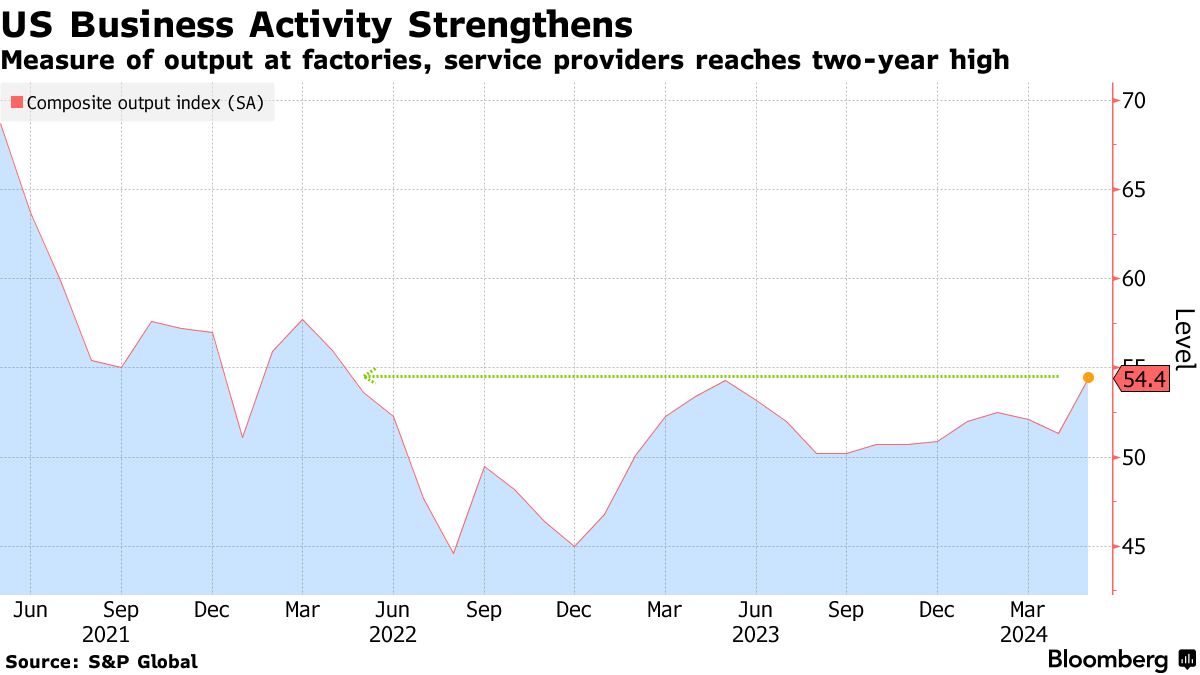

- S&P Global released its flash PMI reports for the US, which showed an improvement in business activity in May.

- Input prices soared in the US manufacturing sector, indicating a possible increase in goods inflation.

- Initial claims for unemployment in the US fell in the previous week.

Interest futures ended lower on Thursday as Treasury yields soared after positive US data. The rally in yields came as market participants lowered bets on Fed rate cuts. PMI data and weekly jobless claims pointed to a still robust economy, raising fears that the Fed might further delay rate cuts.

US business activity (Source: S&P Global)

On Thursday, S&P Global released its flash PMI reports for the US, which showed an improvement in business activity in May. The services PMI rose from 51.3 in April to 54.8. Meanwhile, the manufacturing sector increased slightly from 50.0 to 50.9. This led to a surge in the composite PMI to 54.4.

Furthermore, input prices soared in the manufacturing sector, indicating a possible increase in goods inflation in the future. This raised concerns that Fed policymakers might call for a longer rate-cut delay. As long as the economy remains resilient, there will be pressure on prices, keeping inflation and borrowing costs high.

Elsewhere, initial US unemployment claims fell in the previous week, a sign that the labor market remains tight. Data revealed 215,000 claims compared to economists’ expectations of 220,000. At the same time, layoffs remained low as employers held onto their workers. Labor market resilience is a significant concern among investors as it drives inflation. Economic demand and inflation increase if consumers have a lot of money to spend.

The last monthly employment report showed some deterioration in the labor market. However, policymakers cautioned markets against making premature conclusions. Therefore, there is always a chance that the previous resilience will continue. If it does, the likelihood of a Fed cut in September will keep falling, leading to higher yields and lower interest futures.

Notably, after these reports, the likelihood of a cut in September was 52.2%, down from 67% a week ago. Another cause for this decline was the hawkish Fed meeting minutes released earlier in the week. Markets were shocked to discover that policymakers were ready to hike interest rates if inflation remained stubborn. Moreover, although they believe inflation will ease, it might do so at a much slower rate than previously expected. Therefore, most called for a longer period of restrictive policy to tame inflation.

{kind=link}