{kind=link}

Regardless of the present global economic recession, coronavirus pandemic, and massive rate of unemployment, investors are still hopeful. Last Monday which was the same day that about 40 million workers lost their jobs and economists foretold that the gross domestic product would fall more than 40 percent in the second quarter, the Standard & Poor’s 500 stock index jumped 1.2 percent. The tech-laden Nasdaq Composite stock index made a new all-time high.

Since the 23rd of March, the S&P 500 has risen by 45 percent, and less than a month before that, the blue-chip index dropped by 34 percent which was the most rapid bear market in history. In Wall Street phrasing, a bear market is a loss of 20 percent or greater from a high, while a bull market is a gain of 20 percent or more from a low. Theoretically, we’ve already returned to a bull market.

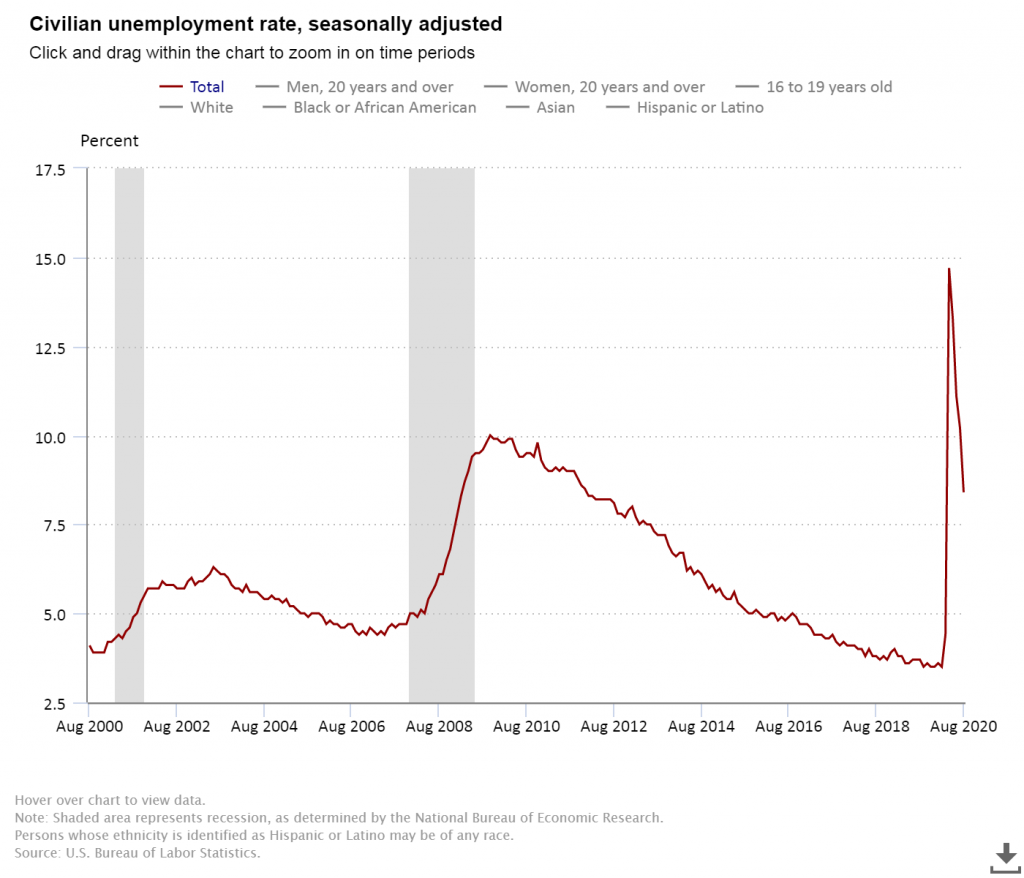

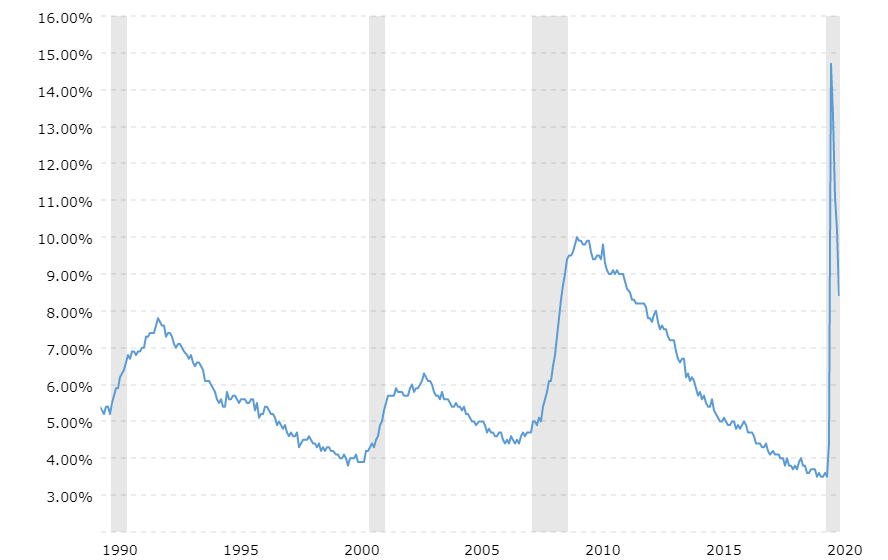

It is easy to understand the bear market part. Investors detest uncertainty and the coronavirus pandemic was such kind as it came in its largeness, halting or crashing global trade and businesses. Countries had to impose quarantines and in the United States by April, the unemployment rate climbed to 14.7 percent; a mass which had never been seen since the Great recession. Disruption in the chain of supply led to a reduction in basic needs like food, toilet paper, etc.

