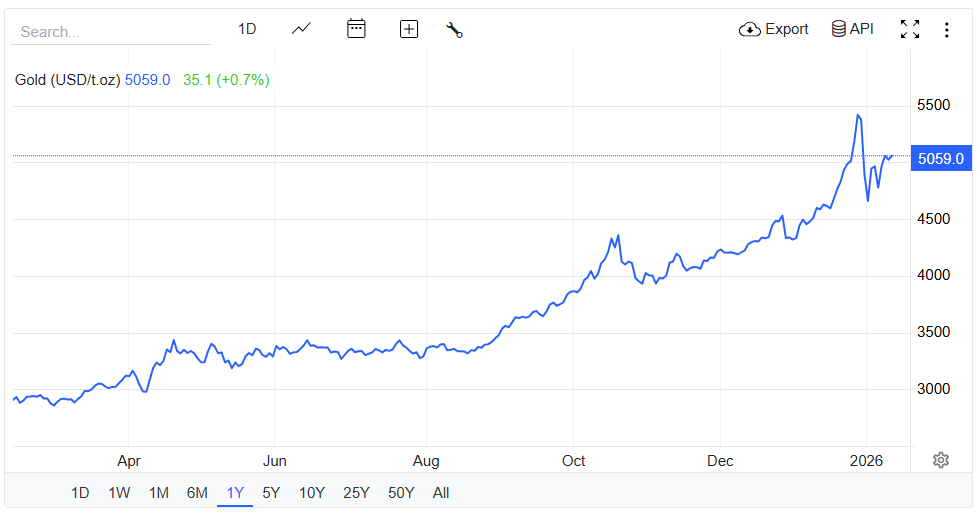

- Gold futures remain tilted to the upside amid central bank buying and macroeconomic uncertainty.

- The Fed’s dovishness and geopolitical risks make gold a safe-haven asset for emerging markets to diversify away from the US dollar.

- Markets await the US NFP data ahead, which is expected to continue revealing weakness.

Gold futures continue to receive strong fundamental support from central bank demand, ongoing macroeconomic uncertainty, and limited supply. This gives the metal a positive medium-term outlook.

After a quick round of profit-taking earlier this year, most investors have seen the price fall, not as signs that the bull market is over, but as opportunities to buy back into the market.

Central banks’ ongoing asset purchases are a big part of this resilience. Many countries that import commodities and are in emerging markets are steadily moving away from the US dollar by building up their gold reserves. This official-sector demand, at historically high levels, helps keep prices from falling, even as speculative flows from futures and exchange-traded funds (ETFs) become more cautious.

Current macroeconomic conditions still make gold a good strategic hedge. Headline inflation has fallen from its peak. Yet, real yields and currency expectations keep shifting. This is due to underlying price pressures and uncertainty about the Federal Reserve’s (Fed) interest rate plans. Many institutional and retail investors still see gold as portfolio protection. They want a safeguard in case inflation is worse than expected or if renewed financial stress forces central banks to ease more aggressively.

Geopolitics gives it even further support. Some countries and major investors are holding more assets outside the US-centred financial system due to ongoing conflicts, shifting global alliances, and concerns about sanctions. These trends are good for gold, a physical asset that everyone agrees is a sound reserve.

On the supply side, mining problems are slowly making the market less balanced. There haven’t been many new large-scale discoveries, timelines are still long, and environmental and regulatory pressures are growing. Moving ahead, market participants are eagerly awaiting the US NFP report, which could spur volatility in gold prices.

The January Non-Farm Payrolls report, to be released today (February 11, 2026), is expected to show that nonfarm jobs grew by about 70k. The unemployment rate is likely to stay steady at 4.4%. The slower-than-usual payroll growth shows that the labor market has been cooling and weakening since late 2025. This means hiring is slowing as the economy as a whole becomes more uncertain.

The report is more important than usual because it not only includes immediate employment data but is also expected to show significant changes to benchmark data from previous months. These changes could alter market expectations about the Federal Reserve’s interest rate path and when policy changes might occur in the next few quarters.

Some analysts, like MUFG Research, predict even weaker growth of 30k jobs, suggesting the labor market is getting even softer. Both fixed-income and equity traders will be keeping a close eye on the employment data. If it misses the mark by a lot, it could make the case for Fed rate cuts in the spring stronger. On the other hand, if it beats the mark, it could prompt investors to reconsider how quickly inflation will slow and how long higher rates will last.

{kind=link}