- The S&P downgraded credit ratings for various regional US lenders.

- The 10-year Treasury yield reached nearly 16-year highs overnight on expectations of higher rates for longer.

- Chipmakers led a surge in technology stocks before Nvidia’s earnings announcement.

US equities closed slightly lower on Tuesday as investors remained worried that the Federal Reserve would hold higher interest rates for an extended period. Simultaneously, bank shares experienced a decline. The financial sector dropped by 0.9%, causing the biggest drag on the S&P 500.

Moreover, the S&P downgraded credit ratings for various regional US lenders, impacting bank shares negatively. Consequently, the KBW regional banking index and the S&P 500 banks index fell by 2.7% and 2.4%, respectively.

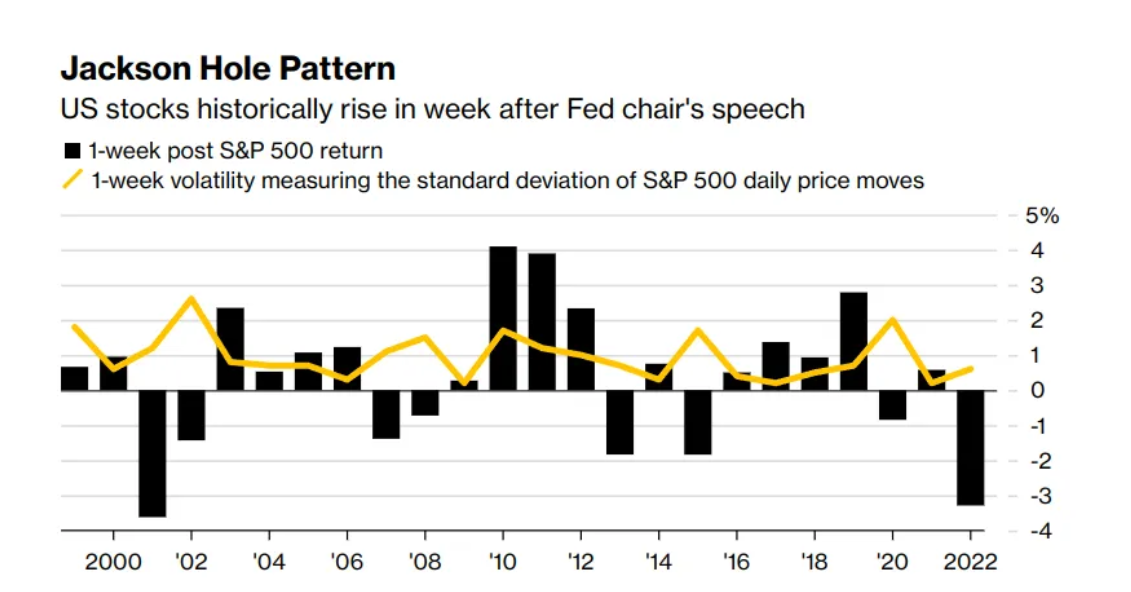

Jackson Hole Pattern (Source: Bloomberg Intelligence)

Investors anticipate greater clarity on the rate outlook during Fed Chair Jerome Powell’s speech at a central bankers’ meeting in Jackson Hole, Wyoming. Stocks have historically risen after such speeches. However, the 10-year Treasury yield reached nearly 16-year highs overnight due to the perception that the Fed might sustain higher rates. Elevated borrowing expenses can hinder business and consumer spending.

Additionally, investors eagerly awaited Nvidia’s results and forecasts, set to come out after the bell on Wednesday. Nvidia pleasantly surprised investors with a strong forecast in May, igniting a rally in its stock and other tech stocks fueled by optimism about artificial intelligence.

In Europe, equities extended their rebound on Tuesday. Chipmakers led a surge in technology stocks before Nvidia’s earnings announcement. Ubisoft also reached a three-week peak due to Activision’s plans to sell streaming rights to its “Call of Duty” game. The STOXX 600 index is on track for its toughest month this year, largely influenced by increasing bond yields across Europe, which impacted stocks in August.

According to Coghlan, there are no indications of a substantial recovery due to the negative sentiment. The economic structure lacks fundamental changes that could support a resurgence in stock values.

Coghlan noted that a better economic outlook in China, reduced interest rates by the Fed and ECB, and a ceasefire between Russia and Ukraine could potentially rescue European stocks from their current situation.

Despite the attractive valuation of the European equity market, a slowdown in global growth, as indicated by a Reuters poll, might offset these positive factors for the remainder of 2023. However, with easing price pressures, a more noticeable upturn in the market could come in 2024.