Why the bullish market?

Why the stock convention? “It all boils down to optimism that surrounds the revitalization of the economy as business gradually open their doors post lockdowns. Right now, the stock market is hopeful of a surge as investors foresee a speed in the economic recovery. America has returned to work gradually and the corporate earnings estimate which was slashed during the pandemic will probably be augmented soon.

Additionally, the Federal Reserve has reduced the short-term interest rates to almost zero, and the profit on the bellwether 10-year Treasury note stays less than 1 percent. With low-interest rates, businesses can borrow easily and develop themselves and that is why they are more than low-yielding CDs and bonds.

With the kind of air raging now, an indication of progress in things will lead to a celebration. For instance, the U.S. Bureau of Labour Statistics stated that the unemployment rate in May was constantly at 13.3 percent. The S&P 500 rallied 2.6 percent that day. Why? Because though a 13.3 percent unemployment rate is bad, it’s more preferable than the 14.7 percent unemployment rate of the month before — and isn’t comparable to the predictions of nearly every economist.

A review of the recent Trend

At a point when the coronavirus news grew worse in many US states, the stock market still saw an increase and made records. The reason for this growth was some certain achievements like the ability of other nations of the world to handle the pandemic, another potential round of stimulus to combat it, the accelerated development of treatments and vaccine candidates, and the relative importance of the most affected industries.

This was the first time the US stock market and the economy seemed to be deviating from each other ever since the market hit the bottom. Over the past few weeks the high rate of new cases of coronavirus diagnoses has resulted in a renewal of lockdown measures in some locations. It also caused delays in economy reopening in a few US states with viable and promising economy, like California, Texas, and Florida, for instance. The economic data of these locations make this fact visible and clear.

Homebase which is human-resources scheduling and tracking tool for small businesses provided data that showed a sharp decline in the number of employee hours worked in recent days, and the major declines were in states that had numerous cases of the COVID-19 pandemic.

The broader labor market stalled almost completely after it experienced a steady fall and heavy improvement in jobless claims. But stocks are not the economy, so why are markets uniting in the face of bad economic news? Some explanations are likely.

Why stock prices are still rising

First, the news on the coronavirus came in its abundance and it was as scary is it seemed. The market’s readiness to disregard the economic outcome can be traced to another measure of fiscal backup likely at the end of July.

As discussions are going on in Washington, they will probably put a deal into play, which would provide incentives for American households and business — together with an additional round of incentive checks, an extension of enhanced unemployment benefits, and more lending to small businesses. If there is a continuous supply of income to the economy, then the market may be ready to look ahead of poor economic outcomes at the moment.

Secondly, the coronavirus medical news is a quite two-steps-forward and one-step-back story. Of course, the rate of hopelessness in the news with steady increased hospitalizations reports is much but the news seems to be sensibly positive on the development of vaccine development and other treatments relating to permanent curing. If by the end of the year or early next year, a vaccine is extensively distributed, then everything will turn back to its normal way quite sooner.

Thirdly, the rest of the world, especially Europe, is flourishing. While parts of the US are gradually reopening, the reopening speed in Europe is quicker with a huge decline in cases.

And the comparative strength of the rest of the world in handling the pandemic is obvious in the market as well, as US stocks are performing less than them. The US is not leading but following a worldwide equity rally.

Uncertain outlook

Famous investor Benjamin Graham at one time contrasted the stock market to a very moody shopkeeper who increases prices one day and reduces them the next. In extreme uncertainty eras, those mood swings will possibly increase: The stock market has to feature in the itinerary of a formerly strange virus, the impending U.S. elections, and the projection of an economic revival.

Stovall is unwilling to call the current rally a full-blown bull market. “It’s a bull market with an asterisk,” he says. “I’d like to see it run for a full six months before we call it a true bull market.”

In March, investors received a vicious reminder of what a bear market is like following more than a decade of rising share prices. The stock market’s quick revival has supplied some reassurance. Jumping in and out of the market is a mug’s game: Few investors can time it right. It’s best to equal your investments with long-term goals — preferably, 10 years or more away — and invest little amounts at usual periods.

Conclusion

It’s not enough that the US economy is neither here nor there, but that the sectors most affected by the interference like the restaurants, movie theatres, parts of retail, etc, are not quite important to the US equity market or the economy at most.

The share of private GDP for restaurants, hotels, and recreation services without a doubt, is less than 5%. US equities mostly center on technology and industrials, not movies or dining out — Apple and Boeing, not AMC or your local mom-and-pop restaurant.

In summary, the US economy is a basis for being careful on US equities. But the domestic economy is just a part of the market’s feat. There seems to be adequate encouraging news below the surface to maintain the rally’s motion.