The Chairman of the US Federal Reserve, Jerome Powell declared a flexible tactic of aiming at inflation that lets it surpass the intended 2% level temporarily if this level has been undershot before. The aim of the alteration tactics is to increase the inflation rate after many years and this is when it becomes the standard for inflation. The Federal Reserve also showed in its financial policy framework analysis, its dedication to react not just to the general level of employment, but to also underemployment of those sub-level workers. This shows its dedication to increasing inflation.

In 2019, the Federal Reserve was involved in an anticipatory financial thinning sequence that ended in the market displacement of the 2018 fourth quarter which was the last show to be put up by a Western central bank. This then absolutely corroborates our prediction in 2019. The modification of the Federal Reserve policy Fed’s tactics increased the demands on other Western central banks, thus causing them to tail along.

However, we have had no explanation from the US central bank on the means they will take to attain inflation overrun after undershoots. As explained by MMT economists, backing the idea for the fiscal and monetary policy fusion, this involves the approval of frequent public arrears and the related amplification of government arrears till a time they begin utilizing industrious resources and achieve complete employment and capacity utilization.

What Is Price Level Targeting?

Price level targeting is a financial strategy framework that you can use to arrive at constancy in price. Price level targeting is similar to inflation targeting and sets up targets for a price index like the consumer price index (CPI). However while inflation targeting aims ahead, price-level targeting monitor standard price alterations and consigns to repealing any provisional digressions from the intended inflation rate.

For example, if inflation decreases less than 2% for a while looking back, the central bank would reimburse by targeting inflation higher than 2% momentarily until typical inflation for that time had gone back to 2%.

Overview

- Price level targeting is a means central banks use to pass monetary policy by aiming at an exact price index level, as the CPI.

- Comparable to futuristic inflation targeting, price level targeting modifies itself with past occurrences.

- Price level targeting is particularly functional in a low-interest-rate environment when rates are almost at zero percent, as it can promote a more insistent expansionary strategy than an undemanding inflation objective.

Understanding Price Level Targeting

Price-level targeting is, supposedly, more efficient than inflation targeting since it has a more specific target. However, it has more risks as it could miss the target which would bring about some penalties. If in a certain year, inflation suddenly becomes high, this means that they would have to reduce the cumulative prices the next year.

For instance, if an impale in oil prices results in a brief inflation increase, a price-level-targeting central bank would be forced to constrict financial policy, regardless of declination in the economy. This is comparable to an inflation-targeting central bank, which may disregard the momentary inflation increase. This would be a political burden.

This price-level targeting trend of increasing the volatility of inflation and its ability to enhance the economic cycle is the reason central backs are skeptical about trying price-level targeting after the experiment Sweden performed with the policy in the 1930s.

Price Level Targeting at the Zero Bound Interest Rate

Nonetheless, as the nominal interest rates in many countries now approach the zero bound, the implementation of price-targeting has become a current problem. When the Price level targeting is at the zero bound, it creates a negative demand shock that results in the increase of the real interest rates in inflation targeting, only if anticipations for inflation remains unchanged.

The situation deteriorates if families and businesses feel that monetary policy doesn’t function properly again and this causes them to lose hope. If this situation occurs, real interest rates grow more and make it possible for the economy to go into a recession.

On the other hand, price-targeting generates a different inflation anticipation outlook when anytime the economy faces a negative demand shock. A plausible price-level target of 2% inflation would generate the anticipation that there could be a rise in the level of inflation beyond the 2% target, given that people would be aware that the central banks are poised to offset the deficit.

This will push the price up more and would result in lower real interest rates. It’ll equally activate aggregate demand. The tendency of price-level targeting resulting in higher GDP growth in a deflationary environment or not compared to inflation targeting high depends on whether or not the global market conforms with the New Keynesian outlook that wages and prices are sticky.

What this means is that show slow adjustment to near-term economic fluctuations, and that people rationally generate their anticipations for inflation.

Fed Reveals New Attitude Towards Inflation in Major Policy Shift

The coronavirus-activated recession termed “The Great Lockdown” by the International Monetary Fund will result in a dramatic alteration of the debt profile of the world economy. Many governments, businesses, and families borrow a large amount of money to help them recover from the effects of the lockdown.

What this means is that the ability of government, businesses, and families to service these debts would be the determining factor of economic recovery.

While fiscal measures to temporarily replace lost incomes of firms and households have taken center stage, the Federal Reserve signals low rates and looser inflation targeting strategy.

The new strategy of the Federal Reserve is a “flexible” one which will remain low, although not unhelpful rates and let inflation increase “fairly” higher than 2% for a while, as its main aim is to enhance employment on a wide basis.

In the past, central banks would attempt obstructing inflation and increasing interest rates whenever they arrived at total employment, but this would not be the case again. In a press interview, Powell said, “Many find it counterintuitive that the Fed would want to push up inflation. After all, low and stable inflation is essential for a well-functioning economy.

And we are certainly mindful that higher prices for essential items, such as food, gasoline, and shelter, add to the burdens faced by many families, especially those struggling with lost jobs and incomes,” He went on to explain that when inflation remains constantly on a low level, the economy will be at severe risk.

This new structure adopted by the Federal Reserve is excellent news for investors in gold and the U.S. stock as loan rates like mortgages or auto loans will stay low. Unfortunately, it won’t serve the dollar rate well since worldwide central banks and the ECB will have a motivation to follow that pattern.

