The economic growth of countries is estimated through their GDP, which is determined by two components: population growth and productivity of labor. The productivity of labor shows the ability for enhanced output from the available amount of labor in the economy.

US Dollar (USD)

The announcement also provided support to the USD, against the precious metal haven. However, UST earnings continued to remain dampened. There are still high anticipations on the continual argument over the country’s 4th stimulus package on Capitol Hill.

According to BBG, Kudlow, a White House economic advisor this positive growth shows that the job market will continue to make a positive recovery. It equally shows a possibility for single-digit unemployment close to election time and indicates a self-sustaining recovery.

Although the economy doesn’t appear to be recording great stimulus progress, there are anticipations that President Trump will issue an executive order on the payroll tax cut. Also, there are hopes for formal and informal tax relief talks.

Euro (EUR)

The common currency unit of the European Union lost its gains against the USD all through Friday’s trading session. This move is in line with broad risk aversion experienced during the previous time zones. It moved down to the mid-1.17s following the release of the US’s job report that surpassed anticipations.

Industrial output in the region has climbed in conjunction with factory demand and there has been an increasing signal for fast economic recovery in the region. Nonetheless, the sudden rise in geopolitical tension in the region dominated the released data.

According to La Repubblica, Italy makes moves to cut labor tax for businesses in the south to boost production and generate fresh jobs. Der Spiegel stated Germany’s intention to boost stimulus spending from 16 billion EURO to 26 billion EURO. Previously 10bln EURO was allocated to digital, security, and defense-related investments.

British Pound (GBP)

According to ITFX, the UK’s Chancellor, Sunak said that they would be borrowing a huge amount because of the costs of support. Majorities of people recognize that the furlough program is less than sustainable overtime.

BBG report shows that UK Trade Sec Truss noted that UK’s trade negotiations with Japan were positive and the two countries hoped to reach a formal agreement before the end of August.

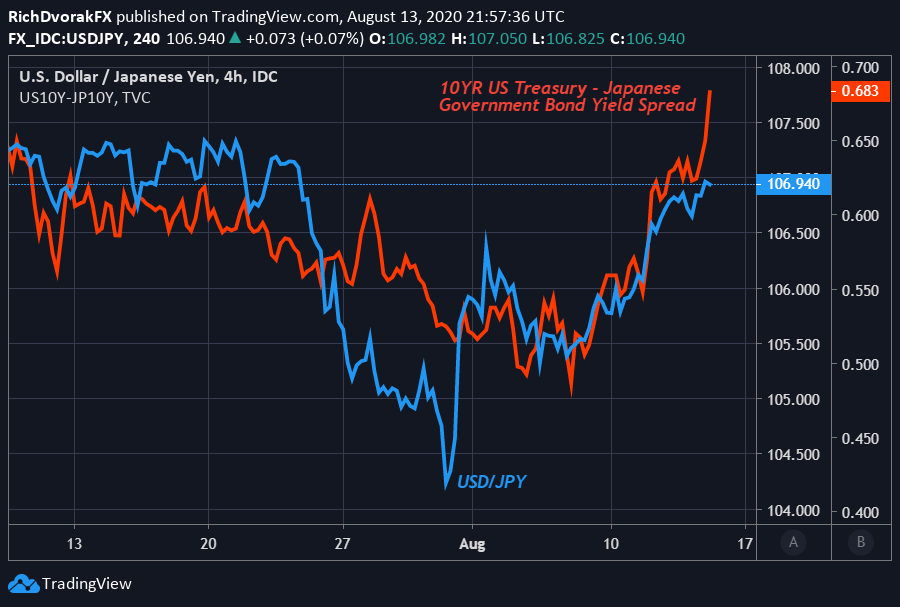

Japanese Yen (JPY)

Japan’s household spending showed signs of recovery close to the level it reached before the COVID-19 Outbreak. (1.2% against exp -7.8%, May -16.2%) This was within the first month after the end of the state of emergency declared all over the nation and as increasing numbers of businesses reopened and as the government makes more cash handouts. USDJPY, nonetheless, held near the mid-105s as the US released the more than expected job report and moved close to its 106-handled post-data while UST revenues continue to remain dampened.

The report of Japan finance minister Aso shows that Japan has no plan to cut sales tax. However, public finances become tougher than what it was during the global financial crisis. The government works to attain secure financial sustainability for upcoming generations. The move by Japan to stop reliance on China enhances SEAsians’ exports and according to Kyodo News Japan and Britain agree on the post-Brexit trade deal. The two countries home to achieve basic agreement towards the end of August 2020.

Canadian Dollar (CAD)

The loonie traded low lower during Friday’s Asian session after President Trump declared re-imposition of tariffs on Canadian aluminum exports to the United States towards the end of the previous session. Another factor that contributed to the rise in USDCAD to mid-1.33s before the US Open session is Risk aversion. Also, a more than expected US job market further gave USDCAD a boost to the upper-1.33s, the position is maintained during the weeks’ closing time.

ANTIPODEANS (AUD and NZD)

The duo gave up their recent gains against the US dollars during Friday’s session, in line with a wider risk aversion. The USD was in line with the RBA’s anticipated dovish monetary policy statements and assistant governor Ellis’s repetition of a similar report when she delivered a speech. The two economies plan to alter their policy package if it is called for. However, the rate of economic recovery is anticipated to be less than the previous projections.

Chinese Yuan (CNY)

The PBOC revolved the onshore yuan a score stronger against the US dollar during Friday’s Asia session. It refreshes the yuan’s topmost rise starting from the 10th of March, 2020. This tallied with expectations and added only CNY 10bln through 7-day OMO at 2.2% to provide “reasonably large” liquidity in the banking system. The move led to a net drain of CNY 10bln from the system with a growing 7-day reverse repo. This brings the tally to CNY 270bln during the trading week.

USDCNH, nonetheless, move higher to towards 6.9750 at the beginning of the Asian trading hours, after US President Trump signed an executive order to ban the TikTok and WeChat apps in the US. This was after the previous announcement to delist all US-listed Chinese companies that fail to meet the onshore accounting rules by the end of 2021.