- US equities have been facing a rough patch, moving wildly in both directions as geopolitical risks grow.

- Rising crude oil prices have pushed the energy sector stocks to fresh highs.

- A risk-off sentiment and continued energy disruption could trigger inflationary shocks, weighing on the equities.

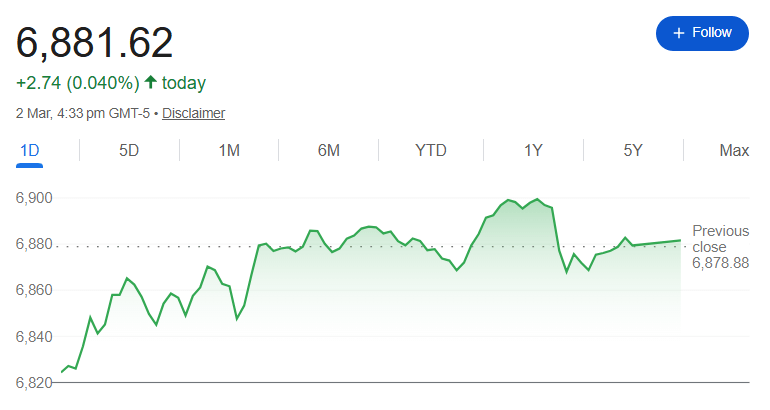

US equities had a rough start to March, swinging back and forth due to rising geopolitical tensions, even though domestic economic data showed economic resilience.

Futures fell sharply at first after the US and Israel bombed Iran over the weekend. This caused oil prices to rise sharply, raising fears of a larger regional war. The S&P 500 fell for a short time at the start of the day, but it bounced back and ended the day almost the same. The Nasdaq Composite went up slightly, and the Dow Jones Industrial Average lost some of its early gains but still closed slightly lower.

Crude oil became the main way that money moved into financial markets. After rising to almost $75 earlier in the day, US crude ended the day up about 6% at around $71 per barrel. This was the most significant daily jump since mid-2025. Worries grew about problems at the Strait of Hormuz, which is where about 20% of the world’s oil supply goes. The S&P 500’s energy sector hit new highs as energy stocks rose.

Even though the geopolitical shock was bad, economic data helped. The Institute for Supply Management said that its manufacturing PMI hit 52.4 in February. This marks the second consecutive month of growth, marking the strongest two-month stretch since 2022. Any figure surpassing 50 indicates growth, bolstering the belief that the US economy will experience a gradual recovery.

However, investors’ positions are still weak. Goldman Sachs’ trading desk said that the mood is unstable and the flows are inconsistent, which makes the S&P 500 weak as it didn’t clearly break through the 7,000 mark. Corporate buybacks have helped, and they’re going much faster than they did last year. However, a blackout window that starts in mid-March could take that support away.

Still, a few good things are happening. Corporate profits and profit margins recently reached all-time highs. However, bearish investor sentiment presents a contrarian positive, with only about a third of respondents in the latest AAII survey identifying as bullish. In the past, March has also had better second halves, especially after weak Februarys.

For now, US equities seem to be stuck between strong fundamentals and volatility driven by headlines. A lot will depend on whether the energy disruptions are short-lived or turn into a long-term inflationary shock that makes it harder for the Federal Reserve to make decisions and limits investors’ willingness to take risks.

{kind=link}