- There is a growing demand for safer assets due to concerns about China’s economy.

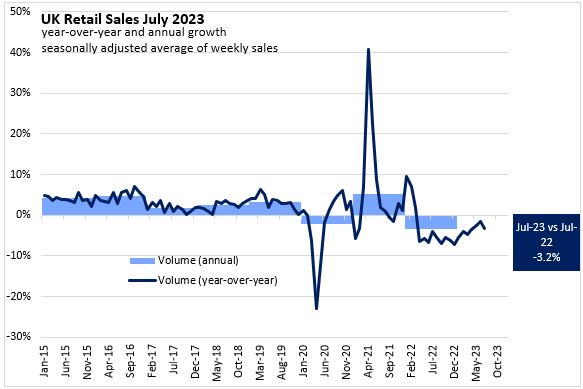

- British retailers reported a larger-than-anticipated decline in July sales.

- Newly released data from the UK, encompassing figures related to GDP and wages, has surpassed initial forecasts.

Currency futures ended mixed on Friday while the dollar closed a fifth week of gains, marking its longest winning streak in 15 months. The gains were driven by a growing demand for safer assets due to concerns about China’s economy and expectations of sustained high US interest rates.

China’s economic difficulties intensified as the property giant China Evergrande sought protection under Chapter 15 in a US bankruptcy court. Worries also escalated about potential defaults within China’s shadow banking sector. Investors boosted the dollar further due to unease over China’s insufficient efforts to stabilize its economy.

The yen’s depreciation kept traders alert to potential intervention by Japanese authorities. The Japanese yen strengthened against the dollar after hitting a nine-month low of 146.56 on Thursday. Historically, there has been a shift towards the yen in times of trouble in China, which typically strengthens it. However, that trend hasn’t held this time.

Last year, the dollar’s surge past 145 prompted the first yen-buying intervention by Japanese authorities in a generation.

Meanwhile, the Australian dollar, often seen as a gauge of China’s performance, increased slightly, following a nine-month low of $0.6365 on Thursday.

UK retail sales (Source: Nova Scotia Department of Finance)

Meanwhile, the British pound dropped as British retailers reported a larger-than-anticipated decline in July sales. Unfavorable weather conditions and the impact of high inflation and 14 consecutive interest rate hikes discouraged shoppers. Official data revealed that sales volumes in the previous month were 1.2% lower compared to June, surprising economists who had projected a 0.5% decrease.

The weakening of the pound stemmed from investor assessments of the extent to which the sales slump signaled a broader economic slowdown in the UK.

Newly released data from the UK, showing figures related to GDP and wages, have surpassed initial forecasts. This has led to increased anticipations in the market for additional interest rate hikes by the Bank of England. The indications of robust economic strength, concurrent with persistent inflation, have resulted in market projections of a peak of 6% for the UK’s primary interest rate. Currently, this benchmark rate rests at 5.25%.

Lastly, the euro slightly gained after hitting a six-week low on Thursday.