- Investors are nearly convinced that the Federal Reserve will deliver a modest interest rate increase next week.

- Money market traders believe the Fed will only raise interest rates twice this year.

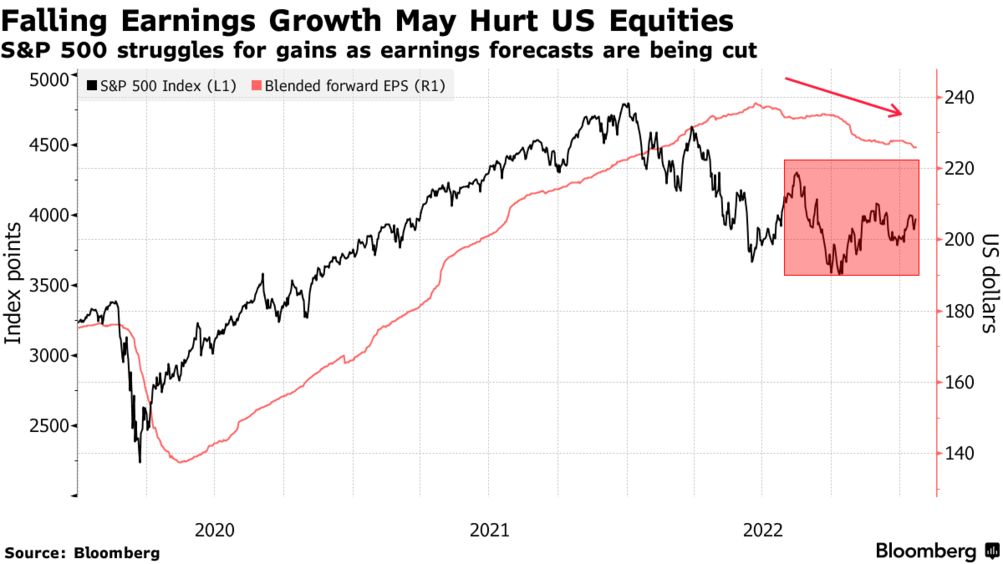

- Analysts predict that the overall S&P 500 fourth-quarter earnings will decline by 3% yearly.

Equities held onto their gains on Tuesday after rallying the previous session. Investors started an earnings-heavy week with fresh enthusiasm for market-leading growth stocks hammered last year, which helped Wall Street close significantly higher on Monday.

The session ushers in the calm before the storm in a week crammed with important economic data and high-profile corporate reports.

Investors are almost convinced that the Federal Reserve will deliver a modest interest rate increase next week. However, it is still dedicated to containing the most intense inflationary cycle in decades.

According to Peter Tuz, president of Chase Investment Counsel, Investors are pretty confident that they will see lesser rate hikes from the Fed and that we are turning the curve on inflation and interest rate hikes. Stocks can perform well in this atmosphere, particularly the market-leading large-growth stocks.

According to CME’s FedWatch tool, financial markets have priced in a 99.9% chance of a 25 basis point increase to the Fed funds target rate after its two-day monetary policy meeting next Wednesday.

Money market traders believe that the Fed will only raise interest rates twice more, reaching a peak of about 5% by June, and then cut rates twice before the year is over. The Fed has maintained that an additional 75 basis points of tightening will likely come.

The fourth-quarter reporting season has accelerated, with 57 S&P 500 businesses having already released their results. According to Refinitiv, 63% of those have posted higher earnings than anticipated.

However, earnings forecasts have gone down, which might hurt US equities. According to Refinitiv, analysts now predict that the overall S&P 500 fourth-quarter earnings will decline by 3% year over year, nearly twice as high as the 1.6% yearly decline observed at the start of the year.

Microsoft Corp. and Tesla Inc. are two high-profile industrials set to report quarterly results this week.

On Thursday, the US Commerce Department is anticipated to release its initial “advance” estimate of fourth-quarter GDP, which economists anticipate will come at 2.5%.

The comprehensive personal consumption expenditures (PCE) data will provide important insight into consumer spending, income growth, and inflation on Friday.