{kind=link}

Asian stocks are currently doing better than the U.S. and European stocks. The major cause of the upbeat stock prices in Asia is China’s ability to recover faster from the COVID-19 induced economic recession.

This created the notion that some regions in Asia have succeeded significantly to control the Coronavirus pandemic. This saw the MSCI Asia Pacific Index move up by roughly 9% starting from the last days in May to Mid-July, 2010. The S&P 500 Index and the Stoxx Europe 600 only recorded a 6% rise.

The rise in Asian stock prices was mostly driven up by the positive price changes of Chinese Tech stocks. The major cause of the positive move comes from the Tencent Holdings Ltd., Alibaba Group Holding Ltd., and Taiwan Semiconductor Manufacturing Co. They contributed to nearly one-third of the index’s price rise.

Asian Equities Show Positive Moves Thanks to Their Government Ability To Contain Coronavirus

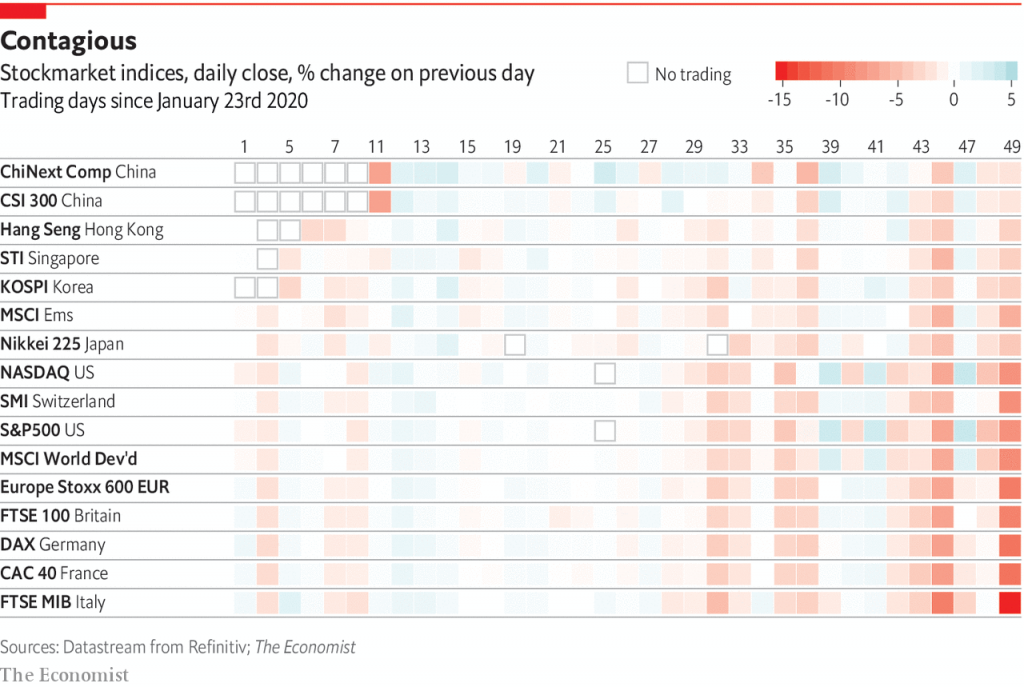

The rebound in Asian equities was bolstered by a view that Asian governments have performed well in containing Coronavirus, especially in China, South Korea, and Taiwan. However, there’re still unanswered questions about the degree of testing for COVID-19 performed in Southeast Asia. The Chinese equities bubble boosted regional inflows.

The development in the area resulted in investors making a bet that Asia will be a haven when the U.S. presidential elections may cause some price volatility this year irrespective of the risk of mounting Washington and Beijing tensions.

For example, Sebastien Galy, a senior macro strategist at Nordea Investment Funds SA who manages roughly 255 billion worth of assets said they have a great for Asian equities. He further anticipated that the growth theme will subsist even during September and October which would be a difficult time for equity markets.

The Resurgence Of Coronavirus In Some Parts Of Asia

The region’s level of the total world’s record fell below 20% when the infection first started in China and when the equity markets made 2020 lows in March, according to a show by Bloomberg and Johns Hopkins University.

That buoyancy may be tested by the reappearance of cases in legions of Asia that had previously contained the escalation of the virus spread. Hong Kong and Tokyo, for instance, have recently recorded fresh episodes of Coronavirus. Residents in Melbourne were asked to put on face masks as Victoria state recorded fresh 275 COVID-19 episodes.

