- Data on Friday showed that US job creation slowed down in June.

- Market participants raised the chances of a September Fed cut to around 79%.

- Investors eagerly await Powell’s testimony.

Equities closed at record highs on Monday as investors looked forward to several key events, including Powell’s testimony. The Nasdaq and the S&P 500 extended Friday’s rally when the US jobs report raised the chances of a Fed rate cut in September.

The market has more rate-cut optimism as economic reports consistently show a slowdown in the US economy. Data on Friday showed that job creation slowed down in June while the unemployment rate increased to a two-and-a-half-year high. At the same time, average hourly earnings eased. This indicates that the labor market is deteriorating amid high interest rates. Therefore, the Fed has less room to keep interest rates high for longer.

After the report, market participants raised the chances of a September Fed cut to around 79%. This means the US central bank might cut rates twice this year. However, policymakers have yet to indicate this. At the last meeting, they projected only one cut in December. Since then, data has come in consistently lower, showing weaker economic demand. Therefore, policymakers might also become more dovish.

As a result, investors are eagerly awaiting Powell’s testimony on Tuesday. If his message is dovish, equities could rally higher as rate-cut bets increase. In his last speech, the Fed Chair clearly saw signs that inflation would reach the 2% target. Therefore, there is a high chance this dovish tone will continue. However, if he remains cautious, there might be little impact as markets await the inflation report.

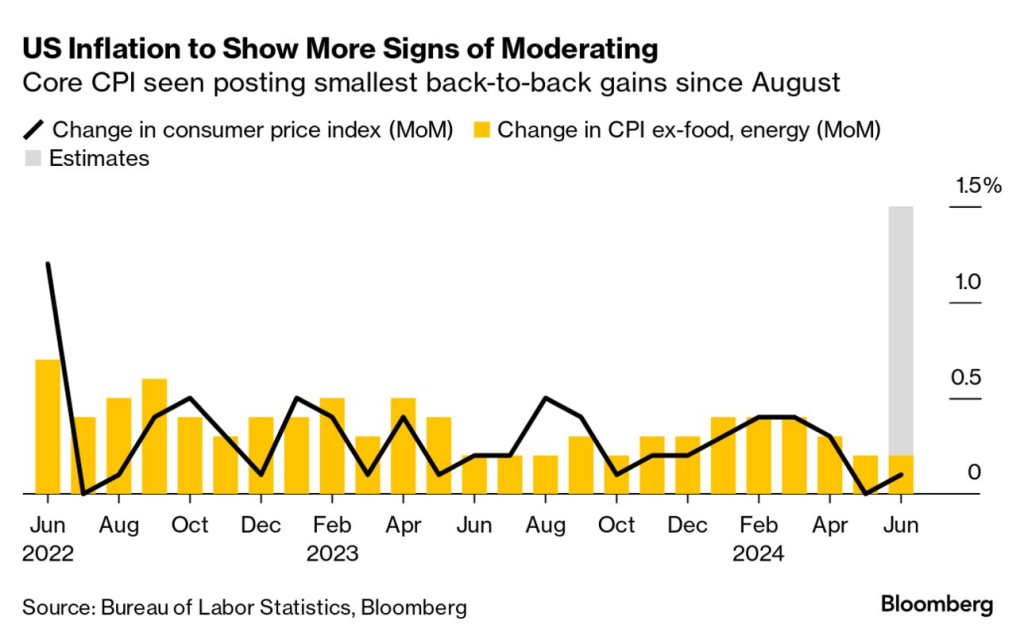

US inflation forecasts (Source: Bureau of Labor Statistics, Bloomberg)

The consumer inflation report on Thursday could further boost rate cut expectations. Experts believe inflation will ease further, with the annual headline figure falling from 3.3% to 3.1%. However, they expect the monthly figure to increase slightly from 0.0% to 0.1%. If the downtrend continues with this month’s inflation report, the Fed will be better positioned to lower borrowing costs in September.

Elsewhere, markets are preparing for the quarterly earnings season. Experts believe that S&P 500 earnings will increase 10.1% in Q2 from 8.2% in Q1. This would boost equities, which have enjoyed positive earnings reports this year. However, if earnings disappoint, the market could pull back or reverse.