- WTI futures slip as US-Iran talks ease fears of supply disruption.

- Recent dollar strength continues to cap the gains in oil and other commodities.

- US pressure on India to shift buying from Russia to the US and Venezuela, and inventory draws keep prices in equilibrium.

Crude oil futures fell to the $63.50 region after two days of gains, as talks between Iran and the US in Oman eased fears of a broader disruption in the Middle East. The move, as reported, shows the market’s sensitivity.

The risk premium can disappear quickly when diplomacy signals are strong and then return just as quickly when negotiations look shaky. Tehran focused on the nuclear file, while Washington sought a broader package. Because of this disagreement, volatility remains high, as a breakdown can shift regional supply risk prices in hours rather than weeks.

On the macro front, dollar-denominated commodities are down as the US dollar gains strength, thanks to hawkish Federal Reserve signals and slower-than-expected rate cuts. If disinflation stops, tighter policy for a longer time can stop rallies even when physical balances get tighter, because it’s harder to justify speculative length.

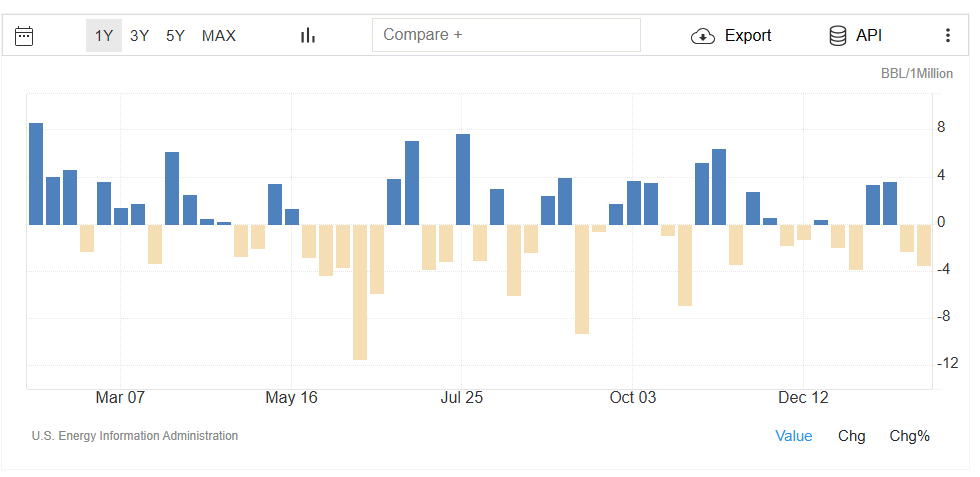

On the fundamentals, US crude stocks fell by about 3.5 million barrels to about 420.3 million barrels. This is nearly 4% less than the five-year average for this time of year. The draw was larger than expected due to winter storms disrupting supply flows.

Meanwhile, the product data were mixed; gasoline inventories rose slightly, distillate inventories fell sharply, and implied demand (total products supplied) rose YoY. In short, the crude draw supports price floors near current levels, but uneven product signals make it hard for a breakout to hold.

The political factor with the greatest effect on the structure is President Trump’s claim that India will switch from buying Russian crude oil to purchasing oil from the US and Venezuela in exchange for lower tariffs (from 50% to 18%). India hasn’t publicly confirmed the promise, and Russia says it hasn’t heard anything about it either.

Even if India wanted to leave quickly, Russian barrels have been significantly discounted (Urals are about $10-20 below Brent), which helps India’s refinery margins. Replacing them with US or Venezuelan crude probably raises delivered costs due to narrower discounts, higher freight costs, and (for Venezuela) a heavier, higher-sulfur grade that requires more complex refining and blending.

Venezuela’s capacity is another problem. Its production of almost 1 million barrels per day (bpd) can’t fully offset India’s recent Russian intake of about 1.1 million bpd, let alone its previous highs. A full pivot could lead to higher global freight rates, more “shadow” trade, and a higher import bill for India, estimated at $9-11 billion a year. This would keep a medium-term risk premium in crude.

{kind=link}