- US interest futures remain under pressure as the odds of aggressive Fed cuts this year fade.

- SOFR contracts for June and September showed slight weakness, indicating a higher cost of funding over three months.

- The demand for 10-year futures (ZN) has decreased as investors focus on the medium-term outlook.

US interest futures fell slightly on Thursday as traders backed off bets that the Federal Reserve would cut rates more aggressively later in 2026, after economic data revealed significant improvement.

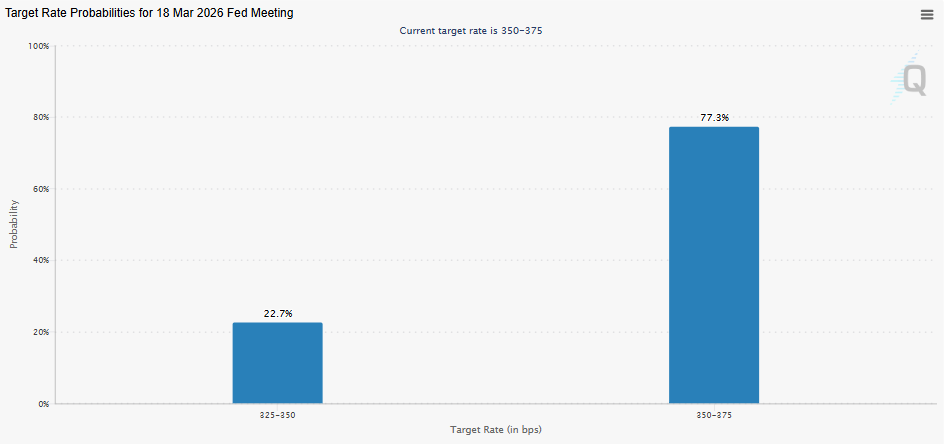

The CME Group’s 30-Day Federal Funds futures prices indicate the decreased probability of more than one cut since last week. Contracts ending in September and December 2026 now show a slightly higher expected policy rate. The move suggests that markets would rather see a slower, more gradual easing cycle than a series of quick cuts.

SOFR futures contracts, being the main short-term US dollar rate benchmark, showed the same change. The SOFR contracts for June 2026 and September 2026 declined slightly. It means the cost of funding for three months will rise slightly. This aligns with market expectations that the Fed might keep rates high for longer if growth and jobs remain strong.

As yields rose, 10-Year US Treasury Note futures (ZN) fell, indicating the reduced demand for long-duration contracts as investors reconsidered the medium-term rate outlook. The benchmark March 2026 and June 2026 10-year contracts are two of the most traded global interest rate futures.

Analysts note that the changes in Fed funds, SOFR, and Treasury futures are in line with a market that had previously priced in a very aggressive easing path but is now moving toward a more data-dependent stance. Positioning still lies in strategies that benefit from a steepening curve. Some leveraged funds prefer going short on front-end contracts while staying long on 10-year note futures to take advantage of any widening gap between short- and long-term yields.

Market participants will now pay closer attention to upcoming inflation data and the Fed’s communications to better gauge when and how quickly any policy change will occur. Until then, US interest rate futures are likely to remain volatile. Each major data release could significantly alter the expectations embedded in Fed funds, SOFR, and 10-year T-note contracts.

{kind=link}