Convenience yield is the profit or premium you get when you buy and hold an underlying asset, inventory, or physical good, in place of the security derivatives or futures contract. Convenience yields of products have a close relationship with the storage of such goods or commodities.

Nonetheless, the storage levels and the prices of the commodity are inversely related. Depending on the supply and demand levels, if the storage levels of a product are scarce, the price of the product will rise. The contrary also applies if the levels of storage of a product are surplus and in this case, the price normally falls.

Convenience yields mostly apply to assets purchased for consumption. It’s unrelated to assets that are held as investments. A good example of a commodity with a high convenience yield is oil. The profit you make from direct ownership of oil implies that you can produce oil and store and make profits by selling at higher prices anytime there are shortages.

More Explanation Of Convenience Yield

Occasionally, market swings irregularities occur and when this happens like in an inverted market, you may be able to make extra profit by holding an underlying asset or security compared to when you own the contract or derivative instrument because of its relative scarcity compared to high demand.

Another example is when you buy physical bales of wheat instead of wheat future contracts. When there’s an unanticipated scarcity, the demand for wheat will increase and the difference between your primary purchase price of the wheat and the selling price of wheat after the draught becomes your convenience yield.

Convenience yields frequently occur when the cost of storing a physical product, including warehousing, insurance, security, and more is comparatively small.

Processing companies like those that deal with oil refineries, metallurgical plants, and processors of food products need their raw materials to be physically available to maintain non-stop business activities. In a bid to avoid increasing the cost of raw materials or disrupting their production processes in the event of scarcity, they may erroneously buy a product at a spot price that is higher than the futures price.

Thus, Kaldor (1939) and Working (1949) came up with a storage theory referred to as convenience yield to explain the profit an owner of a physical inventory makes and the experimental difference between spot and futures prices and, in extension, how the commodity term structure is shaped.

In light of the above, a convenience yield can be described as a return on a specific type of asset, known as ‘convenience claim’. The convenience claim asset is made up of a short position in a commodity future mixed with a spot purchase of the equivalent underlying asset. Convenience claim, therefore, is equal to a near-term lease contract of a single unit of an inventor, also referred to as a calendar spread.

Therefore, convenience claims investments make it easy for an investor to get convenience yield remuneration for temporarily providing the underlying asset physically. Because investors know the value of their convenience yields beforehand, the profits of the convenience claim are equal to the negative convenience yield in the last month.

Know, however, that the value of physical inventories commonly rises when there is an increase in scarcities. As a result, convenience yields make it easy for investors to predict future demand and change in product prices.

Convenience Yield and Cost of Insurance

Investors can estimate the convenience yield as the insurance cost against the price risk. The formula can be obtained by multiplying the front-month futures contract prices with the capital cost of their money that is locked down in the inventory. It can equally be estimated as the Euler’s number raised to the arrogating rate multiplied by the maturity time plus the storage cost. The final result is obtained by subtracting the price of the futures contract from the contract of the back-month.

After that, you need to divide the result obtained by the price of the futures contract of the front-month and add one to the quotient. Then, divide the result obtained by the number of days it takes to mature after raising it to the power of 365. Lastly, subtract one from the result you get.

Practical Application Of Convenience Yield: Illustration With The Crude Oil Market

It is easy to estimate the convenience yield if you know the future price, spot price, borrowing rate, and maturity time of a commodity. To obtain the futures price, multiply the spot price by Euler’s number, or the arithmetic constant e, raised to the power of the answer you get by subtracting the borrowing rate from the convenience yield and multiplying it by the maturity time.

As a result, the convenience can be calculated as the variation between the borrowing rate and the inverse of the maturity time multiplied by the natural record of the futures price divided by the commodity’s spot price. You can utilize this formula for regular compound rates and profits.

If a trader wants to estimate the convenience yield of West Texas Intermediate (WTI) crude oil to be delivered one year ahead from today. Assuming that the yearly borrowing rate is 2%, the spot price of WTI crude oil is 50.50 USD and the futures price of crude oil contracts for one-year expiration from today is 45.50 USD. Thus, the convenience yield will be estimated to be 12.43% consistently compounded every year, or 0.02 – (1/1) multiplied by LN (45.50 USD/ 50.50 USD).

