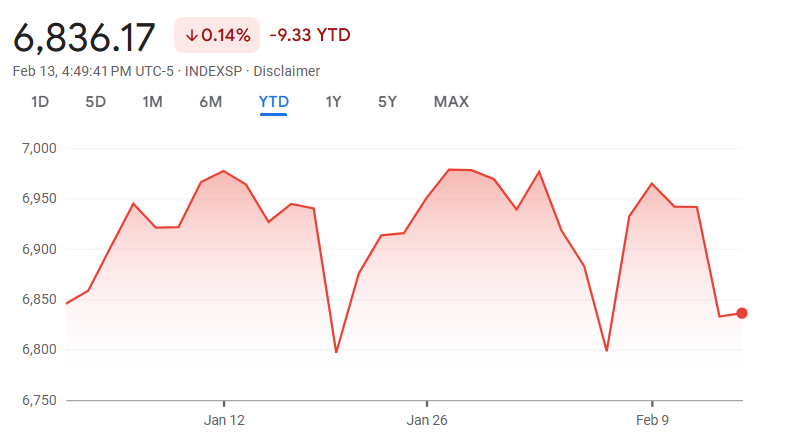

- US equities slipped on Monday’s low-volume day, with major indices continuing the decline.

- The tech sector, along with wealth management and transportation, struggled amid the potential impact of AI tools beyond growth.

- Markets remain attentive ahead of the FOMC meeting minutes, Core PCE, and other key data releases this week.

US equities fell slightly on Monday in a light trading day amid the US Presidents’ Day holiday. Investors were still wary of technology stocks and preparing for a week full of data that could test the strength of the long-running US equity bull run against the soaring overseas markets.

The Nasdaq 100 futures fell about 0.8%, the largest decline among major contracts. The S&P 500 futures fell about 0.5%, and the Dow Jones Industrial Average futures fell about 0.3%. The US cash markets were closed for Presidents’ Day, and many other global exchanges were also closed. This made liquidity tight, leading to low activity.

Later, selling spread from software to sectors such as wealth management and transportation, as portfolio managers considered how AI tools could affect business models beyond just top-line growth.

The S&P 500 lost about 1.4% over the week, the Nasdaq Composite lost 2.1%, and the Dow lost 1.2%. This means that both the S&P 500 and the Nasdaq are down for 2026. Futures trading on Monday suggested the tech sector could still be under pressure, as Nasdaq-100 contracts underperformed other benchmarks.

Now, market attention is focused on several US economic reports and Fed communications that could shift the market narrative on interest rate cuts. On Wednesday, the Federal Reserve will release the minutes of its January meeting, along with reports on durable goods orders and industrial production. On Thursday, we’ll get trade data for December. On Friday, we’ll get the PCE Price Index, the central bank’s preferred measure of inflation and an important factor in policymakers’ decisions on how long to keep borrowing costs high.

The upcoming data will reflect a global shift in market leadership. For over a decade, investors favored US stocks, but since early 2025, non-US markets have outperformed, and a rare “death cross” in relative performance emphasizes this change. These developments prompt questions about a lasting rotation away from US equities. This week’s numbers may confirm a new regime or offer US bulls temporary relief, as portfolios are still heavily weighted toward the US.

{kind=link}