{kind=link}

- US interest rate futures saw a historic rise in open interest this month amid growing uncertainty about monetary policy.

- The Supreme Court’s ruling against Trump’s tariffs has made it harder to predict inflation, leaving the Fed in a quandary about whether to cut rates in June or later.

- Inverted SOFR futures suggest a higher probability of additional cuts in 2027.

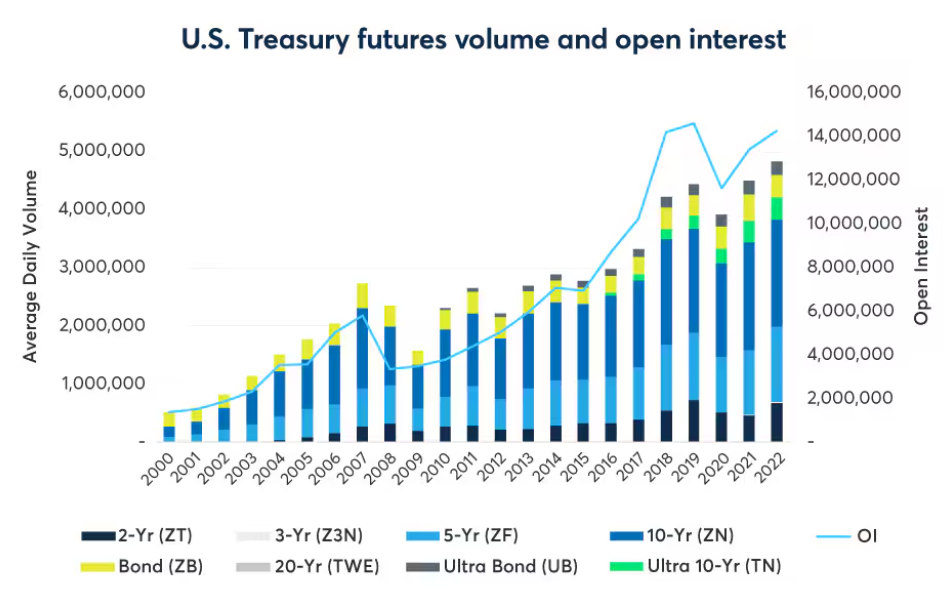

Open interest in US interest futures hit an all-time high in February as investors shifted their positions amid concerns about monetary policy, tariffs, and the economy. The CME Group, which runs the world’s largest derivatives market, said that open interest (OI) in its US Treasury futures and options reached an all-time high of 36,328,151 contracts on February 19. This beat the previous record of 35,120,066 contracts set in November 2025.

Agha Mirza, Global Head of Rates and OTC Products at CME Group, said, “With open interest surpassing 36 million contracts, clients are continuing to turn to our US Treasury markets in record numbers as uncertainty grows around monetary policy, government spending, and other inflationary pressures.”

A record number of investors participated across the yield curve. Futures and options for the 2-Year US Treasury Note OI rose to 5.8 million contracts, 5-Year Note futures rose to 7.9 million, Ten-Year Note futures and options rose to 12.6 million, while 30-Year Bond futures and options rose to 3.6 million. Recent regulatory data shows that the number of large open interest holders in US Treasury futures has also reached an all-time high of 2,100.

The increase in activity comes as traders in US interest futures rethink the Federal Reserve’s policy path after the Supreme Court struck down a wide range of Trump-era tariffs. The decision has made it harder to predict inflation and left policymakers arguing about whether to start cutting rates again in June or wait until later in the summer.

At the same time, futures spreads tied to the Secured Overnight Financing Rate (SOFR) have become much more inverted, which means that investors anticipate the easing cycle will last a long time. The 12-month difference between contracts for December 2026 and December 2027 recently dropped to negative 8 basis points. This shows that investors are now expecting more cuts instead of rate hikes in 2027.

The options markets are reflecting the same perspective. More than 400,000 contracts are now open for December-expiring 98.00 SOFR call options. This shows that people are hedging against the possibility that the policy rate will drop to 2% by the end of the year.

As volatility persists, market participants are increasingly relying on the liquidity and capital efficiency of exchange-traded interest rate products to navigate a changing macro landscape.