- Interest futures face strong volatility as markets shift their expectations for Fed policy following the Iran war.

- Short-dated contracts are pricing in odds of a rate hike by the end of 2026.

- Long-dated contracts remain stable, revealing a temporary phase caused by energy shocks.

Interest futures have seen a sharp and unusual price change this week. Traders have shifted from pricing rate cuts to hedging against the probability of policy tightening as an energy-driven inflation shock spreads through global markets.

Short-term contracts linked to near-term SOFR futures, especially expiring in June and September 2026, have seen implied yields rise sharply as traders quickly unwind bets on easing. Recent comments from central banks and market pricing show that futures markets now expect a rate hike this year. In fact, positioning even shows upside risks to policy rates.

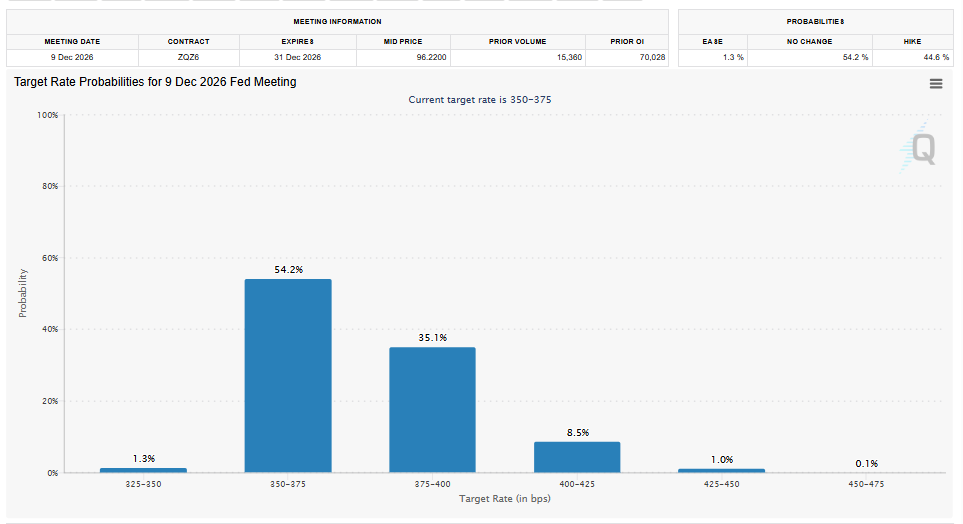

The change accelerated when the Iran conflict disrupted energy flows, sending oil prices above $100 per barrel and sparking renewed inflation fears. According to CME’s FedWatch tool, a 35% probability exists for a rate hike by year’s end, which was zero a week ago.

This price change has been most noticeable in front-end futures, where demand for hedging has grown as investors are unsure about what the Federal Reserve will do over the next 3 to 9 months. Options linked to these contracts are becoming increasingly biased toward higher-rate outcomes as investors are concerned that inflation could stay high for a long time, which could delay or even reverse the easing cycle.

On the other hand, longer-term contracts, such as the December 2028 and December 2030 SOFR futures, are still fairly stable. This suggests that rates will gradually return to normal once the energy shock wears off. This difference shows that the markets anticipate the current inflationary impulse is driven by supply fears and may not last long, even though it changes near-term policy expectations.

The steepening between short- and long-dated futures has gone much worse, showing that the story has changed from “cut cycle” to “higher-for-longer or even hike” risk. Analysts note that this situation is similar to past energy shocks, but there is one big difference: inflation has been high for a few years now, which makes it harder for central banks to act.

According to JP Morgan’s Michael Feroli, the Fed will keep rates on hold until 2026 and will likely hike rates in 2027. This shows that there is a growing gap between the market pricing and the baseline forecasts.

Short-term interest rate futures remain the main source of pressure. Every headline about inflation and energy causes prices to change quickly, while longer-term contracts still show confidence in eventual disinflation.

{kind=link}