The message is clear for investors when the euro is strong: a safer bet amidst the chaos of the U.S. The eurozone economy currently has a promising picture for the coming months. While the rest of the world struggles to switch gears, the UE policies may be taking the lead.

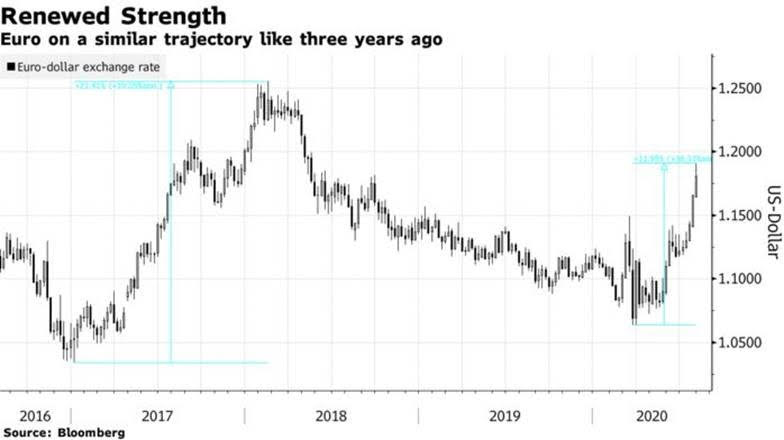

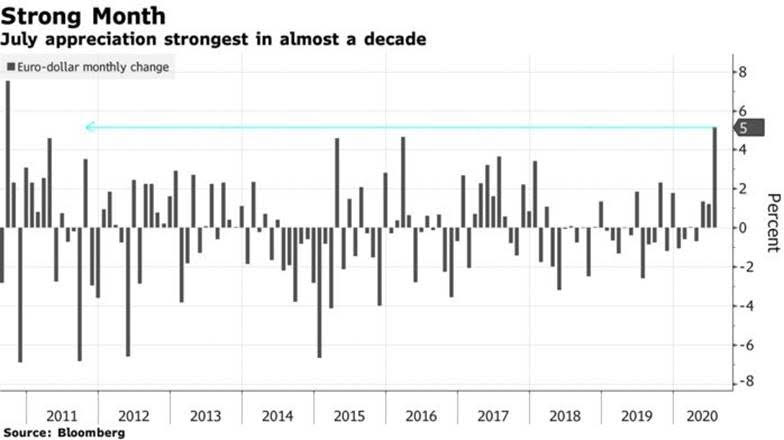

Last month, the euro had a 5-percentage point lead over the dollar-the largest monthly advantage since Q2 2010. Moreover, the current tendency is close to levels of 2017 that caused havoc in the stock markets due to the percentage distancing between both currencies. However, the euro stability is the top antagonist of the European exporting industry. When the euro is stronger, the value of revenues in the U.S. decreases and so does the international demand for products manufactured in dollar-fueled countries.

Berndt Maisch, a senior manager at Tresides Asset Management GmbH in Stuttgart, has declared that a stronger euro is negative for the corporate profits within export-driven companies. On the other side, the rising confidence in the UE outweighs the detriments – he added.

Recent figures point out that the eurozone ramped into an economic downfall in Q2. The U.S. is not doing better, though, and there could be signs of spiraling out of control. The latest USD movements reflect relentless fragility. In words of Maisch, the country could be “losing its grip on the virus pandemic”. Another indicator of this plunge is the Bloomberg Dollar Index (BBDXY), a parameter that compares USD with another 10 currencies, which has had historic lowest records of a decade in July close to levels of 2018.

According to Maisch, the euro is still away from the inflection point where it can force the industry to reassess investment in foreign assets or influence in stock allocation decisions. “The move is currently still too small for that”, he said. In any case, a weak dollar is an indicator of an intrinsic slowdown in the U.S economy.

Although there is the idea that a stronger euro is detrimental for European assets, it is not enough to keep the other regions into stalling global trade, said Stefanie Holtze-Jen, chief currency strategist at DWS Group. Regarding stocks, the decision is also dependent on an optimistic macro outlook, she added.

Vincent Manuel, chief investment officer at Indosuez Wealth Management, explained that although the current percentage separation may not be causing sleep deprivation just yet, it very well could later. The current trend could become a burden for EU equities and mostly for international companies with a high rate of dollar-backed cash flows – continued Manuel.

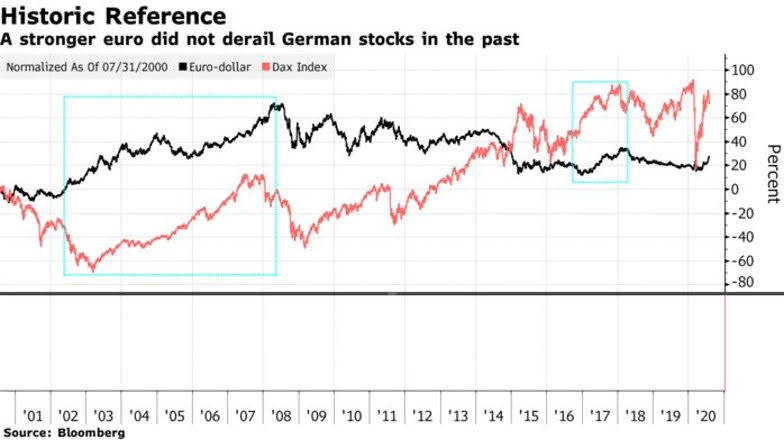

There is a recent precedent from 2017 when the European equities crippled after the French election and a speech by Mario Draghi. But some experts think a currency move of this kind, the impact on stocks, and the historic performance is nothing to be concerned about.

Valerie Gastaldy, Day by Day strategist, stated that “there are many myths on financial markets.” Then, she added that “one of them [myths] is that a strong euro is a problem for European equities. This may sound logical, but it is not confirmed by facts.” To back this statement, she pointed out the mirroring between the euro and the German stock performance since 2000. Moreover, she added that it is to be expected to have this behavior started next year or be in action now already.

DWS’s Holtze-Jen claimed that it could be the stocks having and effect on currencies rather than the other way around. Market trends have a similar outline than those of 10 years ago. There are gaps between the American and the European bond yields closing. Whenever the potential yield earned by shifting from one currency to another relates no significant difference, the moves are driven mostly by risk sentiment. For instance, a major decision influencer is a thrive for equities. By looking at 45 currency pairs of the G10 currencies, we can only find seven pairs moving without correlation with equity markets, she added.

Thus, so many currencies move correlated to equity markets that investors make use of them as a portfolio hedge instead of considering their impact over equity prices, stated Holtze-Jen. “In a multi-asset perspective, currencies are amazing and effective in systematical management risk” – she added.