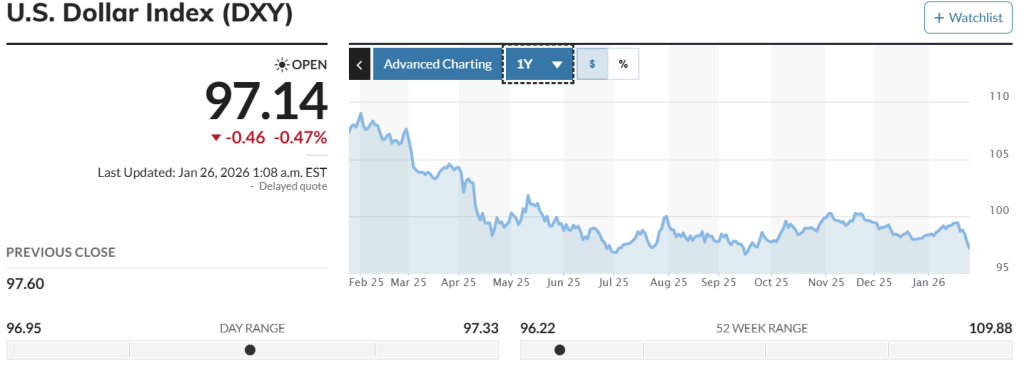

Currency futures are opening the week with the USD complex still fragile, even though pockets of safe-haven demand show up on tariff/geopolitical headlines. The US Dollar Index futures (DXY) are around 97.0–97.1, close to their lowest level in months. Investors are weighing the noise around trade policy, the “Sell America” flows, and the risk that allies will cut back on their USD exposure. The US Durable Goods Orders remain a key short-term event, but the real pricing event of the week is the FOMC decision (Wednesday). The rates are expected to stay unchanged between 3.50% and 3.75%. The market will trade on Powell’s guidance on the next cut.

The Euro FX futures (6E) are more than just “USD weakness”. The 6E trades near 1.1900, partly reflecting the weaker dollar going into the Fed, but also a bet that Europe’s data in the near future won’t cause a sharp drop in the euro’s value. The preliminary Q4 Eurozone GDP and the German January HICP are this week’s Eurozone catalysts. They can change how soon and how far the ECB can ease. If inflation or growth picks up, it would help 6E by raising expectations for European rates. If prints are weaker, it would limit EUR rallies, especially if the Fed sounds even a little hawkish.

UK data surprises, going against the easing narrative, are helping British pound futures (6B). GBP futures are close to 1.3660, the highest level since September 17, 2025. This occurs as the UK Retail Sales beat expectations with a 0.4% MoM increase in December (compared to a 0.1% decrease expected), and core retail sales rose 0.3% MoM. The UK Composite PMI also came in at 53.9, which is the highest level in 21 months. The combination makes traders think that the BoE can hold off in February and that more cuts may come later, even though the markets are still pricing in a quarter-point cut by June.

The Australian dollar futures (6A) are sending out mixed signals. The PMIs for Australia were strong (manufacturing 52.4, services 56.0, and composite 55.5), and employment was better than expected (+65.2K, unemployment 4.1%). This supports the RBA’s “tighter for longer” bias, even though CPI is still above target (3.4% YoY in November). But USD safe-haven spikes and the global risk tone are also pulling AUD’s path.

Intervention risk, the Bank of Japan and the Federal Reserve rate differentials are driving Japanese yen futures (6J). The yen went up because of talk about rate checks from the MoF and the NY Fed, as well as official warnings. The BoJ held rates at 0.75% (8–1), raised its forecasts, and kept a hawkish lean. That mix pushed the yen futures to 2-month highs.

{kind=link}