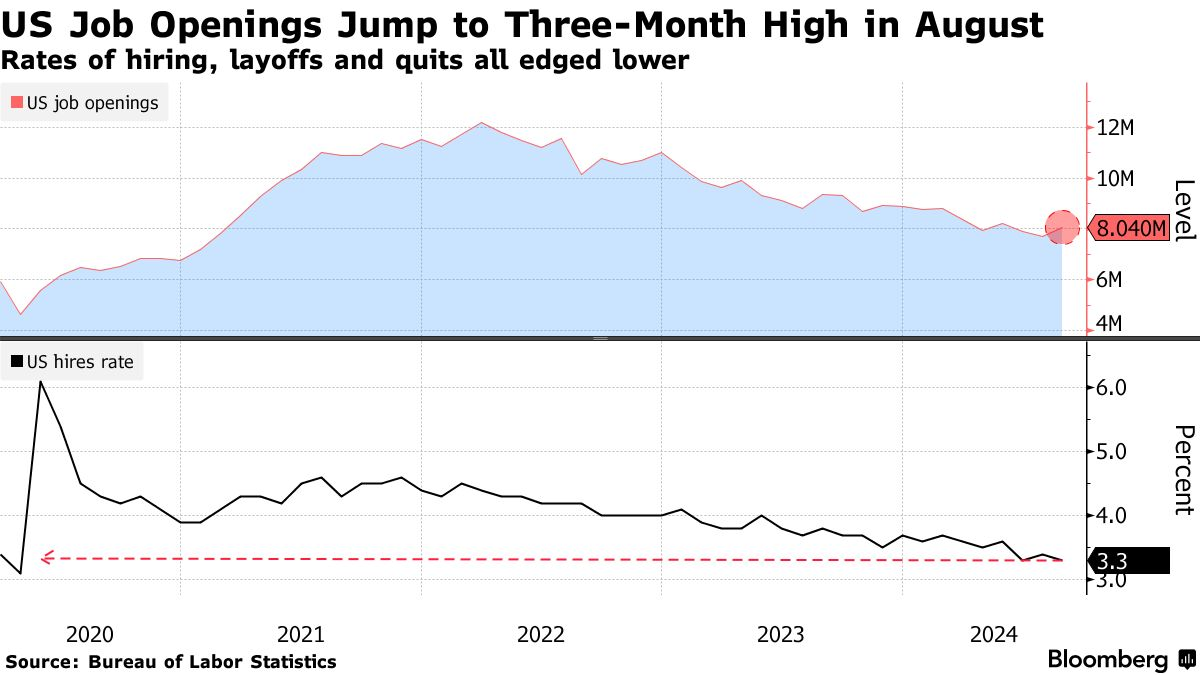

US job openings (Source: Bureau of Labor Statistics)

On the other hand, job vacancies in the US beat estimates, rising to 8.04 million, indicating robust demand for labor. The labor market is a significant sector in the Fed’s rate cut outlook. The central bank has closely examined employment and unemployment levels for signs of weakness. Some reports raised fears of deterioration. However, the general picture is of resilience.

This week, market participants will watch the US nonfarm payrolls report for clues on what the Fed will do in the future. Consensus estimates show an addition of 144,000 jobs, slightly above August’s increase. Meanwhile, the unemployment rate could remain at 4.2%. Better figures will lower the chances of a significant cut in November. On the other hand, poor numbers might rekindle hopes for another massive rate cut.