- This week’s focus is on the November jobs report.

- The S&P 500 achieved its highest close of the year on Friday after Powell’s remarks.

- There were concerns about an escalation in the Israel-Gaza conflict.

On Monday, US equities declined, breaking last week’s rally, as investors became cautious before this week’s employment data. The data could impact expectations of an early interest rate cut by the Federal Reserve next year.

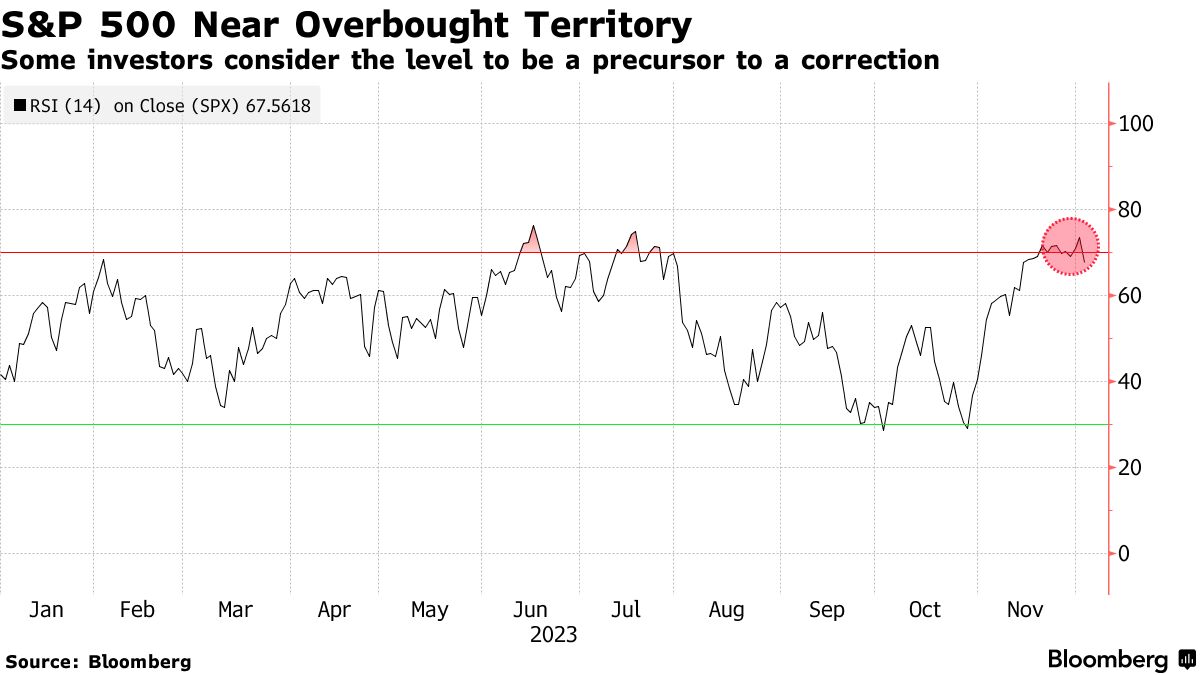

S&P 500 nearly overbought (Source: Bloomberg)

The S&P 500 achieved its highest close of the year on Friday after Fed Chair Jerome Powell’s comments suggested a careful approach. This reinforced expectations that the Fed has concluded its rate hikes. However, the index has reached overbought levels that could lead to a reversal.

This week, investors will focus on the November jobs report, influencing the outlook of the Fed’s future interest rate decisions. Traders widely predict the Fed will maintain current rates at its upcoming meeting. According to CME Group’s FedWatch tool, interest rate futures indicate a 58% chance of rate cuts starting by March 2024.

Moreover, concerns about an escalation in the Israel-Gaza conflict and an attack on commercial vessels in the Red Sea contributed to market declines.

Meanwhile, weak commodity prices affected Europe’s benchmark index, offsetting last week’s gains driven by expectations of interest rate cuts.

The pan-European STOXX 600 slipped 0.1% after reaching a four-month high earlier in the day and securing its third consecutive weekly gain on Friday. Investors are monitoring various data, including Eurozone PMI, producer prices, retail sales, and GDP, to assess inflation and economic prospects.

Europe’s STOXX 600, with a nearly 10% year-to-date increase, lags behind the US S&P 500’s 20% surge. Ipek Ozkardeskaya from Swissquote Bank anticipates European stocks will continue trailing US peers due to rate cut expectations. The Eurozone faces the likelihood of the ECB cutting rates before the Fed. At the same time, the US has maintained above-average growth, while Europe struggles with contraction or stagnation.

Elsewhere, Britain’s FTSE 100 retreated due to a decline in heavyweight energy and mining stocks. This drop came due to a stronger dollar and fears about China’s economy, which pressured oil and metal prices downward. The FTSE 100 declined by 0.2%, returning from its high close on October 19.

Simultaneously, the Bank of England will announce its next policy decision on December 14, with market expectations overwhelmingly leaning towards no change.