In the meantime, India’s record has gone far beyond 1 million and this makes India the third country in the world that has a record of more than one million cases.

Asian Economic Recovery Vs U.S. Economic Recovery

Although most of the Asian economies have reopened roughly 70 to 95%, the majority of US state economies have opened 45 to 60% in June as revealed by Cushman & Wakefield’s global economic reopening tracker. This is when you consider factors like essential services, borders, schools, retail, and manufacturing.

Asia and especially Asian countries like China, South Korea, Taiwan have managed the virus fairly well and this resulted in economies that are showing quick recovery as revealed by Tuan Huynh, Deutsche Bank Wealth Management chief investment officer for Europe and Asia.

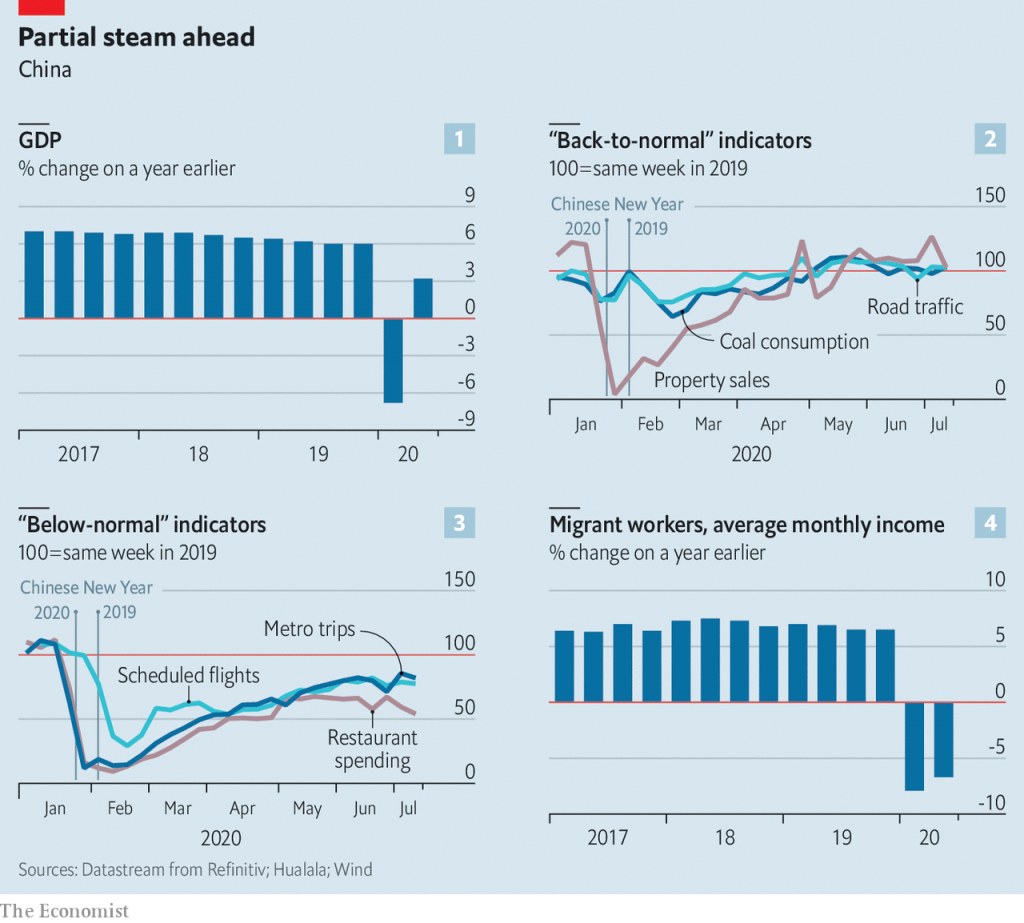

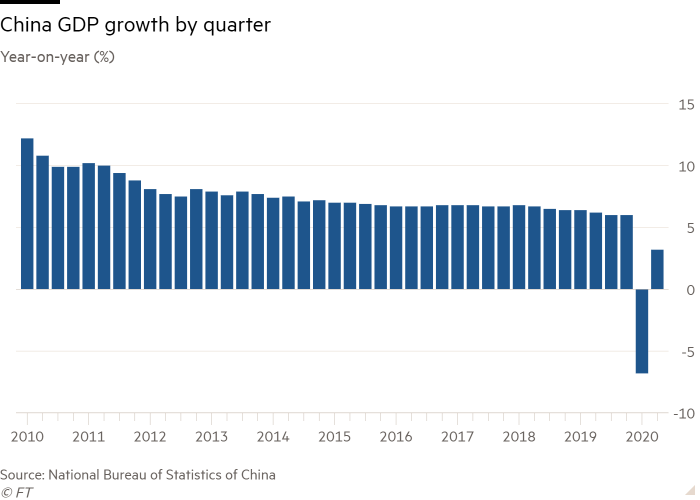

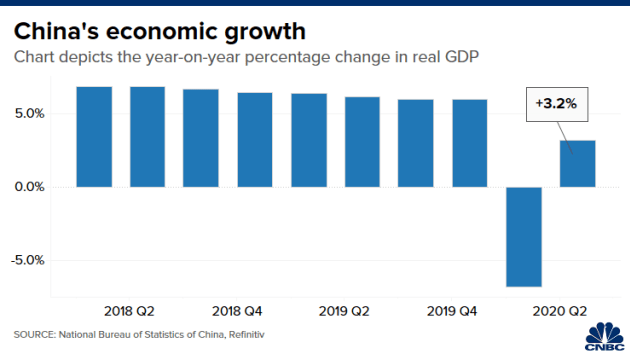

Some investors think the bullish trend in Asian Equities is mainly due to the economic recovery of China. The gross domestic product of China grew by 3.2% in the second quarter of 2020 compared to the past one-year record. The data reversed the first-quarter fall and beat expectations. Galy from Nordea Investment thinks that the Chinese economic rally will diffuse all through the Asia Pacific although the region will record a few months’ lags.

Asian Stocks Also Showed Attractive Valuations

Some analysts who favor possible positive trends for Asian stocks think that Asian stocks also have better valuations. They show the tendency for long-term growth opportunities and are likely to show a price rebound in the coming year as reported by Sumit Mangal, a fund manager at Goldman Sachs Asset Management. He thinks that Asian equities may show a strong demand recovery going forward.

Bloomberg data for the estimated return on equity show that Asian Stock valuations are far cheaper compared to the U.S., and European stocks while the ability of Asian stocks to yield return is double compared to the European and U.S stocks.

