{kind=link}

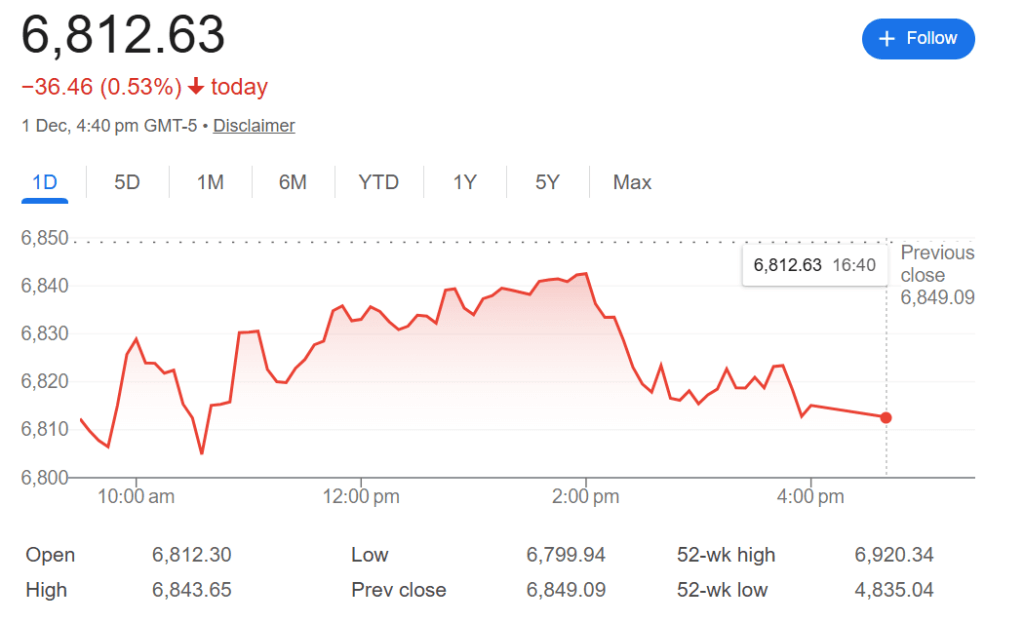

- US equities remained flat on Monday after a significant pullback ended the previous week’s winning streak.

- Weakening risk appetite, cryptocurrency slump, and overstretched valuations could continue to weigh on equities.

- Fed easing probability increased to 87%, keeping investors’ optimism alive.

US equities remained broadly flat on Monday, stabilizing after a pullback ending the previous week’s 5-day winning streak. Dow Jones, S&P 500, and Nasdaq 100 remained near unchanged levels, revealing a cautious tone after weakening risk appetite and growing uncertainty.

The broader sell-off on Monday was triggered by concerns about inflation, stretched valuations in the tech sector, and doubts about the sustainability of AI-linked capital expenditures. The slump in cryptocurrencies also added to the risk-off tone. Bitcoin’s 6% value loss dragged Coinbase and Robinhood lower by 4%. Tech giants that fueled the November rally also faltered, like Alphabet lost 1.7% while Palantir and Broadcom also declined following the cooling AI trade.

Despite the downturn, market participants are still eying catalysts that could revive the momentum by the end of year. The markets are now anticipating around 87% probability of a 25 bps rate cut in December, a dramatic shift from mid-November expectations. Analysts argue that seasonality and improved breadth continue to keep the equities underpinned. December remains the third strongest month since 1950 for the S&P 500, giving more than 1% gain.

However, Monday’s market reaction showed mounting caution as global equities retreated, with the MSCI World Index down 0.4%, and the Stoxx 600 down by 0.2%. Healthcare, utilities, and industrials led losses while energy stocks firmed up as crude oil gained more than 1% as OPEC+ confirmed no supply hike in early 2026.

Treasury yields surged across the curve, with 10-year yields rising to 4.09% and 2-year yields gaining to 3.54%, adding pressure to equities. The ISM Manufacturing PMI fell for the ninth consecutive month to 48.2, igniting fears of recession. The markets are now awaiting the ISM Services PMI and the delayed Core PCE Index for more impetus. However, the major focus still remains on the Fed’s December meeting, which will provide clarity on the monetary policy path.