- Equities rose after a weaker-than-expected US payrolls report.

- Market expectations for the Fed to maintain interest rates at the December meeting now stand at 90.4%.

- There was an acceleration in the downturn of business activity in the Eurozone last month.

On Monday, US equities inched higher as investors looked for guidance from various Federal Reserve policymakers later in the week regarding the central bank’s policy direction.

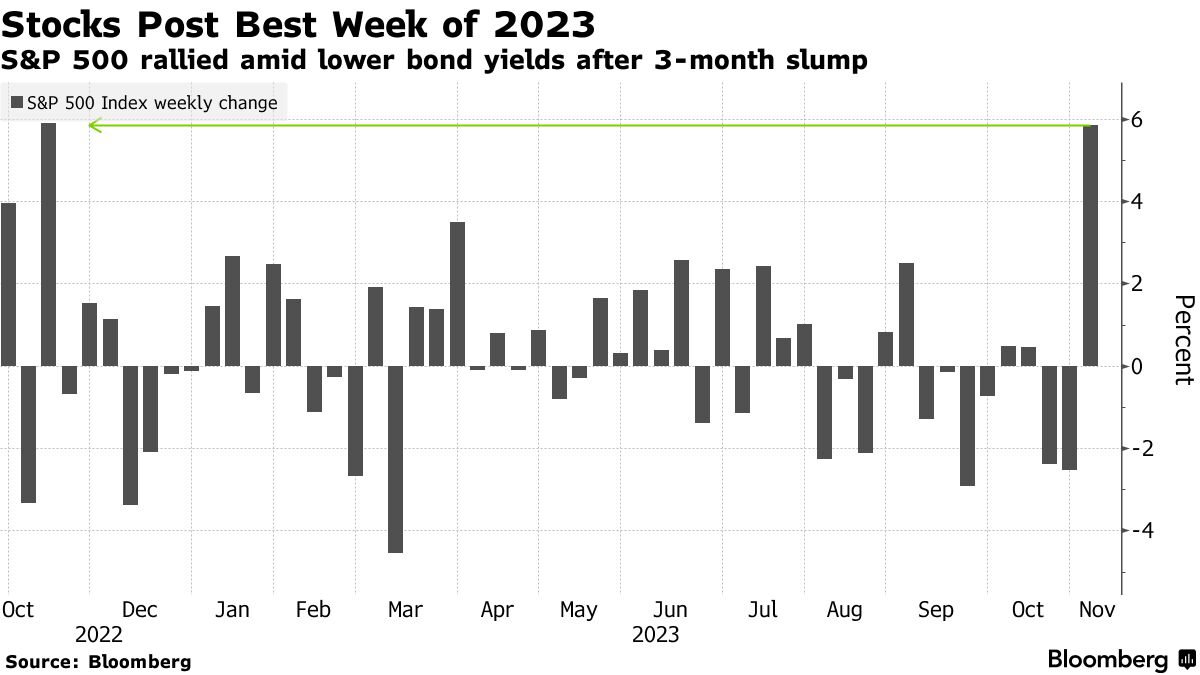

S&P 500 weekly change (Source: Bloomberg)

Last week, equities recorded their most significant weekly percentage gain in nearly a year due to a weaker-than-expected US payrolls report, which led to lower Treasury yields. This report suggested that the Fed might cease raising interest rates and potentially start reducing them next year.

Market expectations for the Fed to maintain interest rates at the December meeting now stand at 90.4%, down from 95.2% on Friday but higher than the 74.4% from a week ago. Meanwhile, anticipations of a rate cut of at least 25 basis points in May 2024 have exceeded 50%, according to CME’s FedWatch Tool.

Later this week, the markets will seek more clarity on the Fed’s intentions from officials scheduled to speak later. Speeches will come from Fed Chair Jerome Powell, New York Fed Chief John Williams, and Dallas Fed President Lorie Logan.

Stephen Massocca, senior vice president at Wedbush Securities in San Francisco, noted that economic data prompts a change, the Fed’s tone will likely stay the same.

The expectation that the Fed had concluded its rate hikes drove the S&P 500 up 5.85% and the Nasdaq up 6.61% last week. This climb marked their most significant weekly gains since November 2022. This week’s economic data calendar is relatively sparse, with the release of weekly jobless claims numbers on Thursday and the University of Michigan’s consumer sentiment report on Friday.

Meanwhile, out of 403 companies in the S&P 500 that reported third-quarter profits through Friday, 81.6% exceeded analyst estimates, according to LSEG data.

Elsewhere, European equities dipped as the real estate sector lost momentum. However, Ryanair saw a surge in its stock following a forecast for record annual profit. Recent data revealed an acceleration in the downturn of business activity in the Eurozone last month, raising concerns about a potential recession in the 20-country bloc.

Throughout the week, market watchers will closely examine Eurozone producer prices and retail sales data for September as price pressures ease.