- The dollar index fell 0.1% last week.

- There was a larger-than-anticipated surge in US nonfarm payrolls in September.

- The odds of a Fed rate hike are increasing.

On Friday, currency futures gained as the US dollar declined slightly against various currencies after the latest jobs report. The report indicated a widespread increase in US hiring for September but also highlighted a deceleration in wage growth.

For the week, the dollar index experienced a 0.1% decrease, ending an 11-week streak of gains. This streak had previously contributed to the dollar’s impressive 6% overall advance.

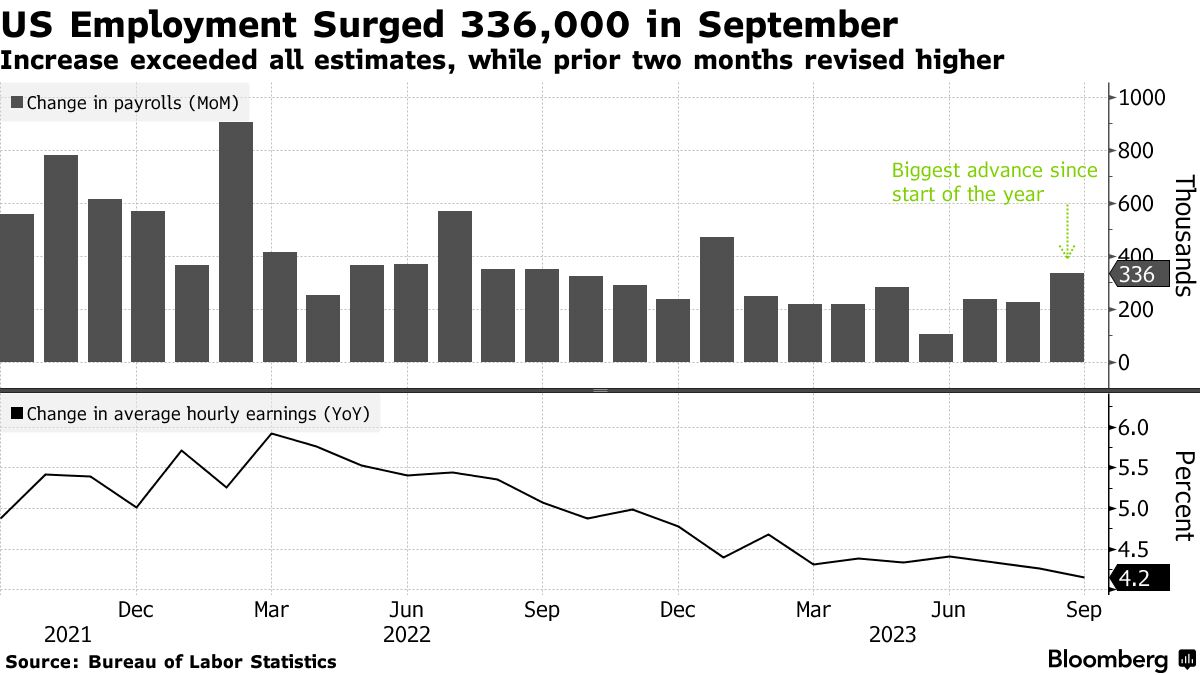

US employment (Source: Bureau of Labor Statistics)

In September, US employment saw its most significant increase in eight months, as hiring occurred broadly. It suggests a robust labor market, potentially providing the Federal Reserve with the means to raise interest rates again. However, wage growth is slowing down.

Last month, nonfarm payrolls expanded by 336,000 jobs, marking the most substantial increase since January. Additionally, the economy generated 119,000 more jobs than previously reported for July and August. This figure far exceeded the economists’ forecast of 170,000 jobs in a Reuters poll.

As a result of these developments, the dollar weakened, and US Treasury prices dropped.

The Labor Department’s recent employment report solidified expectations of accelerated economic activity in the third quarter. The labor market and the broader economy remain resilient, even 18 months after the US central bank began raising rates to manage demand.

Moreover, recent developments, such as the surge in job openings in August and the continued low number of first-time unemployment benefit applications in September, support the notion of a strong labor market.

This resilience indicates that monetary policy might stay tight for an extended period. Financial markets are currently leaning towards the Fed maintaining unchanged rates during its October 31-November 1 policy meeting. However, the odds of a rate hike are increasing, according to CME Group’s FedWatch tool. More clarity on the situation may emerge with the release of inflation data next week.

Since March 2022, the Fed has raised its benchmark overnight interest rate by 525 basis points, placing it within the current range of 5.25%-5.50%.

However, some economists believe the Fed has likely completed its rate hikes. This belief is primarily due to the significant increase in long-term US Treasury yields, reaching levels not seen in 16 years.