The Storage Convenience and the Corresponding Yield

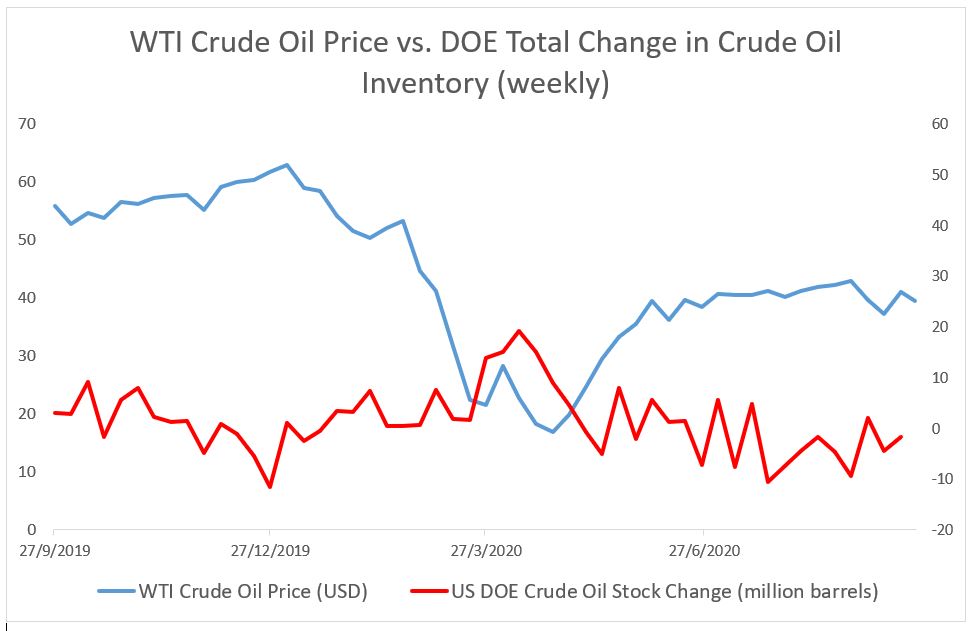

One of the basic determiners of the crude oil price is inventories. Because crude oil is a product that needs to be stored, crude oil stocks connect the present demand and supply to anticipations of future demand and supply. Inventories contribute immensely to a commodity price given that holding stocks is essentially valuable due to their provision of operational flexibility.

For instance, because of issues of technology, an oil refinery is incentivized to hold stocks to boost its petroleum products output and this helps to minimize the costs of altering production and assisting them from running out of stocks. As a result, the highest levels of production and inventories are mutually figured out as long as you know the spot price of oil and the price of storage.

The convenience yield can equally be regarded as the interest rate you pay in barrels of oil to borrow a single barrel of oil. You’ll find that when you borrow a barrel of crude oil, you’ll be adding to the storage supply as a borrower in the form of crude oil inventories to your lender.

As a result, you must compensate your lender for ignoring the profit connected to holding the barrel of oil. To balance the equation, this obligation or condition connects the convenience yield with the storage price and this is the marginal value of the accruing services from holding an extra unit of inventory over the cost of physical storage of crude oil.

How Convenience Yield is Correlated With Inventories

The theory of storage proposes that:

- The marginal gain for holding inventory increases as the rate of the scarcity of commodities decreases.

- The marginal cost of physically stored oil can be regarded as constant. This means that a single period convenience yield is presumed to be a [declining] function of the inventory levels.

Hence, we anticipate a negative and unitary correlation between the convenience yield and the present crude oil stock level. We estimate that there is this kind of relationship in the U.S. Crude oil inventory market.

How to Estimate Convenience Yield and the Related Curve

Although you cannot directly observe convenience yields, you can synthetically replicate them by taking concurrent positions in forex, crude oil spot, and futures markets grounded on the principle that the spot and futures markets are connected consistently with a lack of absence arbitrage opportunities. What this means is that a high convenience yield is specified by a high spot relation to the futures price.

By analyzing futures contracts with multiple expiration dates, we gain access to the term structure data of convenience yield regarding the inherent advantage of physical storage across multiple horizons. For instance, a convenience yield curve that slopes upwards show a scenario where refineries designate a higher value to future inventories compared to the value they put in the present-day inventories. Periods like this show that oil inventory will be smaller in the future.

Oil futures contracts‘ market liquidity is high. On the side of sellers, financial institutions are starting to take more active participation in the commodity derivatives markets and these long-term maturity futures contracts. On the side of the buyers, augmented investor interest leads to big quantities of financial capital unsettled in these markets within the past decade.

So, the researchers investigated the sample period that started in April 1989 to June 2013 and explored the rise in the liquidity of long-term maturity oil [WTI] futures contracts to theorize the one-year term structure of convenience yields.

