{kind=link}

- Currency futures started the week weak, pressured by a stronger US dollar in the face of delayed expectations of a Fed rate cut following strong jobs data and subdued inflation.

- The euro, pound, and CAD could lose further, while the AUD and JPY remain strong amid clear policy divergence.

- FOMC meeting minutes and Fed communication could further mold market expectations for the currency markets.

Currency futures are under subdued pressure as US inflation data shows cooling, with CPI at 2.4% YoY and 0.2% MoM, bolstering bets on later Fed cuts. CME FedWatch expects two 25-bp cuts this year, mostly after June. Key takeaway: Cooling inflation and delayed Fed action keep USD strong in the short term but may weaken it later.

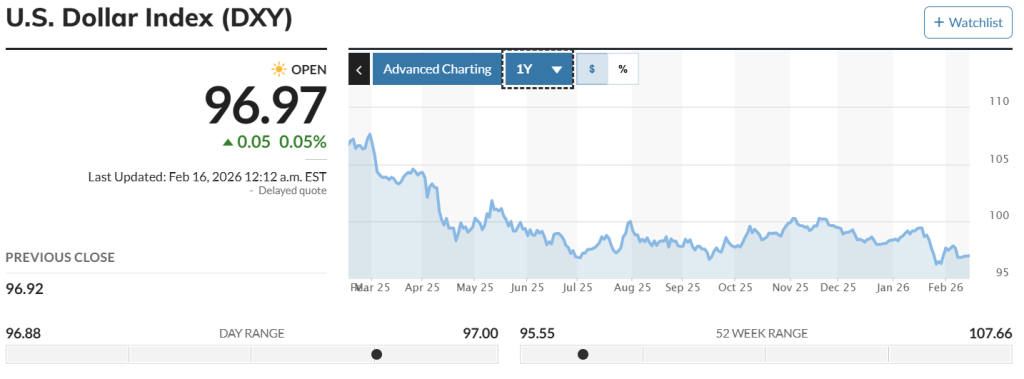

The US job market remains strong, as Nonfarm Payrolls posted the largest gain in over a year and the unemployment rate declined. This firmness in labor data has kept short-term Fed policy expectations steady and cushioned USD futures from immediate losses, resulting in a consolidation bias for the US Dollar Index futures (DXY) near the 97 level. Goolsbee noted progress on inflation and persistently high service prices, strengthening the market view that monetary policy easing will be gradual.

Meanwhile, euro fundamentals are only slightly positive. Euro FX futures (6E) trade lower during the day, but losses are limited because markets expect the Fed to be more dovish than the ECB. Lagarde said inflation in the Eurozone is “in a good place,” and the ECB seems unconcerned by recent euro moves. This reduces urgency for immediate easing, so Euro futures (6E) are likely to outperform USD.

The GBP outlook is more even. This week, markets are focused on UK data (jobs, CPI, retail sales, and PMIs). The Bank of England is expected to cut rates by 25 bps in March. As a result, GBP futures (6B) are uncertain, with the currency positioned between bets on UK easing and the possibility of USD weakening if the Fed cuts rates in June. The key takeaway is that the GBP is caught between domestic rate cut expectations and external USD dynamics.

AUD fundamentals are stronger than USD fundamentals. Markets expect the Fed to cut rates by at least 25 bps in 2026, while the RBA is expected to raise rates in May. Hopes for more Chinese stimulus amid deflation also support AUD futures (6A). In brief, these factors point to a stronger outlook for AUD futures.

The Bank of Canada holds a neutral stance; meanwhile, persistent uncertainty over the Canadian dollar’s 2026 trajectory, along with steady crude oil prices, offers CAD futures (6C) only a modest lift. As a result, this limits substantial USD gains, favoring CAD futures (6C).

Japan’s Q4 GDP underperformed expectations, lowering the likelihood of a near-term BoJ rate hike. Fiscal support prospects offset potential gains in the yen from policy changes. While the USD remains strong, its lead is less clear. The main takeaway: JPY futures (6J) are now driven by data and BoJ communications, and will likely range with global risk sentiment.