{kind=link}

- US interest rate futures reflect a later, milder easing cycle, suggesting a patient Fed.

- Meaningful easing risk only starts to be priced into the June (M26) and September (U26) Fed funds contracts.

- Upside yield risk remains in H26/M26 Fed funds and SR3M26 if inflation or wage data re‑accelerate or the Fed leans more hawkish.

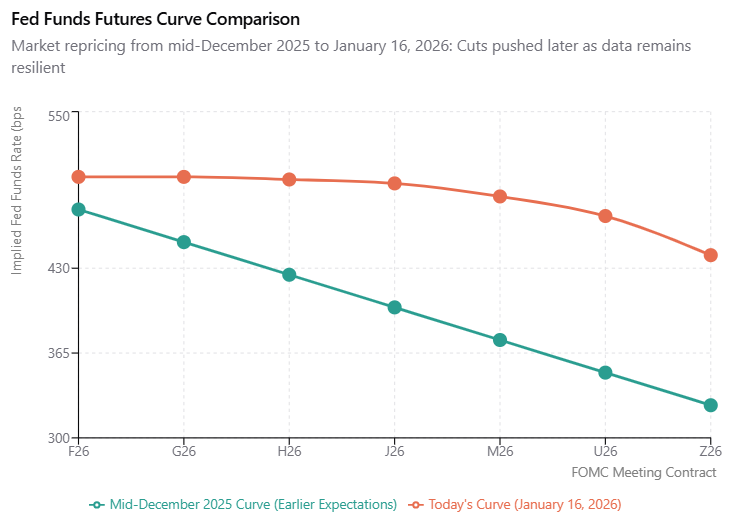

US interest futures are pointing to a “later and milder” easing cycle because markets now expect the Fed to be patient rather than make a quick change. The front of the Fed funds strip (F26 and G26 contracts running from January to March 2026) trades close to the current rates. So, the policy will likely stay the same for the first half of the year.

Meaningful easing risk only starts to be priced into the June (M26) and September (U26) Fed funds contracts. The implied yields dip modestly below today’s level, consistent with one or two 25-bps cuts by late 2026 rather than a rapid sequence of moves.

This repricing is anchored in stronger-than-expected US data and a labor market that remains tight. Lower‑than‑forecast Initial Jobless Claims and solid activity have pushed out the timing of cuts, squeezing out earlier and aggressive dovish bets. As a result, volatility has migrated along the curve; the very front contracts are now relatively pinned, while mid-2026 futures carry more event risk around each major data release and FOMC meeting.

Contracts in the 2026–2027 range on the SOFR curve (such as SR3M26, SR3U26, and SR3Z26) indicate that policy rates will decline slowly and steadily. Instead of a deep inversion, the strip slopes down gently. This is a classic soft landing setup. The markets think there is a chance of slower growth and easier policy, but it doesn’t go all the way to a recession-style cutting cycle. For traders, that helps with relative value setups like:

- Long mid-curve SOFR (like M26/U26) against short back contracts to show that cuts will happen, but not to the lows before COVID.

- Curve trades with butterflies around the M26–Z26 cluster to get ready for either a clear easing path or a long plateau.

The markets now price a cautious Fed, so new information must be genuinely surprising to shift the strip:

- Upside yield risk in H26/M26 Fed funds and SR3M26 if inflation or wage data re‑accelerate or the Fed leans more hawkish.

- Downside yield risk concentrated in M26–Z26 SOFR and U26–Z26 Fed funds if growth or labor data roll over decisively.