Fundamental Features of the Crude Oil Convenience Yield Curve

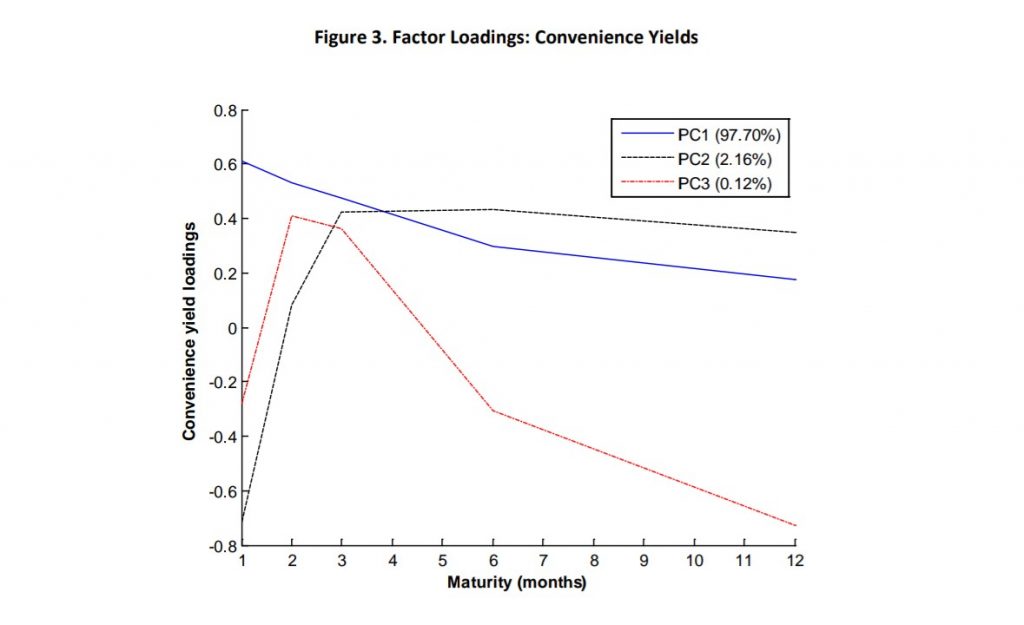

A cross-section of crude oil convenience yields across maturities can be investigated by a small number of key constituents. Related to the term structure of interest rates, the primary factor is to look like a level factor that commonly applies to different horizons of maturities. The second factor is linked to the slope of the curve. These are all technical manners of showing that oil futures curves are commonly smooth instead of forming segments and kinks just like you’d obtain in a few agricultural commodities or livestock.

The convenience yield curve is funnel-shaped and this indicates that the long-term convenience yields’ sensitivity to short-term convenience yield swings dies off as the oil bond matures. Excitingly, the funnel shape signifies that the volatility of convenience yields is a diminishing function of the contract maturity.

An Empirical Study of Convenience Yield

An empirical study of convenience yield shows that convenience yield is dependent on risk factors associated with other classes of assets. Nonetheless, these risk factors inertia appears to assist in the prediction of returns for convenience claims.

Empirical evidence provided by Bollinger, Thomas, and Axel Kind (2015) shows that the primary key feature of convenience yields [also referred to as their level] is negatively correlated to real and nominal prices of crude oil futures. Prices of crude oil commonly fall anytime there is a high convenience yield or when crude oil is scarce.

What this implies is the back-dated futures curve signals the price of future spot prices. This result is commonly due to the sluggishness of the supply response and the average reversal of convenience yields and crude oil scarcity. We have mentioned above that an unanticipated rise in demand can make the spot price of oil overextend in the near-term because it takes time for supply to react to such market rebound.

The empirical study was performed using 22 samples of commodity futures from January 1991 to December 2011. The study integrated 36, 319 monthly futures prices overall and this includes products, metals, and agricultural products.

The researchers implemented the Schwartz three-factor model due to its popularity. The study variables included were the spot price, the real-time convenience yield, and the risk-free interest rate. Using this technique makes it easy for you to figure out the value of the convenience yield and alienate it from other factors that affect futures prices (which include the spot prices and interest rates of the commodity).

By viewing the convenience yields as profits of convenience claims they used the multi-factor asset price models to study the risk exposures of the products in addition to the presence of risk premiums in the convenience yields cross-section.

They utilized 5 economic variables that stand for credible broad-economy risk factors that are regularly utilized in the empirical asset pricing literature.

