- US equities remain cautiously optimistic as the ceasefire between Iran and Israel announced.

- Falling crude oil prices ease the energy-driven inflation concerns.

- Investors are watching Fed Chair’s testimony to find clues about easing policy.

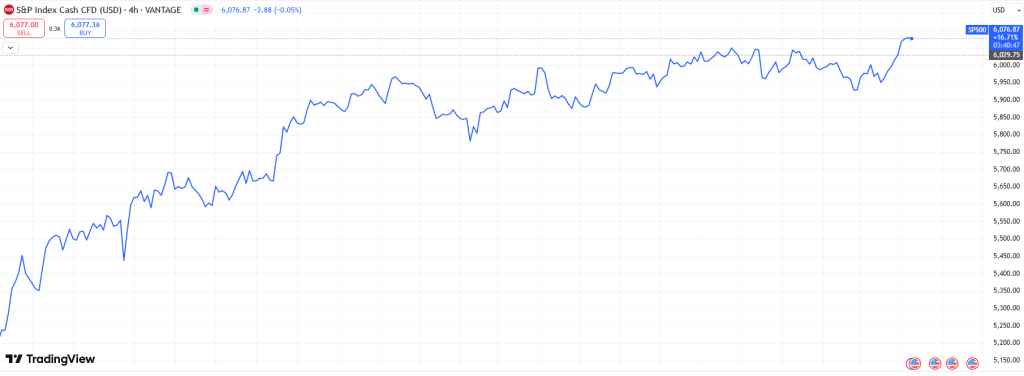

US equities started the week with a cautious tone as major indices showed mixed performance. The investors weighed the implications of a ceasefire between Iran and Israel along with expectations of Fed’s future rate policy. Although the Middle East de-escalation briefly boosted risk sentiment, underlying factors like inflation, interest rates, and earnings growth kept the rallies in check.

On Monday, the US President announced a complete ceasefire between Israel and Iran, following around two weeks of aerial strikes, including the US attack with B-2 stealth bomber on three nuclear sites of Iran. The news initially lifted equites as investors turned to the risk assets amid a sharp decline in crude oil prices. The WTI fell more than 3% on Tuesday, while it had already plunged 13% on Monday. The energy-driven inflation concerns have eased out that could potentially lower the cost pressure for US businesses.

The S&P 500 and Nasdaq Composite posted significant gains, supported by gains in the tech and consumer discretionary stocks. However, Dow Jones Industrial Average underperformed as energy shares showed weakness. However, the stock rally remains capped by the Fed’s monetary policy trajectory.

Fed Chair Jerome Powell’s testimony before Congress is due to day. Investors are cautious as they tend to seek clarity on whether the Fed will ease soon amid cooling inflation and mixed economic data or not. Recent comments from Fed officials have opened doors for a rate cut in July. However, Powell is so far cautious and unclear. The CME FedWatch tool shows a probability of 22% for the rate cut in July. It indicates that any dovish hint by Fed Chair may trigger a rally in equities.

On the data front, the economic indicators are mixed as jobless claims slightly rose while PMIs suggest sluggish activity in manufacturing sector. On the other hand, retail spending and consumer confidence remain steady that may support the earning outlook for key sectors.

The corporate earnings season is set to resume in July and investors are holding tight for stronger signals on Fed policy and inflation. Volatility stays lower but headline risk including geopolitics, central banks and tariff updates may drive the markets. Overall, the sentiment is cautiously optimistic as S&P 500 hovers near fresh record highs but lack a follow-through momentum.