- US stocks fell in February due to economic data and statements made by Fed officials.

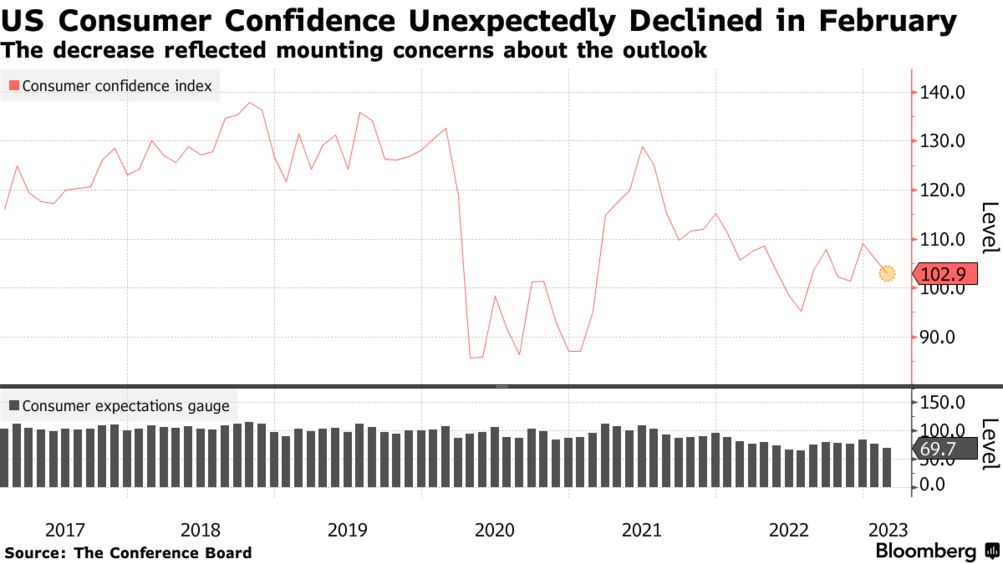

- The Conference Board’s consumer confidence index went down to 102.9 this month.

- European equities ended higher for the second consecutive month.

As investors continue to speculate about whether interest rates will stay high for an extended period, US equities concluded February in a muted manner. Each of the three major indices ended with monthly losses.

After performing well in January, stocks fell in February due to economic data and statements made by US Federal Reserve officials. These made market participants reevaluate the likelihood that the central bank would raise rates higher than anticipated and maintain them there longer than expected.

The S&P 500 dropped 2.61% for the month, the Dow dropped 4.19%, and the Nasdaq dropped 1.11%.

According to Fed fund futures, which predict that rates would peak at 5.4% by September, up from 4.57% now, traders have begun to factor in the likelihood of a more significant 50 basis-point rate hike in March. However, the probabilities remain modest at about 23%.

BofA Global Research warned that the Fed might increase interest rates to almost 6%.

Nevertheless, according to economic statistics released on Tuesday, consumer confidence unexpectedly declined in February, while a measure of property values slowed down even more in December.

The Conference Board’s consumer confidence index fell from 106.0 in January to 102.9 this month.

The two-year US Treasury yield, which usually changes with forecasts for interest rates, increased 2.3 basis points to 4.816%. The S&P 500 and Nasdaq were supported by a drop in yields after the economic report, but the two indices faded late in the day and ended lower.

Although European equities fell on Tuesday due to data from France and Spain suggesting that inflation was more persistent than anticipated, they ended the month higher for the second consecutive month. This was thanks to substantial increases in rate-sensitive banking stocks.

Investors expect the European Central Bank to increase rates by 50bps at its upcoming meeting in March, bringing the benchmark rate to 3%. In July, rates are anticipated to reach a peak of 4%.

All eyes are now on the preliminary consumer price inflation numbers for the entire euro area for February, which are coming on Thursday.