- Investors eagerly await the US inflation data and the FOMC meeting.

- Some investors believe Wall Street is currently experiencing a bull market.

- The ECB is expected to raise interest rates by a quarter percentage point on Thursday.

US equities rose on Monday, with the S&P 500 and the Nasdaq reaching their highest closing levels since April 2022. Investors eagerly awaited the week’s inflation data and the Federal Reserve’s interest rate decision.

Amazon, Apple, and Tesla contributed to the S&P 500’s recovery of 21% from its October 2022 lows. Some investors believe Wall Street is currently experiencing a bull market. Markets expect the US Labor Department’s consumer price index report on Tuesday to reveal a slight cooling of inflation in May, with core prices expected to remain stable.

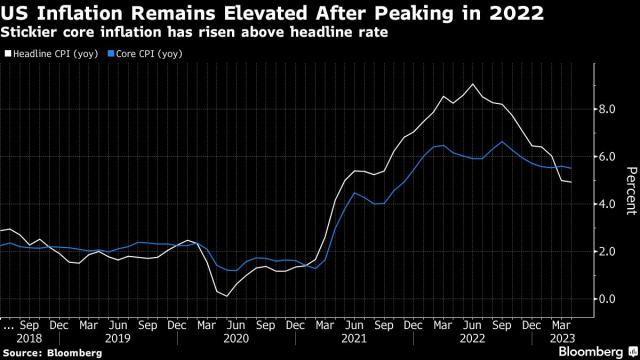

US inflation (Source: Bloomberg)

Additionally, Tuesday marked the beginning of the Fed’s two-day meeting. According to the CME Fedwatch tool, traders predict a 76% probability that the central bank will maintain rates within the 5%-5.25% range on Wednesday, while there is a 71% chance of a rate hike in July as inflation remains elevated.

Dylan Kremer, a co-chief investment officer of Certuity, commented that the Fed might remain dependent on data and keep rates steady in the near term, although future rate hikes are not ruled out.

Recent gains in mega-cap stocks, better-than-expected quarterly earnings, and the possibility of the Fed nearing the end of its monetary tightening cycle have boosted equities in recent weeks. The rally has also expanded to include economically sensitive areas like energy, industrials, and small-cap stocks.

Despite higher interest rates, data continues to demonstrate the resilience of the US economy. On Friday, Goldman Sachs increased its year-end price target for the S&P 500 to 4,500 from 4,000, citing the broader market rally.

In European markets, Germany’s DAX index led the gains on Monday, driven by an upgrade in Adidas shares. Investors were primarily focused on significant central bank policy meetings scheduled throughout the week. The Fed is anticipated to maintain steady rates after its policy meeting concludes on Wednesday.

Meanwhile, the ECB is expected to raise interest rates by 25bps on Thursday to control persistent inflation. At the beginning of the year, the STOXX 600 index had a stronger performance than the S&P 500 index. However, during the second quarter, it lost momentum as investors increasingly favored growth-oriented stocks over value stocks.