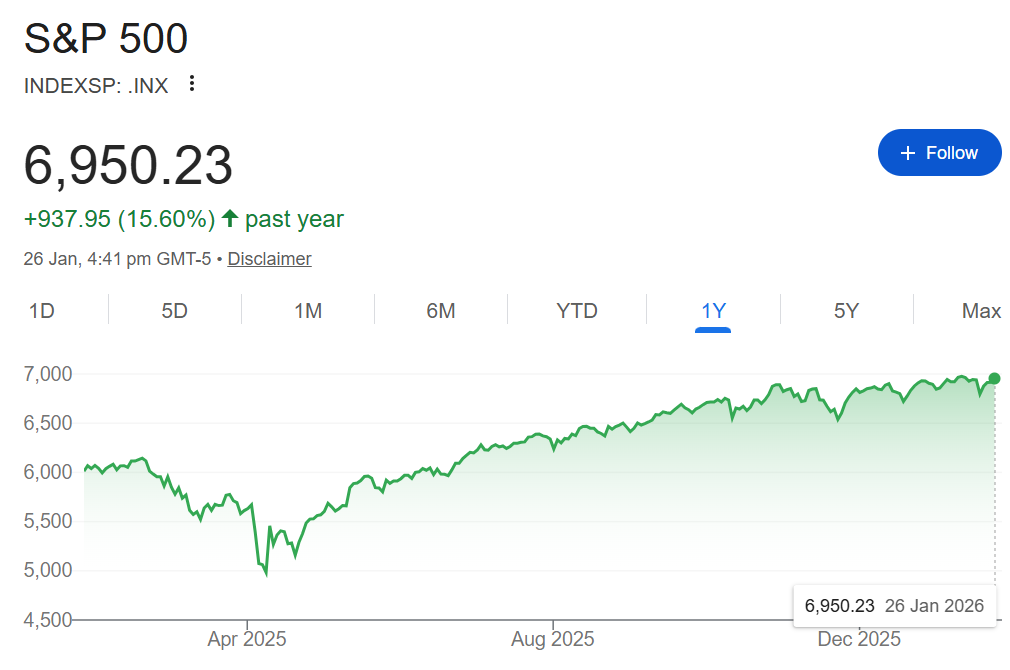

- US equities remain mildly supported amid economic and political noise, with tech stocks leading the way.

- Tariff concerns continue to cap the equities rally, while Big Tech earnings reports help maintain cautious risk-on sentiment.

- The upcoming Fed meeting, followed by Powell’s press conference, remains a key event for the week.

US equities are slowly rising despite a lot of noise in the economy and politics. Tech stocks are helping to keep risk sentiment high, even as policy and tariff risks grow. On Monday, the Dow, S&P 500, and Nasdaq rose by about 0.4% to 0.6%. This kept the cautiously optimistic mood going into a week full of Big Tech earnings reports and a major Federal Reserve decision. Breadth and volume indicate steady, not euphoric, participation, and volatility remains low despite plenty of headline risks.

Tariffs and policy concerns remain significant problems. President Trump has threatened to raise tariffs on several South Korean goods and even suggested a 100% tariff on Canadian imports if Ottawa makes a deal with China. This shows that he is willing to use trade tools aggressively.

At the same time, the administration is pressuring US health insurers with a proposal to sharply slow the pace of Medicare payment increases, triggering double-digit drops in UnitedHealth and Humana and notable weakness across the managed-care space. These moves highlight that policy risk is now very stock‑ and sector-specific. Trade-exposed cyclicals and healthcare insurers face headline shock risk, even as the broader indices hold up.

The Fed is the second most crucial part of this week’s story. Most market participants anticipate the central bank will keep rates unchanged. Still, markets are paying closer attention to Chair Powell’s press conference and any response to attacks on the Fed’s independence. Trump has hinted that he might name a successor to Powell as soon as this week. This raises questions about the future policy path and adds a political complexity to the usual “rates and data” story. With the Dollar Index (DXY) sliding and 10-year Treasury yields easing slightly, the markets are effectively pricing a “steady for now, cuts later” path, which is supportive for duration-sensitive growth names.

Earnings and sector moves round out the picture. Big Tech and AI-linked semis are driving the market’s resilience. Apple, Meta, and Microsoft have been key index drivers on their results. At the same time, Nvidia’s $2 billion investment in CoreWeave underscores confidence in the AI infrastructure build-out, even as Intel sells off on weak guidance. Bank of America’s belief that the biggest AI chipmakers still have good PEGs supports the idea that the “AI trade” is based on real growth rather than just speculation. On the other hand, health insurers and airlines that fly in bad weather have been slow to react to unusual shocks, which shows that the index level is becoming more spread out.

Safe-haven flows into gold and silver are at record highs, while the US dollar is weaker and yields are slightly lower. This shows that investors are hedging against macro and political risks while maintaining their core equity exposure.

Overall, US stocks are in a “cautious risk-on” phase. Tech, AI, and strong macro data support the indices. Still, threats of tariffs, healthcare regulation, storm-related disruptions to growth, and uncertainty about who will lead the Fed suggest trading will be choppy, and single-stock risk will be high, rather than a straight-line rally.

{kind=link}