The MSCI Asia Pacific Index has shown a rebound of over 35% from the low rate it recorded in March. Yet, it may rise at the rate of roughly 10% in the coming year as revealed by Bloomberg analysts’ price forecasts. If this happens, it would outperform the projected 5% rise in U.S. , and European stocks.

That estimate was adjusted a little bit on Monday as investors likely weighed additional policy support and gear up in the earnings season.

Improved Risk-Reward Ratio

Asia stocks are cheap when you compare their return ratios with that of the western countries as the three charts below reveal:

iShares Asia 50 ETF (AIA)

:max_bytes(150000):strip_icc():format(webp)/aia_102219-c49a25463d3b4b85be94605bdf6599fd.jpg)

iShares MSCI China ETF (MCHI)

:max_bytes(150000):strip_icc():format(webp)/mchi_102219-b8a80053f69a4a1d8f56c57646556794.jpg)

iShares MSCI South Korea Capped ETF (EWY)

:max_bytes(150000):strip_icc():format(webp)/ewy_102219-dd3f88a017134a8e833b60fec2ba6150.jpg)

The U.S. Presidential Election And The Potential Effect On The United States Economy

While U.S stocks lag behind the Asian stocks due to the ripple effects of the present pandemic, investors around the world are equally beginning to factor in risks connected to the U.S. Upcoming presidential election. Analysts think that if Democrats succeed in the November election, the possibility for an earnings-depressing increase in taxation would be slim.

Growing anticipation that Democrats will lead in the coming election will slow the growth for the U.S. and European stocks while the election risks are unlikely to affect Asian equities.

Besides, the European stock market has some relationship with the U.S. Stock market. This makes the Asian stock market, except that of Japan lead the stock markets in other parts of the globe. Equities in Asia besides that of Japan are doing better than the U.S. Stock as the country approaches its presidential election. Asian stocks lead for three seasons out of the last four cycles with roughly 6% in four months up till the election time.