- Stronger-than-expected services sector data might lead to prolonged high interest rates.

- China prohibited central government agencies from using iPhones.

- German industrial orders experienced a larger-than-anticipated drop in July.

On Wednesday, US equities closed down, with the Nasdaq leading the decline with a 1% loss. This drop was driven by concerns that persistent inflation, fueled by stronger-than-expected services sector data, might lead to prolonged high interest rates.

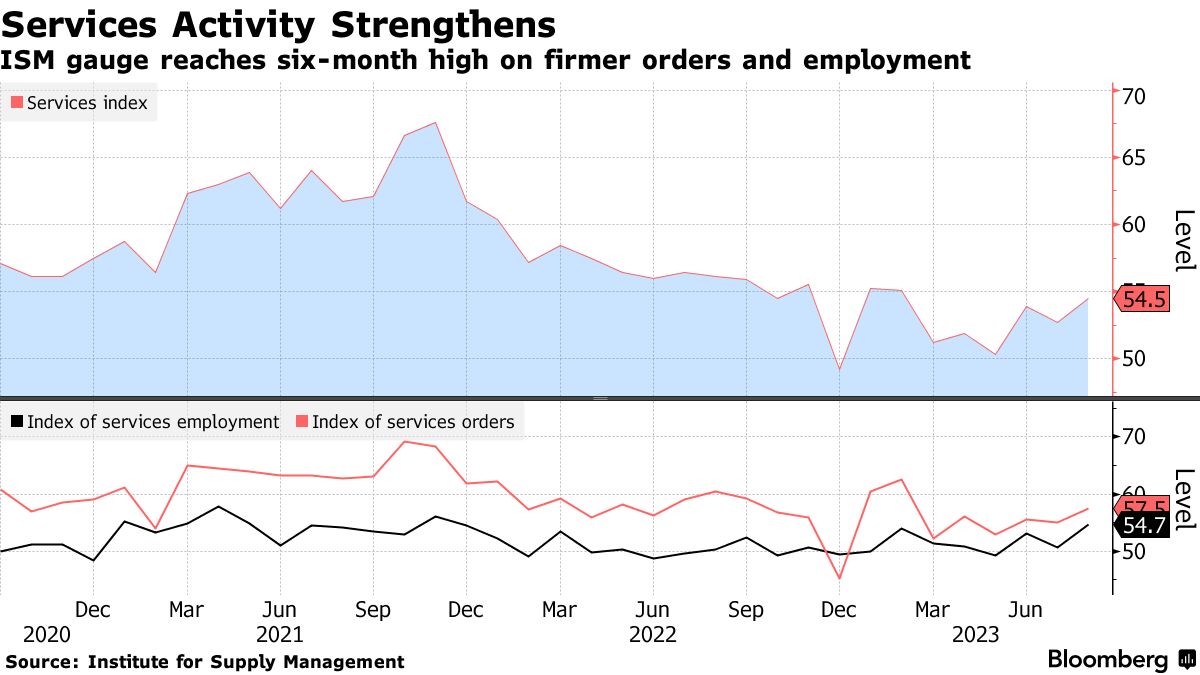

US services activity (Source: Institute for Supply Management)

The Institute for Supply Management disclosed that its non-manufacturing Purchasing Managers’ Index for the previous month was 54.5, surpassing expectations of 52.5. Additionally, the gauge measuring prices paid by service-sector businesses for inputs rose.

Traders believed there was a 93% chance that the US Central Bank would maintain current interest rates at its September 20 meeting, with a 57% likelihood of another pause in November, as indicated by CME Group’s FedWatch Tool.

Carol Schleif from BMO’s family office in Minneapolis commented on the situation, saying, “The unexpectedly strong ISM services data suggests that investors will struggle to interpret the post-pandemic economic signals.” Despite hopes for interest rate cuts, Schleif noted that the data indicated a robust economy, and inflation wasn’t decreasing quickly enough for the Fed to consider rate cuts in the foreseeable future.

Earlier in the day, Boston Fed President Susan Collins emphasized the need for caution in the central bank’s future monetary policy decisions.

The anticipation of higher interest rates particularly impacted growth stocks, with the S&P 500 growth index underperforming the overall market during the session. Equity investors also responded to rising yields in 10-year and 2-year US Treasuries.

In addition to rate concerns, Apple Inc. experienced a 3.6% decline due to reports that China had prohibited central government agencies from using iPhones and other foreign-branded devices for work.

The S&P 500 appeared largely unaffected by the Federal Reserve’s “Beige Book” report on the US economy, which was released a week ahead of the highly anticipated August inflation data and the Fed’s rate decision on September 20.

The “Beige Book” report indicated “modest” economic growth in recent weeks, subdued job growth, and a slowdown in inflation in most parts of the country.

Meanwhile, European stocks continued their decline for a sixth straight session due to concerns about slowing global economic growth. Additionally, the increasing bond yields exerted pressure on equity markets.

Further confirming the trend of sluggish economic growth, data revealed that German industrial orders experienced a larger-than-anticipated drop in July.