- This week, Tesla and Netflix are scheduled to report their earnings.

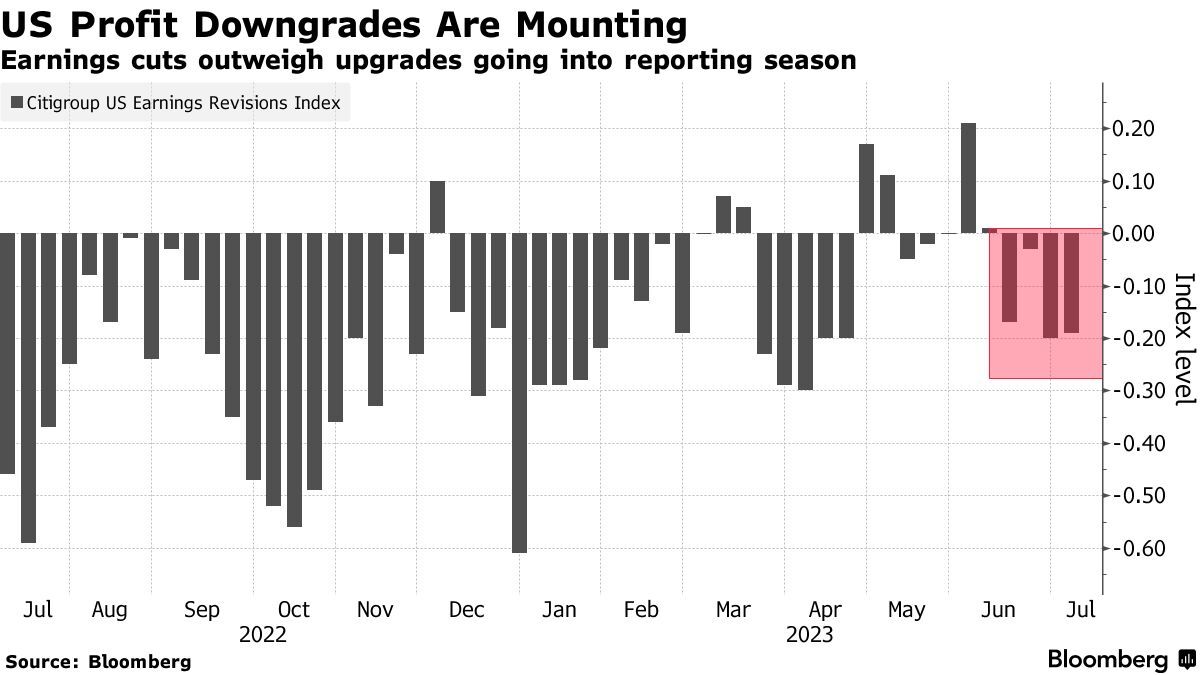

- US earnings for the quarter are expected to decline by 8.1%.

- European shares declined due to weak organic sales growth among luxury firms.

On Monday, financial and technology shares boosted US equities, resulting in a higher closing for the day. Investors were eager for the upcoming quarterly results, marking the acceleration of the earnings season. This week, Tesla and Netflix are scheduled to report their earnings.

Additionally, Bank of America, Morgan Stanley, and Goldman Sachs will post their results, following the reports from JP Morgan and Citigroup last week.

US earnings (Source: Bloomberg)

Investors will closely monitor the company outlooks as earnings for the quarter are expected to decline by 8.1%. This is a larger drop than the initial 5.7% decline predicted earlier this month, according to Refinitiv data.

Recently, equities experienced a rally, with the S&P 500 and Nasdaq reaching 15-month highs. This rally can be attributed to positive economic data indicating a resilient economy, including cooling inflation and a robust labor market. The market has largely factored in a 25-basis-point rate hike by the Federal Reserve at its upcoming policy meeting, with expectations currently standing at 97.3%l.

Conversely, European shares declined on Monday due to weak organic sales growth among luxury firms led by Richemont. Concerns about demand from China, the world’s second-largest economy, arose after lackluster economic growth figures.

Richemont experienced its largest one-day percentage fall in over a year, dropping 10.4%, primarily due to underperforming sales growth in the Americas during the first quarter.

Adding to the negative sentiment, data indicated that China’s economy grew sluggishly in the second quarter. This increases the pressure on policymakers to implement further stimulus measures.

The STOXX 600 index recorded its most significant weekly percentage gain since March’s end in the previous week. It was driven by hopes that the Federal Reserve would conclude its rate hike cycle shortly after July, considering the cooling of US inflation.

Elsewhere, British equities experienced a decline, primarily driven by a drop in mining stocks following disappointing economic data from China, the largest consumer of commodities. This downturn in the mining sector also caused metal prices to fall. Additionally, energy stocks mirrored the decline in crude prices.

The focus has now shifted to the upcoming release of UK consumer prices data scheduled for Wednesday.