Systematic trading, equally referred to as mechanical trading is a way to set trading goals and manage risks and rules so that you can make orderly investment and trading decisions. Systematic trading includes manual trading of the system and full or partial automation with the use of a PC.

While technically structured systems are commonly available, there are equally systems that use fundamental data like short-term hedge funds and long-term stocks such as GTAA funds. Systematic trading can include high-frequency trading (HFT, occasionally referred to as Algorithmic Trading) and slow types of investments like following systematic trends. Another form of systematic trading is known as Passive Index Tracking.

The contradictory type of trade to systematic trading is discretionary trading. The downside of discretionary trading is that it’s controlled by emotions. Backtesting is difficult to do with discretionary trading, and risk management is less stringent.

Systematic trading is similar to quantitative trading which includes all quantitative methods of trading. Most quantitative trades use market-based valuation techniques such as derivatives. However, they use systematic or arbitrary trading decisions.

Strategy for doing systematic futures trading

Let’s say you want to simulate an index with futures and stocks from other markets with high liquidity. Example of system orientation:

1. Decide which stocks and futures you want to play with your fundamental analysis.

2. Analyze the correlation between the target index and the chosen stocks and futures and find the best strategy for the index.

3. Determine a consistent strategy for a dynamic combination of stocks and futures based on market data.

4. Try simulation of strategies including transaction costs, transfers, stop loss limits and any other risk control required.

5. Try the strategies while trading life, generate signals using algorithmic trading, and maximize profits and losses while continually managing risk.

Features of systematic trading

Using Irene Aldridge’s idea that described a particular HFT system, a more common type of systematic trading system ought to include the features below:

1. Data management (for real-time and historical data testing)

2. Signal generation system (generating, buying, and selling signals following a preset strategy with the use of a quantitative method)

3. A portfolio, loss, and income tracking system.

4. Quantitative risk management system (determining exposure for each market, group, or portfolio).

5. A trade execution and routing subsystem (which includes an execution trade algorithm such as TWAP, VWAP, and more, etc.)

Backtesting and systematic futures trading

The main aim of systematic trading is partially to use backtesting to test strategies and alternatives. Easy and reliable access to trading data is a fundamental aspect of backtesting.

Management of Risk

Systematic trading ought to account for the significance of risk management. It would need to utilize a systematic approach for quantifying risk, and utilize constant limits and techniques to determine how to end an overly risky trade position.

Systematic trading allows the trader to objectively set profit targets, loss points, trading volumes, and system closing points before the commencement of trading. This way, systematic trading allows for accurate risk management.

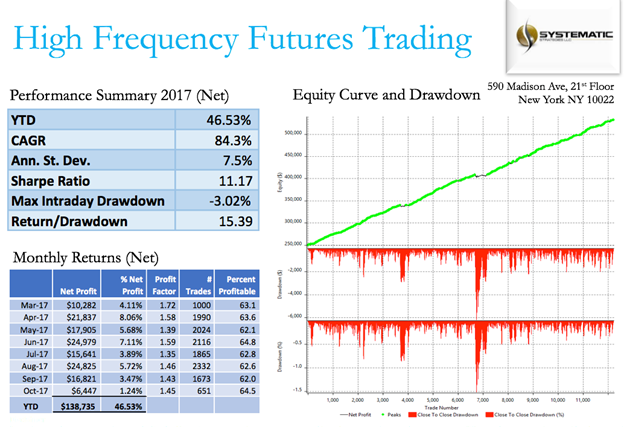

Systematic trading of future frequencies

In trading itself, Systematic strategies primarily concentrate on stocks and volatility, low frequency, and high-frequency strategies. Futures market trading focus on high-frequency trading, but you can equally use one or two low-frequency strategies that perform better, like WealthBuilder futures. The WealthBuilder offered by Collective 2 showed a great performance in 2017 with a net profit of 30% and a share of Sharpe of 3.4.

Designing a high-frequency strategy with a two-digit Sharpe ratio requires a combination of computational and simulation information. The microstructure of the future market is naturally very different from the microstructure of the stock or foreign exchange market and the components of the model, including the microstructure effect, vary greatly from product to product.

Also, whether the time is discrete or continuous wall time, transaction time, or other measures, there can be significant differences in how the model handles time. However, some of the simpler technical indicators we use, like moving averages, are common to multiple patterns across different underlying trading instruments and markets. Machine learning helps a lot in the majority of trading strategies, high-frequency trading strategy inclusive.

{kind=link}