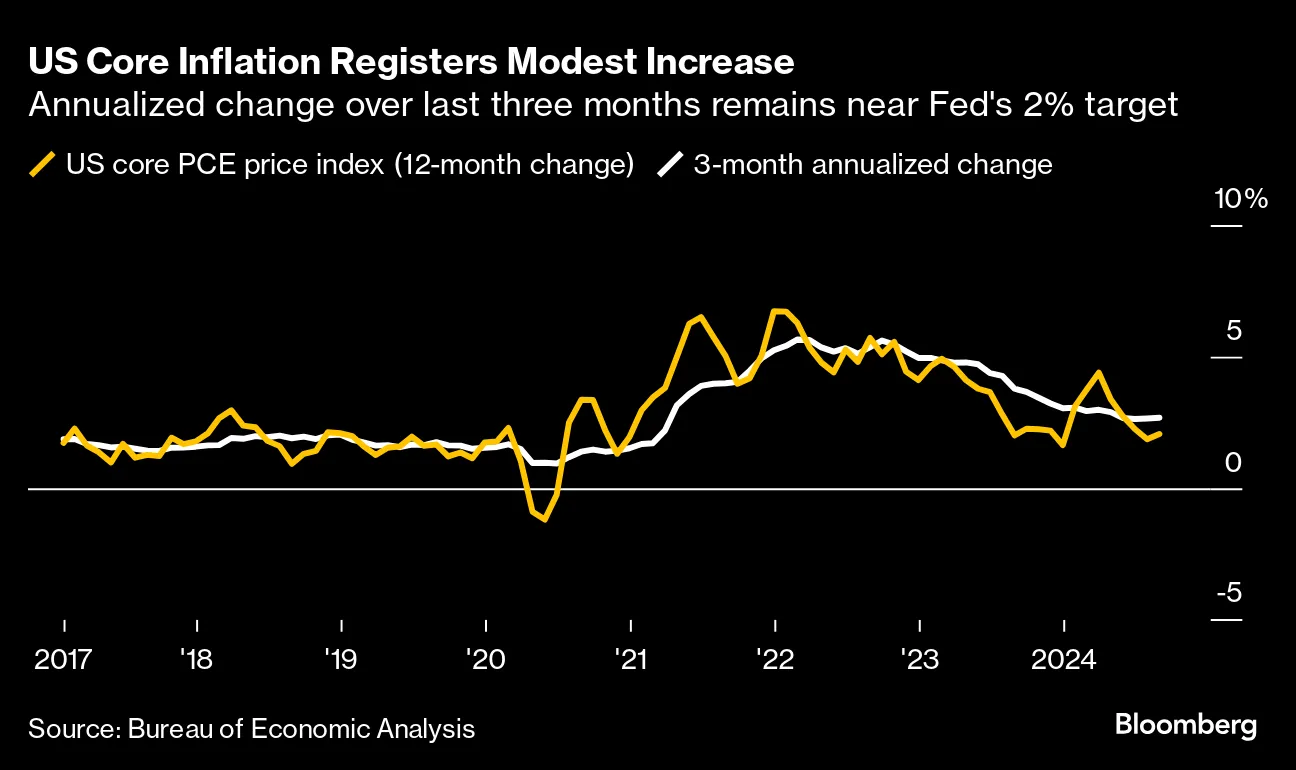

- The US core PCE price index report on Friday revealed a 0.1% increase in August, smaller than the forecast of 0.2%.

- Market participants raised the likelihood of a 50-bps November Fed rate cut from 49.9% to 56.7%.

- The US might add 144,000 jobs in September.

Currency futures were mixed on Friday and Monday amid several economic and political changes in different countries. Meanwhile, the dollar fell after inflation data revealed softer-than-expected numbers.

US core inflation (Source: Bureau of Economic Analysis)

The US core PCE price index report on Friday revealed a 0.1% increase in August, smaller than the forecast of 0.2%. Meanwhile, the annual figure fell from 2.5% to 2.2%, inching closer to the Fed’s 2% target. The same report showed that consumer spending rose by 0.2%, weaker than the previous increase of 0.5%. After the data, market participants raised the likelihood of a 50-bps November Fed rate cut from 49.9% to 56.7%.

Another massive cut from the Fed would weaken the dollar. At the last meeting, the US central bank delivered a 50-bps cut, noting it was meant to keep the unemployment rate low. Moreover, policymakers showed confidence in the progress on inflation.

All eyes are now on the US nonfarm payrolls this week. The US might add 144,000 jobs in September after a 142,000 increase in the previous month. Meanwhile, economists expect the unemployment rate to stay steady at 4.2%. If employment comes in lower than expected or the unemployment rate jumps, November rate cut bets will surge. At the same time, the dollar will collapse, allowing currency futures to rally.

On the other hand, if employment jumps and the unemployment rate holds steady or falls, market participants might increase bets for a smaller Fed rate cut.

The yen rallied on Friday after Shigeru Ishiba won the Primi Minster seat. The outcome boosted Japan’s currency since Ishiba supports rate hikes. Therefore, he might support the Bank of Japan as it increases borrowing costs.

Meanwhile, the euro collapsed after poor inflation figures from Spain and France. The result was an increase in ECB rate-cut bets. Markets moved to price a 90% chance of a cut in October. In Canada, data showed the GDP expanded more than expected in July. However, estimates for August were poor, supporting bets for a massive BoC rate cut in October. As a result, the Canadian dollar fell.