In a new turn of events, the European Commission may just become the new major player in the European financial markets. Over the years, the eurozone hasn’t been an ideal spot for investors. In fact, the currency’s super-safe pool and triple-A international securities shrank by at least 40% from 2007 to 2018.

Even the rating agencies had no choice but to downgrade a few of its trading members during the 2010-12 debt crisis. Conversely, Netherlands and Germany have managed to reduce their debt ratio significantly. According to Bundesbank, Germany may divert focus from its balanced budget strategy. It might face a GDP fiscal deficit of 7.5% in 2020. Interestingly, the coronavirus pandemic may mitigate the shortage.

Source: Google

Simultaneously, the European Commission plans to offer new insurance plans. The intention is to finance the European Union’s recovery amidst the COVID-19 pandemic, and if all things go right, the EU can become a major influencer in the global financial market.

EU – Issuance of Bonds

As of now, the European Commission has already managed to issue bonds for the EU. The total amount of bonds will be pass onto official member states. Currently, the debt stock €52bn (i.e., ($59bn), which is 0.4% of the European Union GDP in 2019.

However, the funding plans to completely recover from the scourge of the pandemic will increase this amount. Onwards September, it will amount to €100bn, which the EU will lend to member countries to fund temporary-employment schemes.

The Recovery Plan

Also, another exciting thing is that national leaders intend to debate the recovery fund. Consequently, the recovery fund will be able to raise €750bn on the capital markets to fund loans and grants to member states.

Although the recovery plan has managed to garner almost all countries’ complete support, some northern states haven’t agreed to the recovery plan idea yet. Nonetheless, if the current plan of action takes its course, the European Commission’s cumulative debt will be smaller than the EU’s four biggest member states (i.e., France, Germany, Spain, and Italy).

Investors are Optimistic

Despite pessimistic uncertainty in the air, the new initiative and issuance of recovery plans have certainly captured investors’ interest. Ordinarily, the majority of the EU’s bond-holders are numerous institutional investors of Europe.

In addition, Asian countries that value diversification of their portfolio from USD hold some bonds too. Rating agencies will soon determine the safety of the bonds. It will primarily depend on member states’ guarantees, which is not finalized at the moment.

The Role of the European Central Bank

European Central Bank, for instance, could also become another buyer of European Commission debt. Safe assets will render a high demand in the post-pandemic period. In fact, continuous economic predicament and the aging population will increase the saving rate.

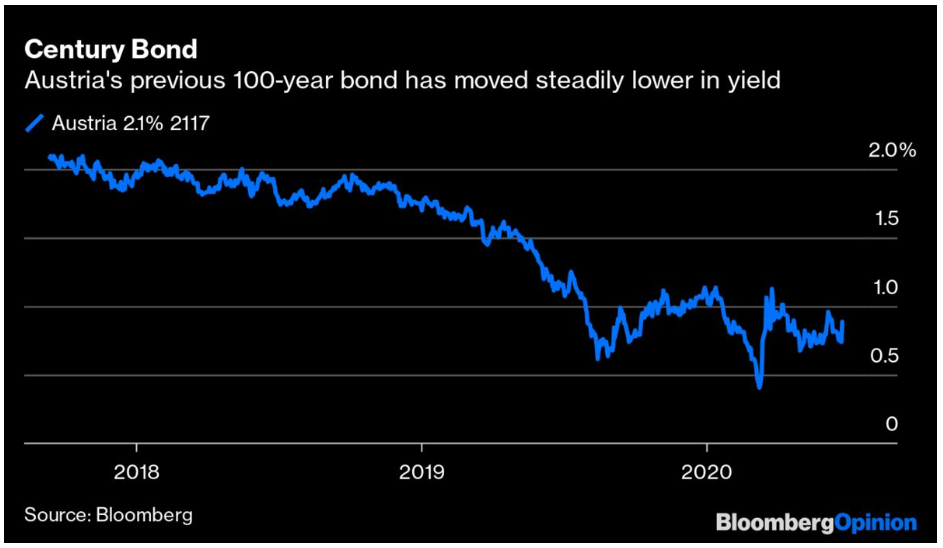

However, it is interesting to note that investors are interested in Austria’s century-old bond that was issued back in June. There were ten times more sales than oversubscribed. As a result, the 100-year old bond is now trading a return of 0.7%.

Benchmark Asset

The question is, will the European Commission’s bonds become a benchmark dominated asset in the foreseeable future? If not, the blame on a single currency to make up the dollar status often serves as a reserve currency. Therefore, the benchmark may improve the integration of banking systems throughout the EU.

Besides, over the years, member states haven’t been able to concur on a mutually beneficial deposit-insurance plan. And that’s because lenders almost always hold most of the country’s debt amount. Subsequently, it exposes lenders to face new challenges in government-bond capital markets. Thus, a common agreed-upon safe asset will undeniably help break the Mobius strip.

Conclusion

Ultimately, to turn bonds into a benchmark asset, investors will have to trade rather than hold indefinitely to mature. It is an enthusiast approach that would pave the way for secondary trading. Fortunately, the European Commission intends to issue bonds with maturities of more than 30 years. It would build a high yield curve, but a lot depends on the state of politics in Europe.