- Bank stocks significantly underperformed following the failure of First Republic Bank.

- Investors are worried the US government will run out of money soon.

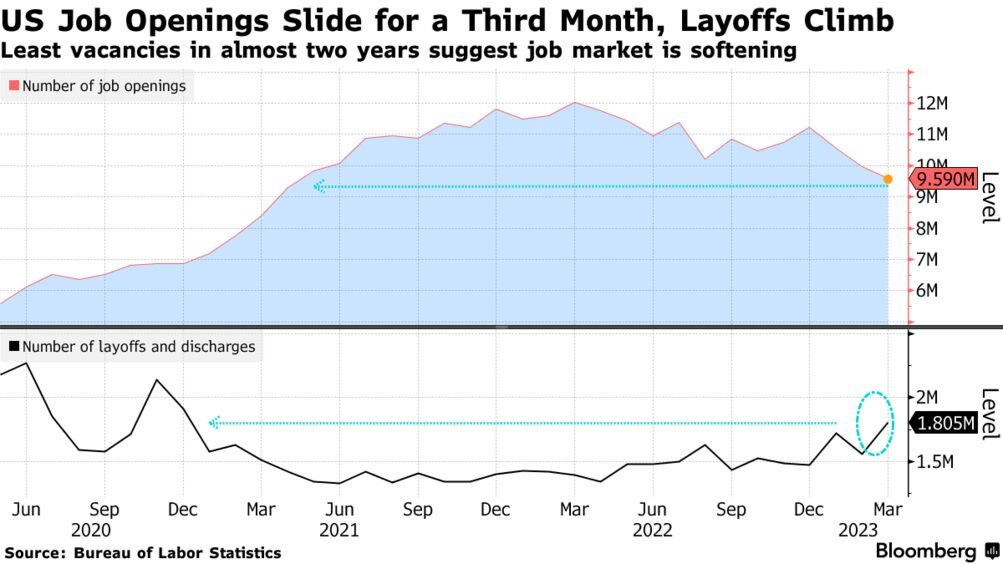

- Job vacancies in the US decreased for a third consecutive month.

US equities ended lower Tuesday due to concerns that the government would run out of money after June 1 without a debt ceiling increase. Bank stocks collapsed following the weekend failure of American regional bank First Republic Bank.

Energy shares tumbled as oil prices fell by 5% to a five-week low amid Concerns about the economy.

On Tuesday, senior US Senate Republicans urged President Joe Biden to accept their party’s debt-ceiling proposal or make a counteroffer.

A prominent Democrat said the Senate might try to pass a “clean” debt-ceiling hike next week. The Treasury Department has warned that the US could run out of funds to pay its debts in the upcoming month.

The S&P 500 bank index fell 3.2% due to the large declines in smaller US banks. Th declines came after the First Republic folded over the weekend and sold its assets to JPMorgan Chase.

Tuesday’s trading highlighted growing market concerns that other banks might begin to see rapid deposit outflows similar to First Republic Bank’s.

Job vacancies in the United States decreased for a third consecutive month. At the same time, layoffs rose to their highest level in more than two years, indicating a possible softening in the labor market. This softening might help the Fed in its fight against inflation.

European shares fell to their lowest point in almost a month on Tuesday, dragged down by the energy sector.

Oil and gas shares fell 4.5%, marking their lowest finish in over a month. The drop followed the decline in oil prices due to market concerns. There were concerns about a potential US bond default, bad Chinese economic data, and global rate hikes.

Investors are expecting a 25bps rate boost on Wednesday. The markets will also be paying careful attention to the European Central Bank (ECB), whose rate decision is anticipated on Thursday.

According to derivatives markets, European rates are expected to peak at about 3.7% in November.

On the data front, banks in the Eurozone are turning off the lending taps, and an important inflation indicator is finally declining. These reports support the case for a more gradual increase in rates.