- ECB’s Philip Lane cautioned that rapid rate cuts could spur new inflation.

- Traders anticipate around 150 basis points of ECB rate cuts this year.

- China’s central bank defied expectations by keeping the medium-term policy rate unchanged.

On Monday, European equities closed lower as government bond yields increased, following warnings from ECB officials against premature rate cuts. Meanwhile, the US equity market was closed due to a public holiday.

Government bond yields rose across the region after ECB’s chief economist Philip Lane cautioned on Saturday that rapid rate cuts could lead to new inflation.

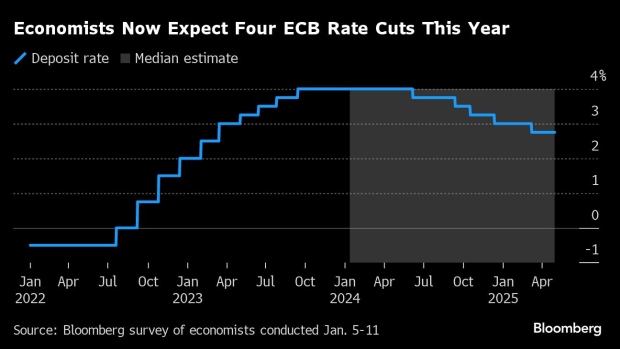

ECB rate cut expectations (Source: Bloomberg)

Meanwhile, economists expect about four rate cuts this year. Still, Bundesbank president Joachim Nagel, a known policy hawk, stated it was too early for the ECB to consider cutting interest rates.

Daniela Hathorn, senior market analyst at Capital.com, highlighted the gap between market expectations and central banks’ plans. Therefore, there might be downside pressure on European equities when expectations adjust.

Traders anticipate around 150 basis points of rate cuts this year, with over a 20% chance of the first cut occurring as early as March.

In economic news, Sweden’s headline inflation hit its lowest level since mid-2021 in December. Meanwhile, the German economy contracted by 0.3% in 2023 due to persistent inflation, high energy prices, and weak foreign demand. Moreover, the economy avoided a recession at the end of the year.

Elsewhere, China’s central bank defied expectations by keeping the medium-term policy rate unchanged.

Meanwhile, the UK’s FTSE 100 fell on Monday due to a sell-off in luxury and bank stocks. At the same time, poor corporate earnings forecasts weighed on FTSE 250 shares. Moreover, investors eagerly awaited British consumer price inflation data and December retail sales figures for insights into expected interest rate cuts. In the US, investors are closely monitoring US business activity data for January and December retail sales.

Notably, the Bank of England has maintained a relatively hawkish stance compared to the Fed and the ECB, sticking to a higher-for-longer policy rhetoric. Meanwhile, an industry survey showed that average asking prices for British homes have made the strongest start to the year since 2020. This suggests a potential recovery in the sector.

Between December 3 and January 6, the average price of homes listed for sale increased by 1.3% compared to the previous month. This marks the most significant December to January rise since 2020. Moreover, it was more than double the average increase during this period.