- The US equities remain near all-time highs, facing a crossroads of corporate earnings and macroeconomic factors.

- The corporate earnings for large-cap stocks have exceeded expectations amid positive sentiment.

- Fed’s meeting, along with US NFP and other key data, is vital to watch.

The US equities approach a vital week, facing a conflict of good corporate earnings on one end and tightening macroeconomic factors on the other. The S&P 500 and Nasdaq 100 are holding close to all-time highs, thanks to a bullish earnings season, sentiment around AI, and hope that the economy will achieve a soft landing. However, in the background are threats associated with monetary policy and geopolitics, all of which will open up potential volatility to the equity world.

The corporate earnings have been one of the props. More than 70% of S&P 500 companies that have already reported exceeded the expectations of analysts, and again, it is the large-cap tech to the fore. Mega-cap tickers such as Microsoft, Alphabet, and Tesla have reported good topline growth, confirming their leadership position in terms of cost savings and productivity due to AI incorporation. This has given rise to an optimistic sentiment and seen valuations rise to extreme levels, considering a macroeconomic ideal of moderate inflation, steady growth, and dovish policy.

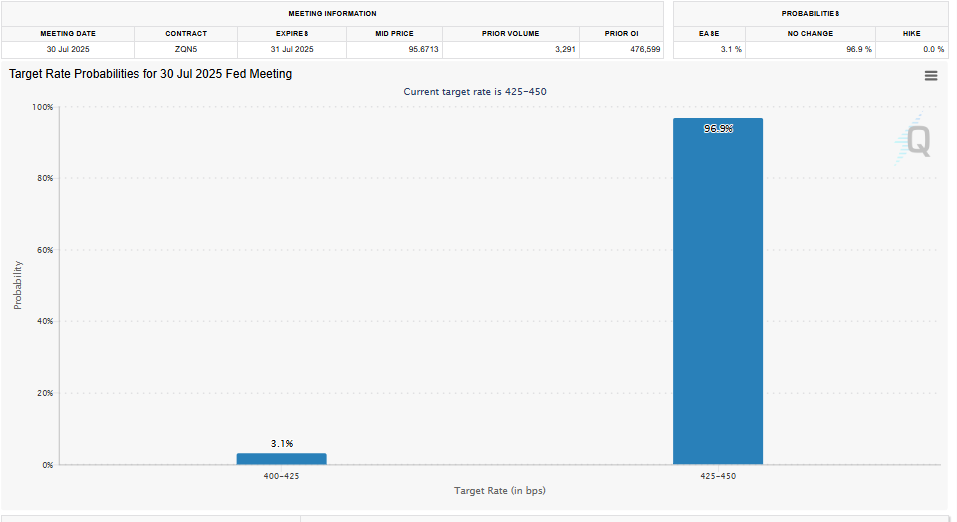

Nevertheless, the macro situation is more colorful. The Fed will leave rates unchanged this week, but investors are gradually growing more attentive to nuance when it comes to the Fed. Positive data on labor markets and stable consumer spending have cooled the chances of an imminent rate cut.

In the meantime, the geopolitical and trade events remain acting as wildcard variables. Although the new US-EU trade deal is good news for the global mood, it can have an asymmetrical impact on positive US capital flows. Economic negotiations between the US and China have also restarted this week, which could provide relief or more tension based on the results.

Signs of such changes are showing up in flows, even as technology, with money flowing into energy, industrials, and financials, the likes of which have traditionally done well with firm commodity prices and a rising bond yield. The Dow Jones Industrial Average, which had lagged earlier in the year, has started to recover as traders seek exposure to undervalued names that offer payouts during earnings stability.

Moving forward, Nonfarm Payrolls and Core PCE Index will be the next macro-heavy catalysts for the US equities. These will provide new information in terms of inflation pressures, employment trends, and the consumer economy in general. A deceleration in the rate of wage growth or a dovish tilt in the Fed might lengthen the rally, and an excessively hawkish tilt or hotter-than-expected numbers could shift to profit-taking.