These economic variables include:

- S&P 500 Index Returns

- The Citigroup world government bond index

- The Goldman Sachs commodity index

- The U.S. industrial production growth rates

- The unanticipated inflation

They equally utilized Instrumental variables to predict alterations of risk premiums related to each risk factor. And four instrumental variables were utilized for the study and these include:

- The lagged dividend yield of the S&P 500 Index

- The mean value of lagged spread of yields of Baa-rated and Aaa-rated corporate bonds

- The capacity utilization rate of all US industries

- The level of Fresh orders in the U.S. economy

Factors That Determine the Convenience Yields?

The factors that activate convenience yield in all commodities besides a few precious metals are stochastic and mean-reverting convenience yields.

The study found returns of convenience claim investments (which are directly influenced by the term organization of commodity futures) to risk factors that affect stock and bond returns. It shows the presence of substantial premiums entrenched into convenience yields for methodical risk factors linked to other classes of assets. Also, there was a correlation to the risk factors of the broad economy.

This more precisely relates to the bond-loaded convenience claims. Also, the commodity spot market earnings’ data showed a high premium. The outcome of the cross-sectional data sample composition was robust. The same applies to the asset pricing model.

Alterations in provisional betas, according to the findings, predict the differences in convenience yields. Because the differences in the convenience yield are activated by logical factors, the bundle benefits in commodity trading techniques cannot be viewed precisely as characteristic return features of commodity investments.

Convenience Yields and Profits Projections

The recognized risk premiums can only be slightly predicted by several commonly utilized helpful variables. A good number of risk premiums in commodity markets are non-predictable.

Nonetheless, the best technique for the prediction of convenience-claim returns is to evaluate the strong levels of automatic relationships obtained in their factor loadings. Choosing commodity portfolios of equal with high and low conditional betas with regards to the two essential risk factors- the bond and commodity spot market- leads to average convenience-claim returns that vary significantly.

To investigate this simple correlation, the researchers formed constructs for every one of the five risk factors portfolio pairs, which included the 11 commodities with the highest (lowest) provisional betas. They rebalanced each of the 5 portfolios at the start of every month after the estimated betas for the preceding month. The obtained data showed significant variations between pairs of portfolios. And these variations were identified when sorting with:

- Bond market loadings

- Commodity index price loadings

In each of these scenarios, the variation in return is higher than four percentage points per year, and the high-beta portfolio’s returns are a lot bigger than zero.

Convenience Yield for Predicting Changes in Stocks

To investigate how convenience yield predicts changes in stocks, we examine if the term structure of convenience yields consists of data that reveals the future direction of inventories in PADD 2, which is the administrative area of the oil distribution network in the United States. Cushing, Oklahoma, which is the delivery point for the WTI futures contract is located within this region.

The level and slope factors help to predict future changes in crude oil stocks for up to one year. Following the theory of storage, long-term maturity convenience yields are forward-looking variables concerning Crude oil scarcity.

Using Convenience Yield to Predict Production and Price

Given that convenience yields can be estimated by the correlation that exists between storage decisions concerning the crude oil supply and demand, convenience yields equally provide us with data that shows the future states of the physical Crude oil market and future prices of oil. Empirical studies show that the term structure of convenience yields consists of future crude oil production data, worldwide real economic events, and the actual Crude oil price.

If there are anticipations about a future fall in the supply of crude oil compared to future demand for oil, agents will increase their demand for crude oil stocks today because they anticipate future deficit in net oil supply. On the other hand, the best response of suppliers to this scenario is to boost their production of crude oil.

Nonetheless, it takes a while for the increased production to reflect because of the oil supply curve inelasticity. This collection of forces generates a scenario where the increase in today’s inventories leads to an increase in the production of crude oil to offset the extra demand for crude oil stocks. Empirical studies show that the short-term production of crude oil is inelastic.

Conclusion

Convenience yield is a profit made from holding an underlying asset, instead of the derivative security or contract. Convenience yields commonly exist when the cost of physical storage of a commodity is low. Investors ought to be aware of the future price of the product, the spot price, the borrowing rate, and the maturity to be able to estimate the convenience yield.

You may want to purchase a product straightaway when the level of supply is low, and the demand is high. Convenience yield boosts your profit potential and frequently occurs in an inverted market.

Nonetheless, it is significant to remember that any value you put on the immediate acquisition of a product vis-à-vis the futures contract depends on future events, and this is not always guaranteed. While the convenience yield value is always implied, just like every other type of investment strategy, it equally comes with a risk. So keep this in mind while investing and know that it may not always be profitable.

For more insights into futures trading and strategies to consider, read our blog: Top Futures Trading Strategies.