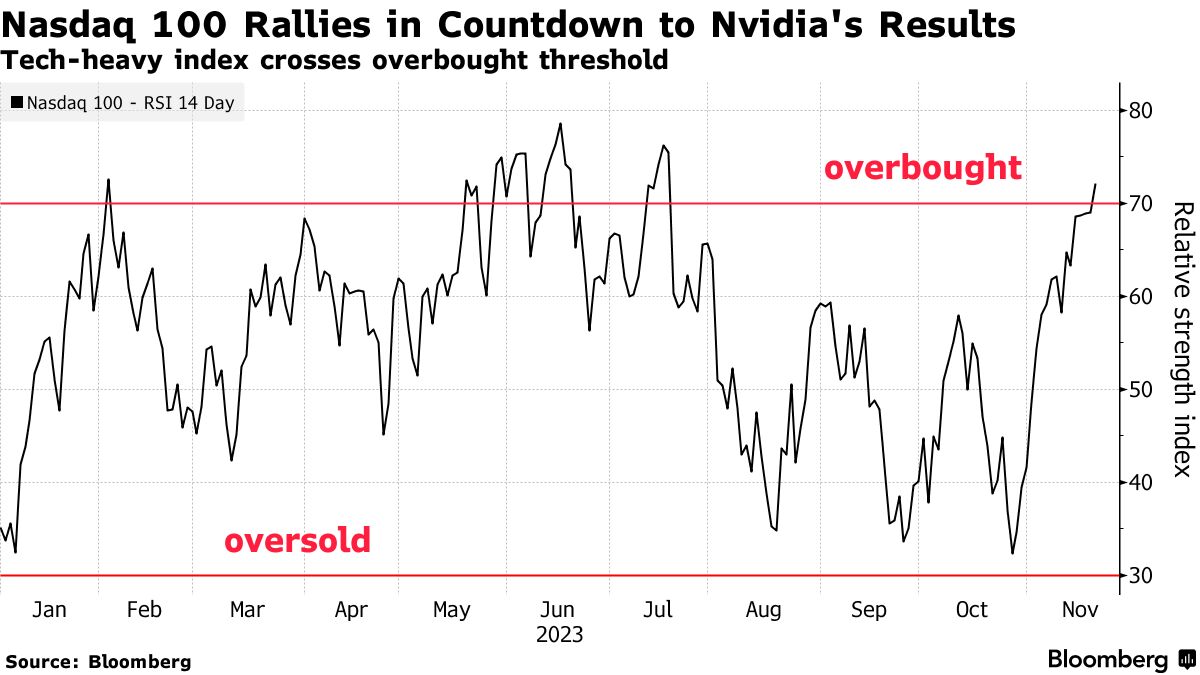

- The Nasdaq reached its highest closing level since July 31.

- Equities rebounded in November, supported by easing US inflation.

- The Fed will issue minutes of its November meeting on Tuesday.

On Monday, equities on Wall Street closed higher, with the Nasdaq leading the charge with a 1% rally, reaching its highest closing level since July 31. The S&P 500 also registered its highest close since Aug. 1. The Nasdaq rose because Microsoft hit a record high after hiring prominent artificial intelligence executives.

Microsoft CEO Satya Nadella announced that Sam Altman, the former head of OpenAI, would lead a new advanced AI research team at Microsoft. Greg Brockman, another OpenAI cofounder, and other researchers would join Microsoft. This news set a positive tone for the market, and heavyweight technology stocks like Nvidia and Apple gained ground.

In November, investors were pleased with better-than-expected earnings and falling Treasury yields. Moreover, Bruce Zaro from Granite Wealth Management noted that Wall Street’s main indexes rebounded in November, supported by easing US inflation and the belief that the Federal Reserve was done raising interest rates.

As Thursday’s US Thanksgiving holiday approaches, trading volume is typically thin. However, investors will have two key catalysts to watch.

Nasdaq 100 rally (Source: Bloomberg)

Firstly, chip designer Nvidia is set to release its quarterly report on Tuesday. The company’s stock is an excellent way to bet on the artificial intelligence industry. Nvidia’s results will mark the end of the earnings season for the “Magnificent Seven,” a group of mega-cap companies.

Secondly, the Fed will release minutes of its November meeting on Tuesday, providing clues on the direction of US interest rates.

Traders have almost entirely priced in the likelihood of the Fed holding current interest rates in December. Rate cuts might come as early as March, according to the CME Group’s FedWatch tool.

European equities edged higher on Monday after a strong week driven by aggressive bets on interest rate cuts. Despite market optimism, European Central Bank officials flagged still-high inflation and a somewhat resilient economy.

Data from the region showed producer prices falling along expectations in October, continuing a downward trend after September’s record fall.

Meanwhile, the UK’s FTSE 100 opened the week negatively as shares of equipment rental firm Ashtead Group plunged on a downbeat annual profit outlook. Investors awaited updates on the government’s fiscal policy later in the week. These include Britain’s budget deficit readings for October on Tuesday and the UK’s Autumn Statement on Wednesday.