{kind=link}

- US interest futures remain perplexed amid the Fed’s divergence on the timing and depth of policy easing.

- Recent macroeconomic data have challenged the earlier aggressive-easing narrative, with the Fed reiterating its data-dependent approach.

- The 2-Year Note reflects a strong correlation with policy expectations.

US interest futures are currently at the center of the macro debate as markets and the Fed diverge on the timing and speed of policy easing. Pricing in 3-month SOFR futures on CME indicates that traders still expect a lower policy rate path over 2026 than today.

However, the depth and pace of cuts implied by the curve have been repeatedly repriced as incoming data challenge earlier aggressive‑cuts narratives. The front part of the SOFR strip has flattened in recent weeks amid stronger-than-expected activity and sticky service inflation, leading markets to trim near-term easing expectations.

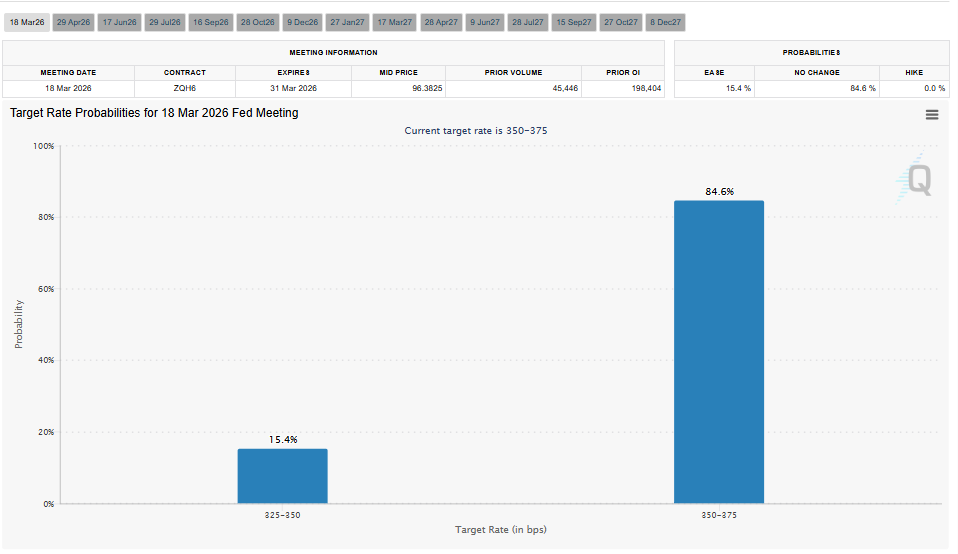

A key reference point is the CME FedWatch Tool, which translates 30-day Fed Funds futures pricing into probabilities of rate moves at each FOMC meeting. The futures market still expects a good chance of cuts in the next year, but the distribution has moved toward a more gradual path as the Fed has stressed its commitment to being “data dependent” and avoiding a premature pivot.

This tension between the Fed’s data-driven caution and lingering market optimism about cuts is evident in the way probabilities swing sharply after each major inflation or labor-market release.

Further out on the curve, US Treasury futures, notably the 2-Year (ZT), 5-Year (ZF), and 10-Year (ZN) contracts, are reflecting a more subtle story about growth and term premia. The 2-Year Note futures remain closely tied to policy expectations, rallying on signs of disinflation or soft data and selling off when markets contemplate a “higher for longer” stance.

At the same time, the 5-Year and 10-Year futures have been going up and down as investors weigh strong economic activity against worries that strict policy could slow growth more sharply in 2026. The term structure of SOFR and Treasury forwards suggests there is only a small term premium at present.

Positioning and volatility are still very important in the most recent price action. Speculative accounts and macro funds have been active in SOFR futures spreads, trading the curve’s shape (for example, buying deferred contracts while selling near-dated ones) to express views on whether the Fed will ultimately have to cut more than its own dot plot suggests.

Tools like the Atlanta Fed’s Market Probability Tracker show that options on rate futures price in tail risks of both much higher and much lower policy rates. This shows a fragile consensus path.