- Powell suggested the need to raise interest rates to control inflation.

- Europe’s STOXX 600 index achieved its best one-day performance in a month.

- China’s finance ministry cut the stamp duty on stock trades by half.

Equities rallied on Monday, driven by gains in 3M and Goldman Sachs. Moreover, the focus was on upcoming inflation and jobs data, pivotal for insights into the Federal Reserve’s interest rate trajectory. All three leading stock indices saw increases.

Investors processed recent remarks from Fed Chair Jerome Powell, suggesting the need to raise interest rates to control inflation. The spotlight now turns to two impending releases: the personal consumption expenditures price index, a loved inflation measure of the Fed, on Thursday, and the non-farm payrolls data set for Friday.

Ross Mayfield, an Investment Strategy Analyst at Baird, noted that while not overtly dovish, Powell’s comments still fostered a risk-on sentiment due to their non-hawkish nature.

Nvidia’s stock rose by 1.78%, dominating trading within the S&P 500 with a share value exchange of $31 billion. Major companies like Apple and Alphabet also saw gains, each adding 0.9%.

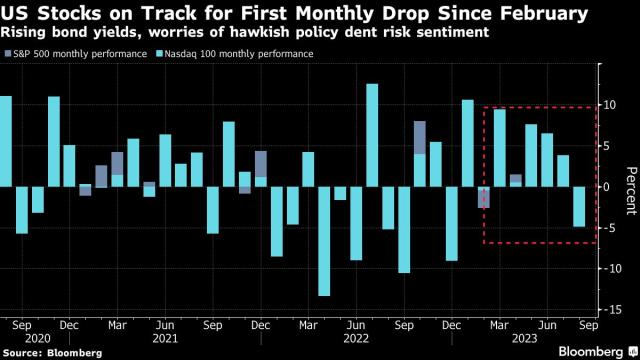

US stocks (Source: Bloomberg)

However, US stocks will likely close the month lower. That would mark the first monthly drop since February.

Meanwhile, European equities rose, with Europe’s STOXX 600 index achieving its best one-day performance in a month. This progress came as China-exposed industrial companies benefited from Beijing’s interventions to support its struggling stock market.

Market traders largely maintained their expectations of a pause in US interest rate hikes come September, despite Powell’s emphasis on the necessity for further increases at the Jackson Hole symposium.

European Central Bank policymaker Robert Holzmann suggested the possibility of another hike unless unexpected inflationary developments occur. Meanwhile, French Finance Minister Bruno Le Maire did not foresee a rate decrease over the upcoming months.

Automakers associated with China and industrial companies saw increases of 0.8% and 1.3%, respectively. This followed a decision by China’s finance ministry to cut the stamp duty on stock trades by half. This move aimed to stimulate the capital market and enhance investor assurance.

As August draws to a close, the STOXX 600 index is on track for its poorest performance this year. The decline has been primarily propelled by basic resource companies, negatively impacted by higher bond yields and a deteriorating economic forecast for the Eurozone and China, a key export market.