- US equities closed mixed on Tuesday after the US reported a big drop in job vacancies.

- Th US services sector recorded an increase in business activity in November.

- UK companies reported an increase in prices charged in November.

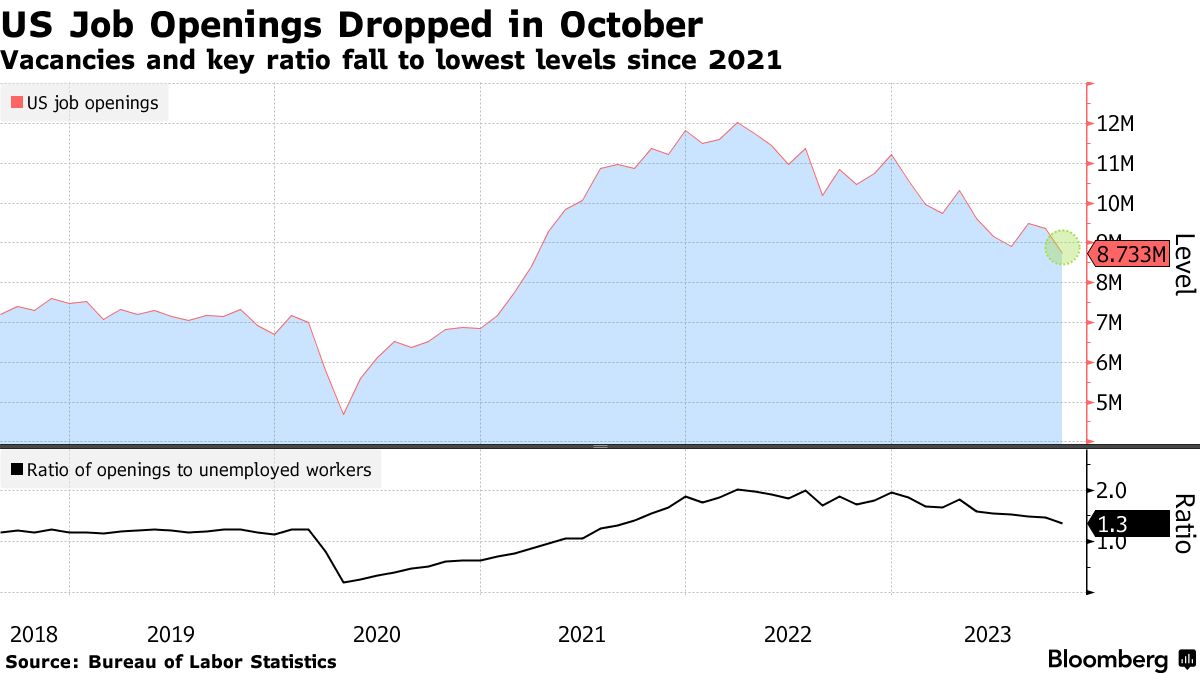

Equities closed mixed on Tuesday after the US reported a big drop in job vacancies. As a result, investors increased their bets on a Fed rate cut in March. Job vacancies in the US have fallen to their lowest level since early 2021.

US job openings (Source: Bureau of Labor Statistics)

On Tuesday, the Labor Department’s JOLTS report showed a drop to 1.34 job vacancies per unemployed person in October, the lowest since August 2021. This decrease suggests a potential relief in wage inflation as fewer workers resign.

Moreover, the larger-than-expected drop in unfilled jobs followed last week’s data, indicating a decrease in October inflation and prompting financial markets to anticipate an early rate cut. Sam Stovall, Chief Investment Strategist at CFRA Research, predicts the Fed is likely done raising rates, and the key question is when they will start cutting. Another report indicated increased US services sector activity in November. However, this week’s stock trading remained uneven after the S&P 500’s 9% November rebound.

Market expectations lean towards the Fed maintaining current rates next week, with interest rate futures suggesting a 65% chance of a cut by March.

Elsewhere, in a panel discussion, strategists at the BlackRock Investment Institute forecast increased market volatility, predicting fewer Fed rate cuts than what futures markets imply.

On Tuesday, German equities reached a record high, supported by gains in industrial stocks and insurers. Eurozone surveys showed a services sector downturn in Germany but at a slower rate than the previous month.

European Central Bank conservative Isabel Schnabel deemed further interest hikes “rather unlikely” following an unexpected fall in inflation. The ECB’s October consumer expectations survey revealed stable inflation expectations among Eurozone consumers, while the economic growth outlook worsened. Eurozone producer prices rose as anticipated in October compared to September, with a milder decline from the previous year.

Meanwhile, Britain’s FTSE 100 experienced a second consecutive session decline, with miners facing pressure due to a drop in gold prices and Moody’s revision of its outlook on China. Despite a survey indicating growth in the UK’s services sector in November, companies reported an increase in prices charged. This development poses a potential concern for the Bank of England ahead of its decision next week.