Challenges

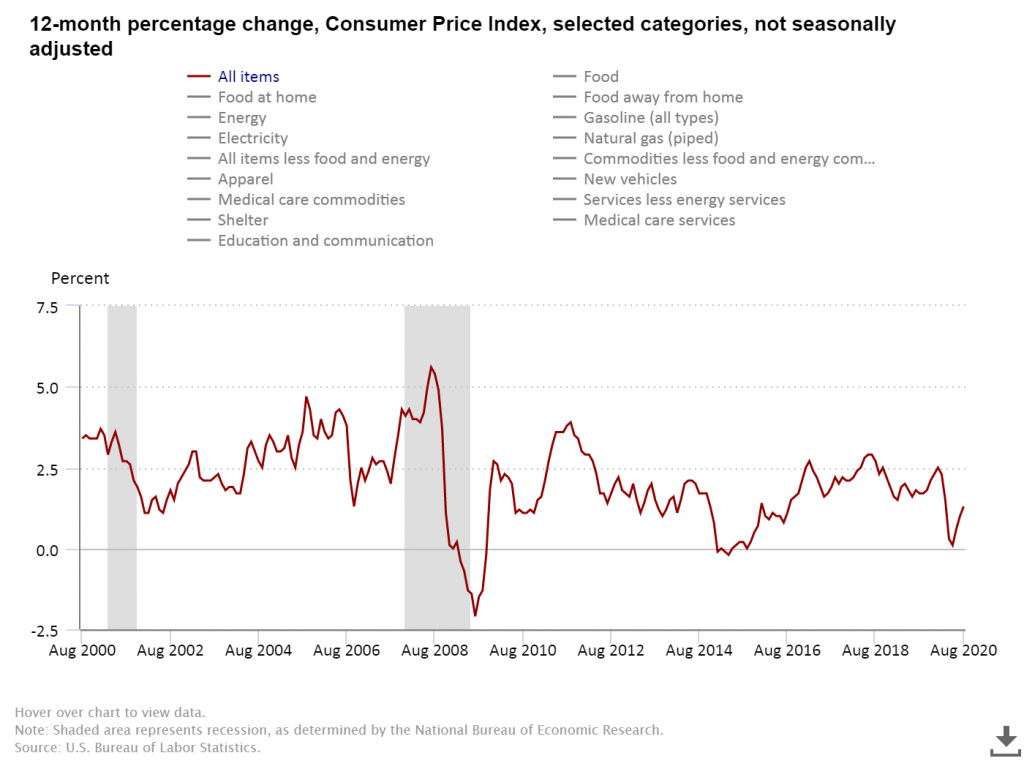

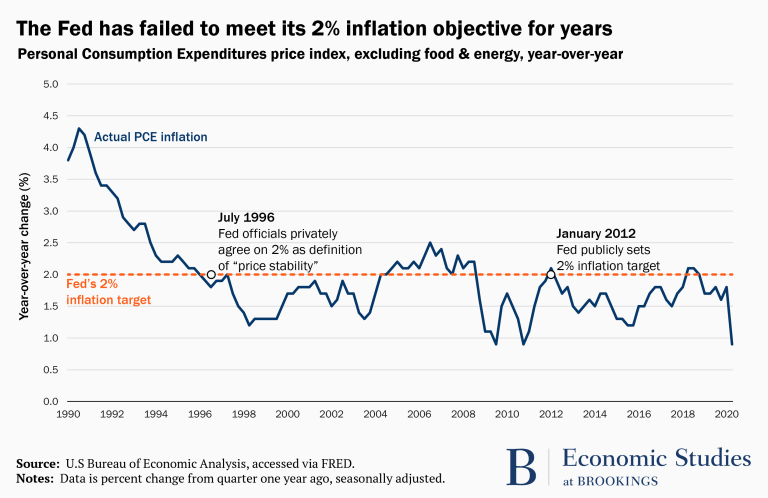

In 2012, U.S. inflation was lower 2% and it has persistently continued to stay that way and it is difficult to sell higher prices to people like in the event of the most horrible economic decline in years with the pandemic as an instance. The challenge Powell faces now is to clarify the necessity of the momentous strategy modification, which is as momentous Paul Volcker’s 1970 conflict when he was trying to abscond high inflation.

Volcker’s condition underlined the behavioral feature of the functioning of policies. He let unemployment in particular to rise as he slashed the economic money supply and which made him face extreme pressure and criticism for a long period. Inflation was at a high level for several months as people had no beliefs of a drop with an increase in wages by managers. Japan is another eminent illustration of policymakers that cannot manage their prices.

Powell will as well have to persuade investors and markets that the Federal Reserve can increase inflation taking into consideration its low level regardless of low unemployment, which defies the Phillips curve. When the country keeps manufacturing goods cheaply and innovating new technologies outside, prices will keep reducing. For this to fall into place, the Federal Reserve will have to cooperate intently with the Congress on financial support.

Details Of Plans Remain Obscure

Even though we currently have a plan for this unruffled course, worrying professionals at this time shows the lack of realization details. The President of the Federal Reserve in Dallas told CNBC that it is not dedication or formula to and they will employ arithmetic standard since moderate is merely equal to 2 and a half or 2 and a quarter.

In a blog post, Tim Duy, an economist wrote that they do not the time and level at which the Federal Reserve can tolerate inflation. He also explained that they have no idea of the terms on which they would ease the policy as they rely on operational leadership to back the new policy.