- Investors expect quarterly results from prominent banks this week.

- Analysts estimate third-quarter earnings for S&P 500 companies increased 2.2% year-over-year.

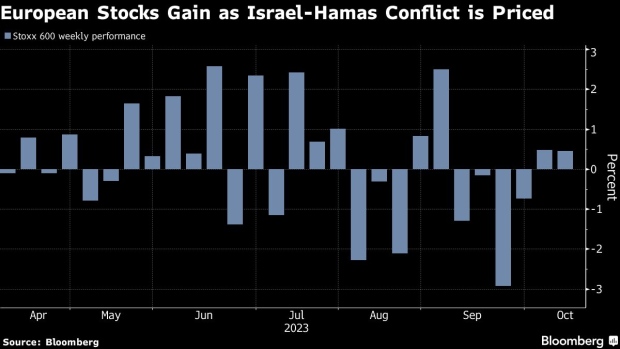

- European equities started the week positively, driven by gains in financial and mining stocks.

On Monday, US equities surged, driven by investor optimism for the start of earnings season. Moreover, transportation and small-cap shares gained, further boosting optimism. Still, investors remained cautious as Israeli forces continued to bombard Gaza, with cease-fire efforts failing and thousands, including many women and children, losing their lives. Global leaders are working to contain the Middle East conflict.

This week, investors expect quarterly results from prominent banks like Goldman Sachs, Bank of America, Morgan Stanley, pharmaceutical giant Johnson & Johnson, electric vehicle manufacturer Tesla, and video-streaming pioneer Netflix.

Analysts estimate third-quarter earnings for S&P 500 companies increased 2.2% year-over-year, up from the previous week’s estimate of 1.3%, per LSEG data.

There was also optimism after Philadelphia Fed President Patrick Harker reaffirmed that the US central bank had likely concluded its rate-hike cycle.

Elsewhere, the New York Fed’s General Business Conditions index, known as “the Empire State Index,” returned to negative territory.

Stoxx 600 weekly performance (Source: Bloomberg)

European equities started the week positively, driven by gains in financial and mining stocks. The gains came despite caution about the Middle East situation, indicating investors had mostly priced in the conflict.

Concerns about the Eurozone labor market and the Middle East conflict have kept investors on edge. Speaking at a conference, Lagarde emphasized that the labor market remains robust, with no apparent signs of deterioration. She noted that the data related to workforce participation, actual unemployment rates, and nominal unemployment numbers are notably strong.

On the other hand, the UK’s FTSE 100 saw an increase, supported by rising commodity-linked stocks.

Investors will closely watch the September data on the UK’s unemployment rate this week. Moreover, inflation will likely rise to 0.4% in September from 0.3% in August but fall to 6.5% from 6.7% annually, according to economists.

Stuart Cole, the chief macroeconomist at Equiti Capital, anticipates that the key labor and CPI figures set for release on Tuesday and Wednesday could signal the necessity of maintaining tight monetary policy. This assessment holds despite the lackluster growth figures observed last week.

Chief Economist Huw Pill stressed that the Bank of England (BoE) should not conclude that the battle against high inflation has ended merely because the price growth rate has decelerated.