{kind=link}

- Saudi is likely to extend its voluntary 1 million barrel per day cut into October.

- Moscow has agreed with OPEC+ partners to continue export cuts in October.

- The US August jobs data have raised expectations the Fed will pause this month.

On Monday, oil prices rose due to expectations that OPEC+ would maintain limited supplies and speculations of a halt to the aggressive interest rate hikes by the US Federal Reserve.

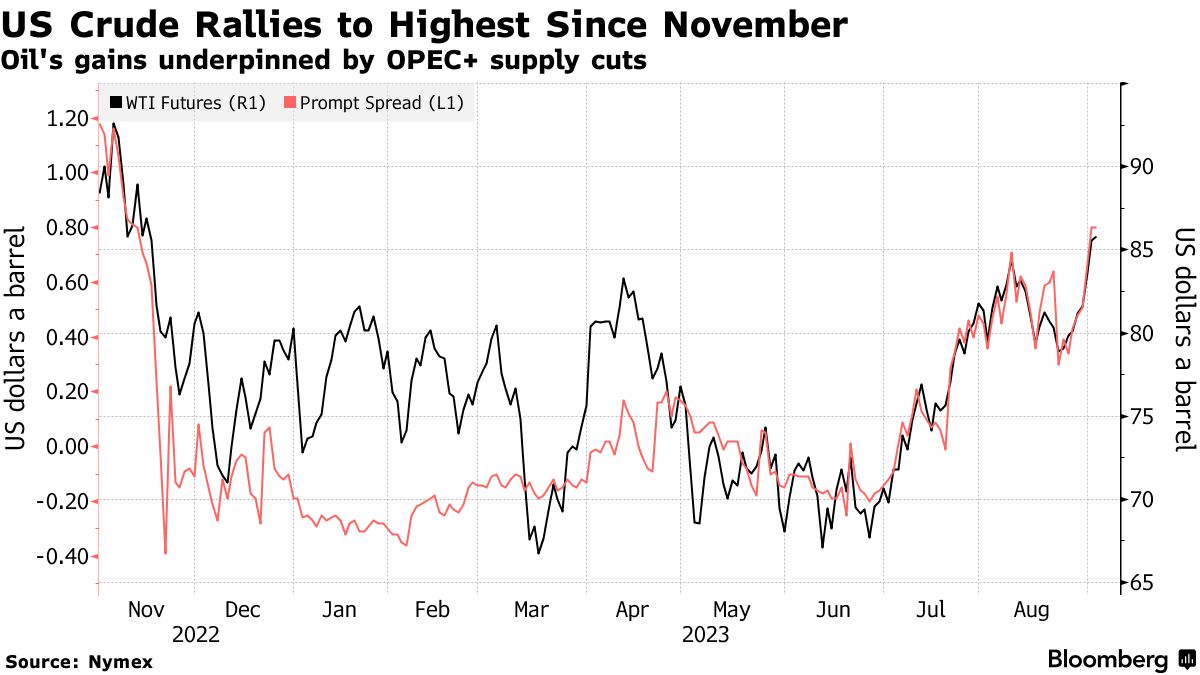

US crude rally (Source: Nymex)

Saudi Arabia led efforts to boost prices by implementing significant voluntary output cuts as part of the OPEC+ production agreement, which includes allies like Russia. The kingdom will likely extend its voluntary 1 million barrel per day cut into October, a fourth consecutive month. Typically, Saudi announces this before its official selling prices in the first week of the month.

Meanwhile, Russian Deputy Prime Minister Alexander Novak confirmed Moscow’s agreement with OPEC+ partners regarding continued export cuts in October. OANDA analyst Craig Erlam noted that while Saudi Arabia and Russia can withdraw the cuts, they are unlikely to do so hastily to avoid a price drop.

Russia, the world’s second-largest oil exporter, has reduced its output and exports alongside Saudi Arabia in addition to the ongoing OPEC+ reductions.

Brent crude futures for November settled at $89.00 per barrel, gaining 45 cents, while US West Texas Intermediate crude (WTI) October futures increased by 40 cents to reach $85.95.

Over the next six to eight weeks, global crude oil supplies will improve due to refinery maintenance. However, according to Russell Hardy, CEO of Vitol, the world’s largest independent oil trader, sour crude will remain scarce. Low inventories and inadequate investment in new oilfields make the oil market vulnerable to price spikes, warned a senior official at the global commodities trading firm Trafigura.

Additionally, the US August jobs data have raised expectations that the Fed will pause its interest rate hikes this month.

In China, unexpected growth in manufacturing activity in August and economic measures to support post-pandemic recovery have sparked optimism about increased demand in the world’s largest oil-importing nation.

In an unexpected turn, a private-sector survey on Friday revealed that China’s manufacturing sector expanded in August. The survey indicated improvements in supply, domestic demand, and employment, hinting at the possibility that government initiatives aimed at stimulating economic growth could be yielding results.

Specifically, the Caixin/S&P Global manufacturing purchasing managers’ index climbed to 51.0 in August, surpassing analysts’ predictions of 49.3.