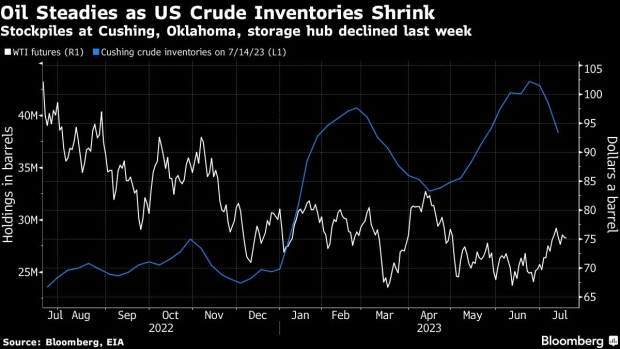

- US crude inventories fell by 708,000 barrels last week to 457.4 million barrels.

- The strength of the US dollar index exerted downward pressure on prices.

- Retail sales in the US rose less than expected in June.

On Wednesday, oil prices declined slightly as investors took profits, following earlier gains driven by tighter US crude supplies and China’s commitment to boosting economic growth. Oil had risen by more than $1 a barrel but lost later in the session.

Phil Flynn, an analyst at Price Futures Group, stated that market participants capitalized on the higher prices to take profits. Additionally, the strength of the US dollar index exerted downward pressure on prices, making crude more expensive for investors holding other currencies.

WTI vs crude inventories (Source: Bloomberg EIA)

According to Energy Information Administration data released on Wednesday, US crude inventories fell by 708,000 barrels in the last week to 457.4 million barrels, contrary to analysts’ expectations of a 2.4 million barrel drop.

Notably, inventories in the Strategic Petroleum Reserve increased for the first time since January 2021, as the US aimed to replenish the reserve following last year’s record drawdown. Furthermore, on Tuesday, China’s top economic planner pledged to implement policies to “restore and expand” consumption, potentially boosting oil demand.

Data from Tuesday indicating that retail sales in the US rose less than expected in June strengthened the view that the Federal Reserve might halt interest rate hikes. Higher interest rates could increase borrowing costs, potentially slowing economic growth and reducing oil demand.

In another positive development, a European Central Bank governing council member, Klaas Knot, suggested that rate hikes beyond the ECB’s upcoming meeting were “by no means a certainty.”

Klaas Knot, a governing council member of the European Central Bank (ECB), stated in an interview on Tuesday that the ECB will closely monitor signs of inflation cooling down in the upcoming months to avoid excessive rate hikes.

Regarding the possibility of further rate increases, Knot emphasized that it is necessary for July, but beyond that, it would at most be a possibility, not a certainty. He highlighted the importance of attentively observing the data, as the focus has been primarily on the risk of persistent inflation.

However, the balance of risks is gradually shifting, and there is a need to be more cautious about the potential of doing too much in terms of rate adjustments. An end to global hikes is positive for oil.