Capitalism is not going anywhere, but the coronavirus crisis has certainly jolted the foundation of the global economy. Perhaps, the deep recession was inevitable. What is startling, however, is that the GDP would contract by 3.1% in 2020. Comparatively, it makes the current year weaker than the financial crisis of 2007-08.

That said, it seems as if the worst is past and the economic recovery is on the horizon. So long as the medical professionals manage to flatten the infectious rates, there are good chances economies will start to reopen sooner than people realize. However, there will have to be new control measures in place to halt the spread of the virus.

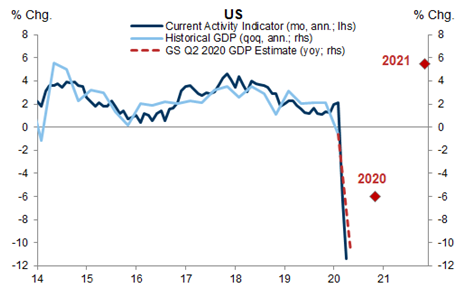

The U.S. GDP Growth

You can for instance expect a -34% QoQ annualized GDP growth in the second quarter prior to the slow recovery. Simultaneously, the Q2 will also witness the dwindling output by the end of the year. Consequently, it would leave the cumulative growth of 2020 at -6%. As of now, the unemployment rate is at 14%, and the Q3 will see a one-percent increase. In addition, the PCE index will unfortunately see inflation of about 1¼ percent at the end of 2020.

Apart from uncapped assets and return of the zero rates, the Fed has put in place numerous crisis facilities to provide corporates with sufficient funding, minimal reserve requirements, relax capital buffers, and initiate FX swaps with international central banks. Concurrently, these steps are good enough to render support and maintain the credit flow. However, the Fed will have to intervene for more assistance in the foreseeable future.

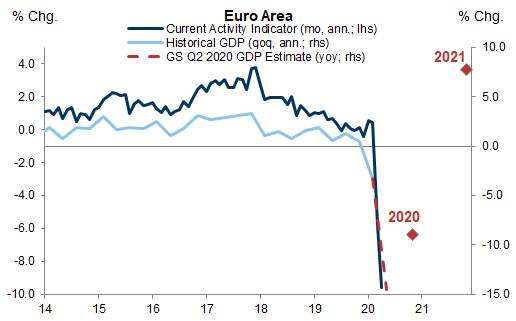

GDP Growth: European Region

Conversely, the Euro region expects to see a YoY decline of -8.9% in GDP due to coronavirus outbreak. Massive 1H economic contraction is responsible for this decline. Not to sound pessimistic, but most of the European countries will see more economic contractions and a surge in unemployment rates. In fact, the process of economic normalization will be slower in Spain and Italy as compared to northern Europe.

The asset purchase program from the ECB and packaged measures from Eurogroup will certainly offer short-term economic relief. It will, however, fall short because it is not a permanent fiscal solution when it comes to sovereign risk. Therefore, you can expect more pressure to raise the PEPP and push ECP by the sovereign markets. The underlying objective is to garner EUR 500bn by the end of June. However, the recent contradictory German court ruling has put a question mark on the base.

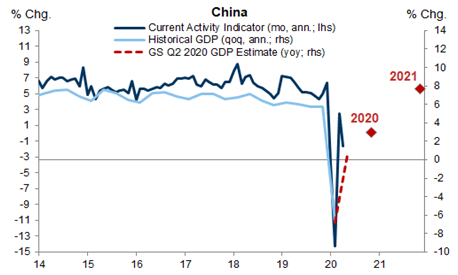

GDP Growth: China

After a YoY decline of 6.8% in China’s GDP growth in the first quarter, you can expect an economic rebound throughout 2020. However, strong stimulus packages and ease of virus restrictions will play a significant role. Collectively, the real GDP growth will round up at 3% at the end of 2020 with the assumption that the measures to control the virus will normalize economies in the third quarter (Q3). Furthermore, fiscal accommodative fiscal and monetary policies will lead to more positive growth in China.

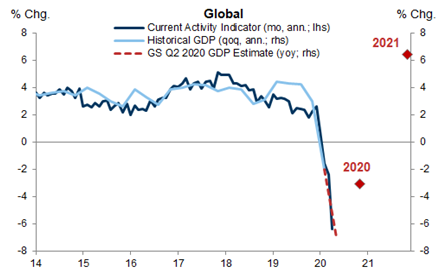

Global Economy and Coronavirus

As much as the economic balance hangs in the balance due to the coronavirus, the lockdown measures will flatten the infection rate and gradually ease the restriction in the upcoming months. As the economies start to reopen, the resurgence of new infections and the fallout from attempting to hit the pause button in nearly every country does however pose a great risk to the world economy and the recovery.