{kind=link}

- US interest futures reflect a higher-for-longer policy stance, as confirmed by the January FOMC minutes, keeping near-term Fed funds futures around 3.6% and offering limited pricing for significant rate decreases.

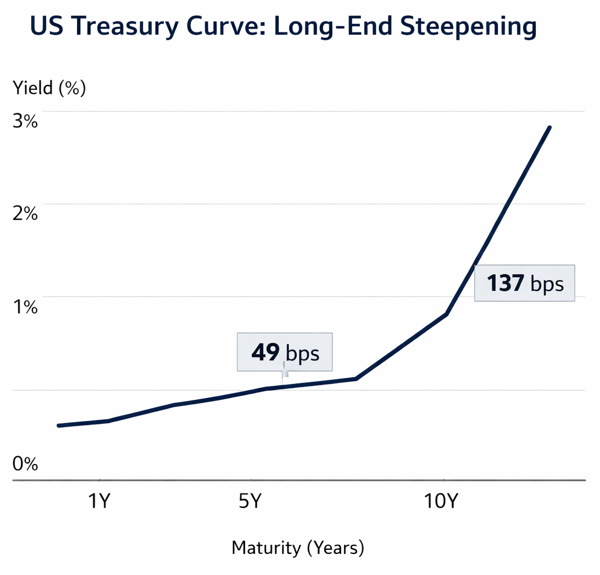

- The Treasury curve shows structural divergence, with a 49 bps slope from 1Y to 10Y and 137 bps from 10Y to 20Y.

- Markets are sensitive to economic data, but positioning suggests a gradual policy adjustment rather than a dramatic easing cycle.

US interest futures show the market has absorbed the Federal Reserve’s hawkish messages but remains highly sensitive to new data. The January FOMC minutes supported the idea that rates would stay high for a long time.

Policymakers voted to keep rates at 3.5%-3.75% and openly warned against easing too soon. Some members want to ease aggressively, while others strongly oppose it. This has led to unchanged near-term Fed funds futures prices.

Front-month contracts are hovering around 96.4, indicating an effective rate of around 3.6% until early 2026. Contracts for May and June, trading at around 96.425 and 96.48, show only minor implied drops. The small price difference between consecutive months suggests markets aren’t certain about making major cuts in the near future. The markets are pricing patience, not urgency. The Fed’s focus on sustained disinflation before easing has kept expectations steady and lowered volatility at the short end of the curve.

However, the structural story becomes clearer as you move further out of the curve. Long-term Treasury futures, especially 10-year contracts, have struggled amid higher yields. The slope of the 10- to 20-year curve is close to 137 basis points, while the slope of the 1- to 10-year curve is only 49 bps.

This steepening at longer tenors shows that investors don’t expect rates to return to where they were before the tightening. Traders are reluctant to extend their duration exposure, worried about structural inflation and the long-run viability of government spending.

Data sensitivity is the first test for futures pricing. Housing indicators, especially New Home Sales are important, as they are directly affected by interest rates. If housing data is weak, it could cause small price changes in the 3- to 6-month strip. This could push front-month contracts above 96.5 as traders add short-term cut probabilities. On the other hand, strong activity data would support the Fed’s asymmetric risk stance and strengthen the current structure.

The difference between low near-term cut expectations and high long-term yields suggests that the market as a whole expects the cuts to be small and limited. Under normal conditions, money market yields are close to 3.6% today and may drop slightly to 3.1% by the end of 2026.

For investors, this means that short-dated futures don’t offer much hedging value, but intermediate- and long-term futures are more important for tactical reasons, as they are in a higher-rate regime expected to last, not a cyclical downturn.