{kind=link}

- US interest rate futures extended gains, pricing over an 80% chance of a 25-bps Fed cut at the October meeting.

- Fed Funds and SOFR contracts climbed as traders positioned for near-term easing while staying cautious on inflation.

- The US data blackout amid the government shutdown has heightened volatility across short-term rate futures.

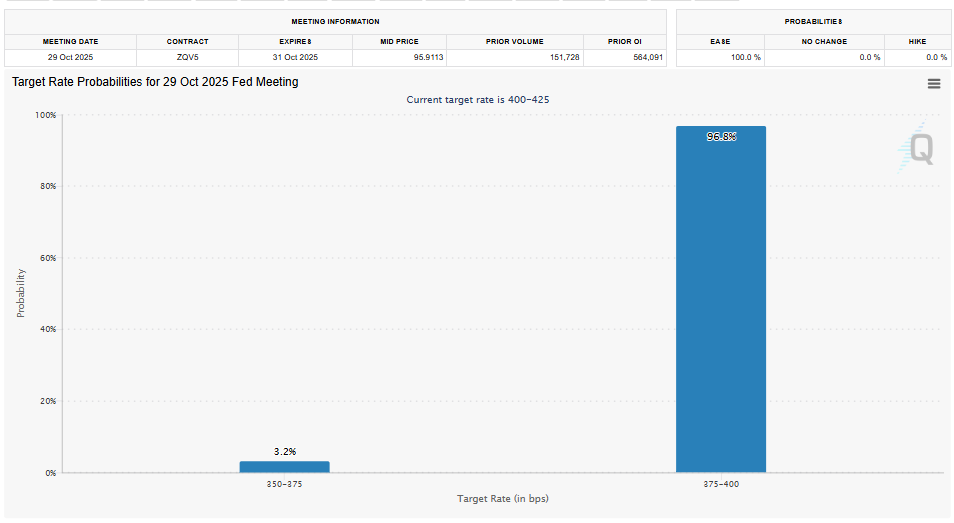

The US interest futures resumed their upward trend this week, with investors increasingly convinced that the Federal Reserve would at least cut rates once before the end of the year. The October meeting is now fully priced with a 25-bps shift.

The change reflects an increasing belief that the US policy rate will not go further despite a sticky inflation rate and limited data flow caused by the current government shutdown.

The expectation along the entire curve was altered as the September Fed rate cut to 4.00%-4.25% pushed short-term interest futures sharply. The CME FedWatch Tool suggests an 80% likelihood of another reduction this month, with futures indicating a new target zone is nearer to 3.75%-4.00% after October.

Fed officials have left mixed signals, as Governor Michelle Bowman indicated two more cuts are still probable later this year to maintain the recovery without triggering inflation. Her remarks were added to the dovish message of New York Fed President John Williams, who recently said that the central bank must be sensitive to indicators of a cooling labor market. Conversely, Vice Chair Michael Barr was wary and cautioned that the inflation is too strong to call a victory.

Such comments have directly translated to volatility in Fed Funds, Eurodollar, and SOFR futures. The fed funds contract, set to be settled in December 2025, increased by almost 10 bps last week, which indicates the re-pricing of the implied terminal rate.

SOFR contracts with longer dates, i.e., March and June 2026, have improved, suggesting that traders are stretching their expectations of relief further. The analysts at Barclays observed that the steepening of the curve in front-end futures indicates that the investors are subjectively anticipating policy easing in the near term.

The inflation ambiguity, which the government shutdown has stalled, has also increased speculative positioning. The open interest in 2-Year Treasury and Fed Funds futures increased to multi-month highs, with hedgers and macro funds repositioning and exposing themselves to the changing Fed rhetoric.

Consequently, US interest futures are reacting to a combination of dovish guidance and their partial observation. The policy meeting in October may prove that what the futures traders already baked into the market with the Beige Book, the Fed may start a measured, data-driven cycle of easing that could set the tone of the rest of 2025 through the October Beige Book, with its mixed regional conditions reports. Inflation still above target may confirm what is being priced in.